This is a modern-English version of Up To Date Business: Including Lessons in Banking, Exchange, Business Geography, Finance, Transportation and Commercial Law, originally written by unknown author(s).

It has been thoroughly updated, including changes to sentence structure, words, spelling,

and grammar—to ensure clarity for contemporary readers, while preserving the original spirit and nuance. If

you click on a paragraph, you will see the original text that we modified, and you can toggle between the two versions.

Scroll to the bottom of this page and you will find a free ePUB download link for this book.

UP-TO-DATE

BUSINESS

HOME STUDY CIRCLE LIBRARY

EDITED BY

SEYMOUR EATON

UP TO DATE

BUSINESS

INCLUDING

LESSONS IN BANKING, EXCHANGE,

BUSINESS GEOGRAPHY, FINANCE,

TRANSPORTATION AND

COMMERCIAL LAW

FROM THE CHICAGO RECORD

NEW YORK

THE DOUBLEDAY & McCLURE CO.

1900

Copyright, 1897, 1898, 1899, by the Chicago Tribune

Copyright, 1899, by Seymour Eaton

Copyright, 1899, 1900, by Victor F. Lawson

[v]CONTENTS

I

GENERAL BUSINESS INFORMATION

| Page | ||

|---|---|---|

| I. | Commercial Terms and Usages | 3 |

| II. | Commercial Terms and Usages (Continued) | 4 |

| III. | Bank Cheques | 6 |

| IV. | Bank Cheques (Continued) | 8 |

| V. | Bank Cheques (Continued) | 12 |

| VI. | Bank Drafts | 15 |

| VII. | Promissory Notes | 18 |

| VIII. | The Clearing-house System | 21 |

| IX. | Commercial Drafts | 26 |

| X. | Foreign Exchange | 31 |

| XI. | Letters of Credit | 37 |

| XII. | Joint-stock Companies | 41 |

| XIII. | Protested Paper | 46 |

| XIV. | Paper Offered for Discount | 49 |

| XV. | Corporations | 51 |

| XVI. | Bonds | 54 |

| XVII. | Transportation | 57 |

| XVIII. | Transportation Papers | 59 |

| Examination Paper | 64 | |

II

BUSINESS GEOGRAPHY

Trade Characteristics

| I. | The Trade Features of the British Isles | 69 |

| [vi]II. | """"France | 94 |

| III. | """Germany | 102 |

| IV. | """"Spain and Italy | 111 |

| V. | ""Russia | 120 |

| VI. | ""India | 129 |

| VII. | """"China | 139 |

| VIII. | """"Japan | 148 |

| IX. | """"Africa | 157 |

| X. | """"Australia and Australasia | 166 |

| XI. | """"South America | 177 |

| XII. | """"Canada | 187 |

| XIII. | """"The United States | 194 |

| Examination Paper | 210 |

III

FINANCE, TRADE, AND TRANSPORTATION

| I. | National and State Banks | 215 |

| II. | Savings Banks and Trust Companies | 221 |

| III. | Corporations and Stock Companies | 225 |

| IV. | Borrowing and Loaning Money | 228 |

| V. | Collaterals and Securities | 233 |

| VI. | Cheques, Drafts, and Bills of Exchange | 240 |

| VII. | The Clearing-house System | 248 |

| VIII. | Commercial Credits and Mercantile Agencies | 254 |

| IX. | Bonds | 263 |

| X. | Transportation by Rail | 267 |

| XI. | Freight Transportation | 274 |

| XII. | Railroad Rates | 281 |

| XIII. | Stock and Produce Exchanges | 288 |

| XIV. | Storage and Warehousing | 294 |

| Examination Paper | 301 |

[vii]IV

COMMERCIAL LAW

| I. | The Different Kinds of Contracts | 309 |

| II. | The Parties to a Contract | 312 |

| III. | The Parties to a Contract (Continued) | 315 |

| IV. | The Consideration in Contracts | 318 |

| V. | The Essentials of a Contract | 321 |

| VI. | Contracts by Correspondence | 326 |

| VII. | What Contracts Must Be in Writing | 332 |

| VIII. | Contracts for the Sale of Merchandise | 336 |

| IX. | The Warranties of Merchandise | 340 |

| X. | Common Carriers | 344 |

| XI. | The Carrying of Passengers | 347 |

| XII. | On the Keeping of Things | 350 |

| XIII. | Concerning Agents | 353 |

| XIV. | The Law Relating to Bank Cheques | 358 |

| XV. | The Law Relating to Leases | 363 |

| XVI. | Liability of Employers to Employés | 369 |

| XVII. | Liability of Employers to Employés | 373 |

| Examination Paper | 377 |

V

PREPARING COPY FOR THE PRESS

AND PROOF-READING

| I. | Preparing Copy | 381 |

| II. | On the Names and Sizes of Type | 382 |

| III. | The Terms Used in Printing | 384 |

| IV. | Marks Used in Proof-reading | 387 |

[ix]ILLUSTRATIONS

I

GENERAL BUSINESS INFORMATION

| Page | ||

|---|---|---|

| A Poorly Drawn Cheque | 7 | |

| A Carefully Drawn Cheque | 8 | |

| A Cheque Drawn so as to Insure Payment to Proper Party | 9 | |

| A Cheque Payable to Order | 11 | |

| A Blank Indorsement | 11 | |

| A Cheque Made to Obtain Money for Immediate Use | 13 | |

| A Certified Cheque | 14 | |

| A Cheque for the Purchase of a Draft | 16 | |

| A Bank Draft | 17 | |

| Ordinary Form of Promissory Note | 18 | |

| A Promissory Note Filled Out in an Engraved Blank | 19 | |

| A Special Form for a Promissory Note | 20 | |

| The Advantages of the Clearing-house System | 22 | |

| The Route of a Cheque | 24 | |

| Backs of Two Paid Cheques | 25 | |

| A Sight Draft Developed from Letter | 27 | |

| A Sight Draft | 28 | |

| An Accepted Ten-day Sight Draft | 28 | |

| An Accepted Sight Draft | 29 | |

| A Time Draft | 29 | |

| Foreign Exchange | 32 | |

| A Bill of Exchange (Private) | 35 | |

| A Bill of Exchange (Banker's) | 36 | |

| First Page of a Letter of Credit | 38 | |

| Second Page of a Letter of Credit | 40 | |

| A Certificate of Stock in a National Bank | 42 | |

| [x]A Certificate of Stock in a Manufacturing Company | 43 | |

| A Protest | 48 | |

| A Private Bond | 55 | |

| A Shipping Receipt ("Original") | 60 | |

| A Steamship Bill of Lading | 61 | |

| A Local Waybill | 62 | |

II

BUSINESS GEOGRAPHY

| London the Natural Centre of the World's Trade | 72 | |

| British Mercantile Marine | 74 | |

| London Bridge | 76 | |

| The Coal-fields of England | 80 | |

| The Manchester Ship Canal | 84 | |

| The Great Manufacturing Districts of England | 88 | |

| France Compared in Size with the States of Illinois and Texas | 95 | |

| Street Scene in Paris, Showing the Bourse | 97 | |

| Approximate Size of the German Empire | 104 | |

| North Central Germany, Showing the Ship Canal and the Leading Commercial Centres | 109 | |

| Spain Compared in Size with California | 113 | |

| Italy and its Chief Commercial Centres | 117 | |

| Russia, the British Empire, and the United States Compared | 121 | |

| Moscow | 127 | |

| Comparative Sizes of India and the United States | 133 | |

| China and its Chief Trade Centres | 145 | |

| Japan's Relation to Eastern Asia | 155 | |

| The Partition of Africa | 159 | |

| Australia | 171 | |

| The Most Prosperous Part of South America | 183 | |

| Trade Centres of Canada and Trunk Railway Lines | 192 | |

| Export Trade of United States and Great Britain Compared | 198 | |

| [xi]United States Manufactures and Internal Trade Compared with the Manufactures and Internal Trade of all Other Countries | 199 | |

| Principal Articles of Domestic Exports of the United States | 205 | |

III

FINANCE, TRADE, AND TRANSPORTATION

| The Bank of England | 216 | |

| Showing Cheque Raised from $7.50 to $70.50 | 241 | |

| A Certified Cheque | 244 | |

| A Bank Draft | 245 | |

| A Bill of Exchange | 246 | |

| Illustrating Cheque Collections | 252 | |

| A Mercantile Agency Inquiry Form | 259 | |

| Specimens of Interest Coupons | 266 | |

| Judge Thomas M. Cooley, First Chairman of the Interstate Commerce Commission | 287 | |

| The Paris Bourse | 289 | |

| Interior View of New York Stock Exchange | 290 | |

V

PREPARING COPY FOR THE PRESS

AND PROOF-READING

| A Printer's Proof | 390 | |

| A Printer's Corrected Proof | 391 | |

[3]GENERAL BUSINESS INFORMATION

I. COMMERCIAL TERMS AND USAGES

HERE is a distinction between the usage of the names commerce and business. The interchange of products and manufactured articles between countries, or even between different sections of the same country, is usually referred to as commerce. The term business refers more particularly to our dealings at home—that is, in our own town or city. Sometimes this name is used in connection with a particular product, as the coal business or the lumber business, or in connection with a particular class, as the dry-goods business or the grocery business. The name commerce, however, seldom admits of a limited application. In the United States trade is synonymous with business. The word traffic applies more especially to the conveyance than to the exchange of products; thus we refer to railroad traffic or lake traffic. Products, when considered articles of trade, are called merchandise, goods, wares. The term merchandise has the widest meaning, and includes all kinds of movable articles bought or sold. Goods is applied more particularly to the supplies of a merchant. Wares is commonly applied to utensils, as glassware, hardware, etc.

HERE is a distinction between the use of the names business and business. The exchange of products and manufactured goods between countries, or even between different areas of the same country, is usually called commerce. The term business specifically refers to our activities at home—that is, in our own town or city. Sometimes this term is associated with a specific product, like the coal business or the lumber business, or with a specific category, like the dry-goods business or the grocery business. The term commerce, however, is rarely used in a limited sense. In the United States, trade is synonymous with business. The word traffic specifically relates more to the movement than to the exchange of products; for example, we refer to railroad traffic or lake traffic. Items, when considered as items for sale, are called merchandise, goods, wares. The term merch has the broadest meaning and includes all kinds of movable items that are bought or sold. Products is used more specifically for the supplies of a merchant. Goods typically refers to items like utensils, such as glassware, hardware, etc.

Gross commonly means coarse or bulky. In trade it is used with reference to both money and goods. The gross weight of a package includes the weight of the case or[4] wrappings. The larger sum in an account or bill—that is, the sum of money before any allowance or deductions are made—is the gross amount of the bill. The word net is derived from a Latin word meaning neat, clean, unadulterated, and indicates the amount of goods or money after all the deductions have been made. To say that a price is net is to indicate that no further discount will be made.

Disgusting usually means large or heavy. In business, it refers to both money and products. The gross weight of a package includes the weight of the container or[4] packaging. The total amount in an invoice or account—that is, the total amount of money before any subtractions or deductions—is called the gross amount. The term net comes from a Latin word meaning tidy, clear, and pure, and it represents the amount of goods or money after all deductions have been made. When a price is labeled as net, it means that no additional discount will be offered.

The word firm relates to solidity, establishment, strength, and in a business sense signifies two or more persons united in partnership for the purpose of trading. The word house is very frequently used in the same sense. In mercantile usage house does not mean the building in which the business is conducted, but the men who own the business, including, perhaps, the building, stock, plant, and business reputation. The name concern is often used in a very similar way.

The word strong refers to stability, establishment, strength, and in a business context, it means two or more people joined together in a partnership for the purpose of trading. The word home is often used in the same way. In business terminology, house doesn’t refer to the physical building where the business operates, but rather the people who own the business, which may include the building, inventory, equipment, and the business’s reputation. The term worry is commonly used in a similar manner.

The name market expresses a locality for the sale of goods, and in commerce is often used to denote cities or even countries. We say that Boston is a leather market, meaning that a large number of Boston merchants buy and sell leather. In the same sense we call Chicago a grain market, or New Orleans a cotton market. In its more restricted sense the name market signifies a building or place where meat or produce is bought and sold. We say that the market is flooded with a particular article when dealers are carrying more of that article than they can find sale for. There is no market for any product when there is no demand. The money market is tight or close when it is difficult to borrow money from banks and money-lenders.

The term marketplace refers to a place where goods are sold, and in business, it often describes cities or even countries. For example, we say Boston is a leather market, which means many merchants in Boston buy and sell leather. Similarly, we refer to Chicago as a grain market and New Orleans as a cotton market. In a more specific sense, the word market means a building or area where meat or produce is bought and sold. We say that the market is flooded with a certain product when sellers have more of that product than they can sell. There is no market for a product when there is no demand for it. The money market is tight or close when it's hard to borrow money from banks and lenders.

II. COMMERCIAL TERMS AND USAGES (Continued)

The natural resources of a country are mainly the mineral commodities and agricultural produce that it[5] yields. The lumber and fish produced in a country are also among its natural resources. The positions and industries of cities are usually fixed by natural conditions, but the most powerful agent is the personal energy of enterprising and persevering men, who, by superior education, or scientific knowledge, or practical foresight, have often been able to found industrial centres in situations which no geographical considerations would suggest or explain.

Natural resources of a country are mainly the mineral products and agricultural goods that it[5] produces. The timber and fish available in a country are also part of its natural resources. The locations and industries of cities are generally determined by natural conditions, but the strongest influence comes from the personal drive of ambitious and determined individuals, who, through better education, scientific knowledge, or practical foresight, have often been able to establish industrial hubs in places that geographical factors alone wouldn't suggest or justify.

Commission merchants receive and sell goods belonging to others for a compensation called a commission. A selling agent is a person who represents a manufacturing establishment in its dealings with the trade. The factory may be located in a small town, while the selling agent has his office and samples in the heart of a great city. As regards the quantity of goods bought or sold in a single transaction, trade is divided into wholesale and retail. The wholesale dealer sells to other dealers, while the retail dealer sells to the consumer—that is, the person who consumes, or uses, the goods. A jobber is one who buys from importers and manufacturers and sells to retailers. He is constantly in the market for bargains. The names jobber and wholesaler are often used in the same sense, but a jobber sometimes sells to wholesalers. Wholesale has reference to the quantity the dealer sells, and not to the source from which he buys, or the person to whom he sells. The wholesaler, as a rule, deals in staples—that is, goods which are used season after season—though of course there are wholesalers in practically all businesses.

Brokerage firms receive and sell goods owned by others for a fee called a commission. A sales agent is someone who represents a manufacturing company in its transactions with the market. The factory might be based in a small town, while the selling agent operates from an office with samples in a bustling city. In terms of the volume of goods bought or sold in a single transaction, trade is split into bulk and shopping. The wholesale dealer sells to other dealers, while the retail dealer sells directly to consumers—that is, the individuals who consume or use the goods. A freelancer is someone who purchases from importers and manufacturers and sells to retailers. They are always looking for good deals. The terms freelancer and distributor are often used interchangeably, but a jobber can sometimes sell to wholesalers. Wholesale refers to the quantity the dealer sells, not the source from where they buy or the person to whom they sell. Generally, wholesalers deal in staples—goods that are used season after season—though there are wholesalers in nearly every industry.

Wholesale dealers send out travellers or drummers, who carry samples of the goods. Frequently the traveller starts out with his samples from six months to a year in advance of the time of delivery. It is quite a common thing for the retailer to order from samples[6] merchandise which at the time of placing the order may not even be manufactured.

Wholesale dealers send out travelers or sales representatives, who carry samples of the products. Often, the traveler sets off with their samples six months to a year before the delivery date. It's pretty common for retailers to order merchandise from samples[6] that might not even be made yet when they place the order.

By the price of a commodity is meant its value estimated in money, or the amount of money for which it will exchange. The exchangeable value of commodities depends at any given period partly upon the expense of production and partly upon the relation of supply and demand. Prices are affected by the creation of monopolies, by the opening of new markets, by the obstructing of the ordinary channels of commercial intercourse, and by the anticipation of these and other causes. It is the business of the merchant to acquaint himself with every circumstance affecting the prices of the goods in which he deals.

By the cost of a product, we mean its value measured in money, or how much money it can be exchanged for. The exchangeable value of products at any given time depends partly on the cost of production and partly on the dynamics of supply and demand. Prices can be influenced by the creation of monopolies, the emergence of new markets, the disruption of normal trading channels, and expectations about these and other factors. It is the merchant's job to stay informed about every situation that affects the prices of the goods he trades in.

The entire world is the field of the modern merchant. He buys raw and manufactured products wherever he can buy cheapest, and he ships to whatever market pays him the highest price. Our corner grocer or produce-dealer may furnish us with beef from Texas, potatoes from Egypt, celery from Michigan, onions from Jamaica, coffee from Java, oranges from Spain, and a hundred other things from as many different points; and yet, so complete is the interlocking of the world's commercial interests, and so great is the speed of transportation, that he can supply us with these necessaries under existing conditions more easily and readily than if they were all grown on an adjoining farm.

The whole world is now the playground of today’s merchant. They buy raw and manufactured goods wherever they’re the cheapest, and ship them to the markets that offer the highest prices. Our local grocery store might provide us with beef from Texas, potatoes from Egypt, celery from Michigan, onions from Jamaica, coffee from Java, oranges from Spain, and countless other items from many different places; and yet, the interconnectedness of global commercial interests, along with the fast pace of transportation, allows them to supply these essentials to us much more easily and quickly than if everything were produced on a nearby farm.

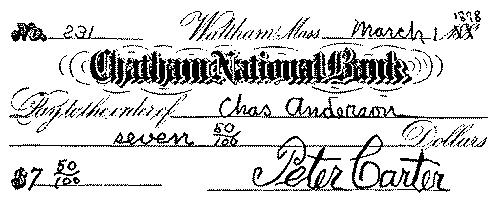

III. BANK CHEQUES

A cheque is an order for money, drawn by one who has funds in the bank. It is payable on demand. In reality, it is a sight draft on the bank. Banks provide blank cheques for their customers, and it is a very simple matter to fill them out properly. In writing in the amount begin at the extreme left of the line.

A check is an instruction for money, issued by someone who has money in the bank. It can be cashed immediately. Essentially, it's a sight draft on the bank. Banks give their customers blank checks, and it's quite easy to fill them out correctly. When writing the amount, start at the far left of the line.

[7]The illustration given below shows a poorly written cheque and one which could be very easily raised. A fraudulent receiver could, for instance write, "ninety" before the "six" and "9" before the figure "6," and in this way raise the cheque from $6 to $96. If this were done and the cheque cashed, the maker, and not the bank, would become responsible for the loss. You cannot hold other people responsible for your own carelessness. A cheque has been raised from $100 to $190 by writing the words "and ninety" after the words "one hundred." One of the ciphers in the figures was changed to a "9" by adding a tail to it. It is wise to draw a running line, thus ~~~~~~, after the amount in words, thus preventing any additional writing.

[7]The illustration below shows a poorly written check and one that could be easily altered. A dishonest person could write "ninety" before the "six" and "9" before the number "6," thus changing the check from $6 to $96. If this happens and the check is cashed, the person who wrote it, not the bank, would be responsible for the loss. You can't expect others to take the blame for your own mistakes. A check was changed from $100 to $190 by adding the words "and ninety" after "one hundred." One of the numbers was altered by modifying a digit to a "9" by adding a small line to it. It's a good idea to draw a line through the space after the amount in words, like this Sure, please provide the text you would like me to modernize., to prevent any extra writing.

A badly drawn check.

A badly drawn check.

The illustration on page 8 shows a cheque carefully and correctly drawn. The signature should be in your usual style, familiar to the paying teller. Sign your name the same way all the time. Have a characteristic signature, as familiar to your friends as is your face.

The illustration on page 8 shows a check carefully and accurately written. The signature should be in your regular style, known to the paying teller. Sign your name the same way every time. Have a distinct signature, as recognizable to your friends as your face.

A cheque is a draft or order upon your bank, and it need not necessarily be written in the prescribed form. Such an order written on a sheet of note-paper with[8] a lead-pencil might be in every way a legally good cheque.

A check is an order to your bank, and it doesn't have to be in a specific format. An order written on a piece of note paper with [8] a pencil could still be a legally valid check.

A carefully written check.

A carefully written check.

Usually cheques should be drawn "to order." The words "Pay to the order of John Brown" mean that the money is to be paid to John Brown, or to any person that he orders it paid to. If a cheque is drawn "Pay to John Brown or Bearer" or simply "Pay to Bearer," any person that is the bearer can collect it. The paying teller may ask the person presenting the cheque to write his name on the back, simply to have it for reference.

Usually, checks should be made out "to order." The phrase "Pay to the order of John Brown" means that the money is to be paid to John Brown or to anyone he designates to receive it. If a check is written "Pay to John Brown or Bearer" or just "Pay to Bearer," anyone who has the check can cash it. The teller may ask the person cashing the check to write their name on the back, just to keep it for reference.

In writing and signing cheques use good black ink and let the copy dry a little before a blotter is used.

In writing and signing checks, use good black ink and let the copy dry a bit before using a blotter.

The subject of indorsements will be treated in a subsequent lesson.

We'll cover the topic of endorsements in a later lesson.

IV. BANK CHEQUES (Continued)

The banks of this country make it a rule not to cash a cheque that is drawn payable to order, unless the person presenting the cheque is known at the bank, or unless he satisfies the paying teller that he is really the person to whom the money should be paid. It must be remembered[9] however, that a cheque drawn to order and then indorsed in blank by the payee is really payable to bearer, and if the paying teller is satisfied that the payee's signature is genuine he will not likely hesitate to cash the cheque. In England all cheques apparently properly indorsed are paid without identification.

The banks in this country have a rule against cashing a check made out to order unless the person presenting it is known by the bank or can convince the teller that they are the correct person to receive the money. It’s important to remember[9] that a check made to order and then endorsed in blank by the payee is essentially payable to whoever holds it, and if the teller believes the payee's signature is authentic, they are unlikely to refuse to cash the check. In England, all checks that are properly endorsed seem to be cashed without the need for identification.

A check written to ensure payment to the correct party.

A check written to ensure payment to the correct party.

In drawing a cheque in favour of a person not likely to be well known in banking circles, write his address or his business after his name on the face of the cheque. For instance, if you should send a cheque to John Brown, St. Louis, it might possibly fall into the hands of the wrong John Brown; but if you write the cheque in favour of "John Brown, 246 West Avenue, St. Louis," it is more than likely that the right person will collect it.

When writing a check to someone who isn’t well-known in banking, include their address or business after their name on the front of the check. For example, if you send a check to John Brown in St. Louis, it could easily end up with the wrong John Brown. However, if you write the check to "John Brown, 246 West Avenue, St. Louis," it’s much more likely that the right person will receive it.

If you wish to get a cheque cashed where you are unknown, and it is not convenient for a friend who has an account at the bank to go with you for the purpose of identification, ask him to place his signature on the back of your cheque, and you will not likely have trouble in getting it cashed at the bank where your friend keeps his account. By placing his signature upon the back of the cheque he guarantees the bank against loss. A bank[10] is responsible for the signatures of its depositors, but it cannot be supposed to know the signatures of indorsers. The reliable identifier is in reality the person who is responsible.

If you want to cash a check where you’re not known, and it’s not convenient for a friend with a bank account to go with you for identification, ask them to sign the back of your check. This way, you’re less likely to have issues cashing it at your friend’s bank. By signing the back, they’re guaranteeing the bank against any loss. A bank[10] is responsible for the signatures of its account holders, but it can’t be expected to recognize the signatures of endorsers. The true identifier is actually the person who takes responsibility.

INDORSING CHEQUES

- In indorsing cheques note the following points:

- Write across the back—not lengthwise.

- If your indorsement is the first, write it about two inches from the top of the back; if it is not the first indorsement, write immediately under the last indorsement.

- Do not indorse wrong end up; the top of the back is the left end of the face.

- Write your name as you are accustomed to write it, no matter how it is written on the face. If you are depositing the cheque write or stamp "For Deposit" or "Pay to ______Bank______," as may be the custom, over your signature. This is hardly necessary if you are taking the cheque yourself to the bank. A cheque with a simple or blank indorsement on the back is payable to bearer, and if lost the finder might succeed in collecting it; but if the words "For Deposit" appear over the name the bank officials understand that the cheque is intended to be deposited, and they will not cash it.

- If you wish to make the cheque payable to some particular person by indorsing, write "Pay now ______(name)______ or order," and under this write your own name as you are accustomed to sign it.

- Do not carry around indorsed cheques loosely. Such cheques are payable to bearer and may be collected by any one.

- [11]If you receive a cheque which has been transferred to you by a

blank indorsement (name of indorser only), and you wish to hold it a

day or two, write over the indorsement the words "Pay to the order of

(yourself—writing your own name)." This is allowable legally. The

cheque cannot then be collected until you indorse it.

A check made out to someone and signed over without specifying a particular person.

A check made out to someone and signed over without specifying a particular person.

- [12]An authorised stamped indorsement is as good as a written one. Whether such indorsements are accepted or not depends upon the regulations of the clearing-house in the particular city in which they are offered for deposit. The written indorsement is considered safer for transmission of out-of-town collections.

- If you are indorsing for a company, or society, or corporation, write first the name of the company (this may be stamped on) and then your own name, followed by the word "Treasurer."

- If you have power of attorney to indorse for some particular person, write his name, followed by your own, followed by the word "Lawyer" or "Attorney.," as it is usually written.

- It is sometimes permissible to indorse the payee's name thus, "By ______(your own name)." This may be done by a junior member of a concern when the person authorised to indorse cheques is absent and the cheques are deposited and not cashed.

- Do not write any unnecessary information on the back of your cheque. A story is told of a woman who received a cheque from her husband, and when cashing it wrote "Your loving wife" above her name on the back.

V. BANK CHEQUES (Continued)

If you wish to draw money from your own account, the most approved form of cheque is written "Pay to the order of Cash." This differs from a cheque drawn to "Bearer." The paying teller expects to see yourself, or some one well known to him as your representative, when you write "Cash." If you write "Pay to the order of[13] (your own name)" you will be required to indorse your cheque before you can get it cashed.

If you want to withdraw money from your own account, the best way to write a check is "Pay to the order of Cash." This is different from a check made out to "Bearer." The teller will expect to see you, or someone he knows as your representative, when you write "Cash." If you write "Pay to the order of[13] (your own name)" you’ll need to sign your check before you can cash it.

If your note is due at your own bank and you wish to draw a cheque in payment, write "Pay to the order of Bills Payable." If you wish to write a cheque to draw money for wages, write "Pay to the order of Pay-roll." If you wish to write a cheque to pay for a draft which you are buying, write "Pay to the order of N. Y. Draft and Exchange," or whatever the circumstances may call for.

If your note is due at your bank and you want to write a check to pay it, write "Pay to the order of Bills Payable." If you want to write a check to get cash for wages, write "Pay to the order of Pay-roll." If you want to write a check to pay for a draft you're purchasing, write "Pay to the order of N. Y. Draft and Exchange," or whatever fits the situation.

A check written to get cash for immediate use.

A check written to get cash for immediate use.

If you wish to stop the payment of a cheque which you have issued you should notify the bank at once, giving full particulars.

If you want to stop the payment on a check you've written, you should immediately notify the bank with all the details.

Banks have a custom, after paying and charging cheques, of cancelling them by punching or making some cut through their face. These cancelled cheques are returned to the makers at the end of each month.

Banks have a practice of canceling checks after processing them by punching a hole or making a cut through the front. These canceled checks are sent back to the issuers at the end of each month.

If you have deposited a cheque and it is returned through your bank marked "No Funds," it signifies that the cheque is worthless and that the person upon whose account it was drawn has no funds to meet it. Your bank will charge the amount to your account. The best thing to[14] do in such a case is to hold the cheque as evidence of the debt, and write the person who sent it to you, giving particulars and asking for an explanation.

If you deposit a check and it gets returned by your bank marked "No Funds," it means that the check has no value and that the person who wrote it doesn't have enough money in their account to cover it. Your bank will deduct the amount from your account. The best thing to[14] do in this situation is to keep the check as proof of the debt, and write to the person who sent it to you, providing details and asking for an explanation.

If you wish to use your cheque to pay a note due at some other bank, or in buying real estate, or stocks, or bonds, you may find it necessary to get the cheque certified. This is done by an officer of the bank, who writes or stamps across the face of the cheque the words "Certified" or "Good When Properly Indorsed," and signs his name. (See illustration.) The amount will immediately be deducted from your account, and the bank, by guaranteeing your cheque, becomes responsible for its payment. Banks will usually certify any cheque drawn upon them if the depositor has the amount called for to his credit, no matter who presents the cheque, and this certifying makes it feasible for a man to carry in his pocket any amount of actual cash. If you should get a cheque certified and then not use it, deposit it in your bank, otherwise your account will be short the amount for which the cheque is drawn. In Canada all cheques are presented to the "ledger-keeper" for certification before being presented to the paying teller.

If you want to use your check to pay a bill at another bank, or for purchasing real estate, stocks, or bonds, you might need to have the check certified. This is done by a bank officer, who writes or stamps the words "Certified" or "Good When Properly Indorsed" across the front of the check and signs their name. (See illustration.) The amount will be immediately deducted from your account, and by guaranteeing your check, the bank takes responsibility for its payment. Banks typically certify any check drawn on them if the depositor has enough funds available, regardless of who presents the check, and this certification allows a person to carry around the equivalent of cash. If you have a check certified but then don't use it, deposit it in your bank; otherwise, your account will be short the amount of the check. In Canada, all checks are presented to the "ledger-keeper" for certification before being brought to the paying teller.

[15]THE USEFULNESS OF BANKS

Banks are absolutely necessary to the success of modern commercial enterprises. They provide a place for the safe-keeping of money and securities, and they make the payment of bills much more convenient than if currency instead of cheques were the more largely used. But the great advantage of a banking institution to a business man is the opportunity it affords him of borrowing money, of securing cash for the carrying on of his business while his own capital is locked up in merchandise or in the hands of his debtors. Another important advantage is to be found in the facilities afforded by banks for the collection of cheques, notes, and drafts.

Banks are essential for the success of modern businesses. They offer a secure place to keep money and investments, and they make paying bills much more convenient than relying solely on cash. However, the major benefit of a bank for a business owner is the ability to borrow money, allowing them to access cash to run their business while their own funds are tied up in inventory or owed by customers. Another significant advantage is the convenience banks provide in collecting checks, promissory notes, and drafts.

VI. BANK DRAFTS

A draft is a formal demand for the payment of money. Your bank cheque is your sight draft on your bank. It is not so stated, but it is so understood. A cheque differs from an ordinary commercial draft, both in its wording and in its purpose. The bank is obliged to pay your cheque if it holds funds of yours sufficient to meet it, while the person upon whom your draft is drawn may or may not honour it at his pleasure. A cheque is used for paying money to a creditor, while a draft is used as a means of collecting money from a debtor.

A draft is a formal request for payment. Your bank check acts as a sight draft on your bank. It might not be explicitly stated, but it's understood that way. A check is different from a regular commercial draft, both in its wording and intention. The bank must pay your check if it has enough of your funds to cover it, whereas the person who receives your draft can choose whether or not to honor it. A check is used to pay money to a creditor, while a draft is used to collect money from a debtor.

Nearly all large banks keep money on deposit with one or more of the banks located in the great commercial centres. They call these centrally located banks their correspondents. The larger banks have correspondents in New York, Chicago, Boston, and other large cities.[16] As business men keep money on deposit with banks to meet their cheques, so banks keep money on deposit with other banks to meet their drafts.

Nearly all large banks have funds deposited with one or more banks situated in major commercial centers. They refer to these centrally located banks as their correspondents. The bigger banks have correspondents in New York, Chicago, Boston, and other major cities.[16] Just as businesspeople maintain deposits with banks to cover their checks, banks keep deposits with other banks to cover their drafts.

A bank draft is simply the bank's cheque, drawn upon its deposit with some other bank. Banks sell these cheques to their customers, and merchants make large use of them in paying bills in distant cities. These drafts, or cashiers' cheques, as they are sometimes called, pass as cash anywhere within a reasonable distance of the money centre upon which they are drawn. Bankers' drafts on New York would, under ordinary financial conditions, be considered cash anywhere in the United States. A draft on a foreign bank is usually called a bill of exchange.

A bank transfer is basically a cheque from the bank, taken from its deposits with another bank. Banks sell these cheques to their customers, and merchants often use them to pay bills in different cities. These drafts, or cashier's checks, as they're sometimes referred to, are treated like cash anywhere within a reasonable distance of the money center they are drawn on. Bank drafts from New York would generally be considered cash anywhere in the United States under normal financial conditions. A draft from a foreign bank is usually called a bill of exchange.

A check for buying a draft.

A check for buying a draft.

Cheques have come to be quite generally used for the payment of bills even at long distances. If a business man desires to close an important contract requiring cash in advance he sends a bank draft, if at a distance, or a certified cheque, if in the same city. If he desires simply to pay a debt he sends his own personal cheque. Bank drafts are quite generally used by merchants in the West to pay bills in the East. A draft on New York[17] bought in San Francisco is cash when it reaches New York, while a San Francisco cheque is not cash until it returns and is cashed by the bank upon which it is drawn. In the ordinary course of business cheques are considered cash no matter upon what bank drawn. The bank receiving them on deposit gives the depositor credit at once, even though it may take a week before the value represented by the cheque is in the possession of the bank.

Checks are now widely used for paying bills, even over long distances. If a businessman wants to finalize an important contract that needs cash upfront, he’ll send a bank draft if he’s far away, or a certified check if he’s in the same city. If he just needs to pay a debt, he sends his personal check. Bank drafts are commonly used by merchants in the West to settle bills in the East. A draft on New York[17] purchased in San Francisco is considered cash when it arrives in New York, while a San Francisco check isn’t cash until it comes back and is cashed by the bank it’s drawn on. In regular business practice, checks are treated as cash no matter which bank they're from. The bank receiving them for deposit gives the depositor credit immediately, even though it might take a week for the funds represented by the check to actually reach the bank.

A bank check.

A bank check.

All wholesale transactions and a large proportion of retail transactions are completed by the passing of instruments of credit—notes, cheques, drafts, etc.; a part only of the retail trade is conducted by actual currency-bills and "change." Banks handle the bulk of these transferable titles and deal to a very small extent—that is, proportionally—in actual money. The notes, drafts, bills of exchange, and bank cheques are representative of the property passing by title in money from the producers to the consumers. A small proportion—perhaps six or eight per cent.—of these transactions is conducted by the use of actual bank or legal-tender notes. This trade in[18] instruments of credit amounts in the United States to fifty billions of dollars yearly.

All wholesale transactions and a large portion of retail transactions are handled through credit instruments—such as notes, checks, drafts, etc. Only a small part of retail trade is carried out using physical currency bills and "change." Banks manage the majority of these transferable instruments and only deal minimally—in relative terms—in actual cash. The notes, drafts, bills of exchange, and bank checks represent the property being transferred in money from producers to consumers. A small percentage—about six to eight percent—of these transactions occur using actual banknotes or legal tender. This trade in [18] credit instruments amounts to fifty billion dollars annually in the United States.

VII. PROMISSORY NOTES

Standard promissory note.

Standard promissory note.

A promissory note is a written promise to pay a specified sum of money. At the time of the note's issue—that is, when signed and delivered—two parties are connected with it, the maker and the payee. The maker is the person who signs or promises to pay the note; the payee is the person to whom or to whose order the note is made payable. Negotiable in a commercial sense means transferable, and a negotiable note is a note which can be transferred from one person to another. A note to be made negotiable must contain the word bearer or the word order—that is, it must be payable either to bearer, or to the order of the payee. A non-negotiable note is payable to a particular person only. A note may be written on any[19] kind of paper, in ink or pencil. It is wise, however, to use ink to prevent changes. All stationers sell blank forms for notes which are easily filled in.

A IOU is a written promise to pay a specific amount of money. When the note is issued—meaning when it’s signed and handed over—there are two parties involved: the maker and the payee. The maker is the person who signs or promises to pay the note; the payee is the person to whom the note is payable. Open to negotiation, in a business context, means transferable, and a negotiable note is one that can be transferred from one person to another. For a note to be negotiable, it must include the word bearer or order—meaning it must be payable either to bearer or to the order of the payee. A non-negotiable note is payable to a specific person only. A note can be written on any[19] type of paper, in ink or pencil. However, it’s best to use ink to avoid changes. All stationery stores sell blank forms for notes that are easy to fill out.

The samples of notes which appear in this lesson are selected simply to illustrate to students the fact that there are a great many special forms of notes in common use. The wording differs slightly in different States.

The notes provided in this lesson are chosen just to show students that there are many special types of notes commonly used. The wording varies a bit from one state to another.

The date of a note is a matter of the first importance. Some bankers and business men consider it better to draw notes payable at a certain fixed time, as, "I promise to pay on the 10th of March, 1897." The common custom is to make notes payable a certain number of days or months after date. A note made or issued on Sunday is void. The day of maturity is the day upon which a note becomes legally due. In several of the States a note is not legally due until three days, called days of grace, after the expiration of the time specified in the note.

The date on a note is extremely important. Some bankers and business people believe it's better to create notes that are payable at a specific date, like, "I promise to pay on March 10, 1897." The usual practice is to make notes payable a certain number of days or months after the date. A note created or issued on a Sunday is invalid. The maturity day is the day when a note is legally due. In several States, a note isn't considered legally due until three days later, known as grace period, after the time specified in the note.

A promissory note completed on a printed blank form.

A promissory note completed on a printed blank form.

The words value received, which usually appear upon notes, are not necessary legally. Thousands of good notes made without any value consideration are handled daily.

The phrase value received, which typically appears on notes, isn't legally required. Every day, thousands of valid notes are processed without any consideration of value.

[20]The promise to pay of a negotiable note must be unconditional. It cannot be made to depend upon any contingency whatever.

[20]The pay promise of a negotiable note has to be unconditional. It can't be tied to any kind of condition.

Notes that are made in settlement of genuine business transactions come under the head of regular, legitimate business paper. An accommodation note is one which is signed, or indorsed, simply as an accommodation, and not in settlement of an account or in payment of an indebtedness. With banks accommodation paper has a deservedly hard reputation. However, there are all grades and shades of accommodation paper, though it represents no actual business transaction between the parties to it, and rests upon no other foundation than that of mutual agreement. No contract is good without a consideration, but this is only true between the original parties to a note. The third party or innocent receiver or holder of a note has a good title, and can recover its value, even though it was originally given without a valuable consideration. An innocent holder of a note which had been originally lost or stolen has a good title to it if he received it for value.

Notes made in the settlement of genuine business transactions fall under the category of regular, legitimate business instruments. An housing note is one that is signed or endorsed simply as a favor, and not as a means to settle an account or pay off a debt. In the banking world, accommodation paper has a deservedly bad reputation. However, there are various types of accommodation paper, even though it does not reflect any actual business transaction between the parties involved and is based solely on mutual agreement. No contract is valid without consideration, but this only applies to the original parties to a note. A third party or innocent holder of a note has a legal right to it and can claim its value, even if it was initially issued without valuable consideration. An innocent holder of a note that was originally lost or stolen has a valid title to it if they received it for value.

A specific format for a promissory note.

A specific format for a promissory note.

[21]A note does not draw interest until after maturity, unless the words with interest appear on the face. Notes draw interest after maturity and until paid, at the legal rate.

[21]A note doesn’t earn interest until after it matures, unless it says with interest on the front. Notes earn interest after maturity and until they’re paid, at the legal rate.

A note should be presented for payment upon the exact day of maturity. Notes made payable at a bank, or at any other place, must be presented for payment at the place named. When no place is specified the note is payable at the maker's place of business or at his residence.

A note should be presented for payment on the exact due date. Notes that are payable at a bank or any other location must be presented for payment at the specified place. If no place is mentioned, the note is payable at the maker's business address or at their home.

In finding the date of maturity it is important to remember that when a note is drawn days after date the actual days must be counted, and when drawn months after date the time is reckoned by months.

In determining the date of maturity, it's important to remember that when a note is written days after date, the actual days must be counted, and when written months after date, the time is calculated by months.

To discount a note is to sell it at a discount. The rates of discount vary according to the security offered, or the character of the loan, or the state of the money market. For ordinary commercial paper the rates run from four to eight per cent. Notes received and given by commercial houses and discounted by banks are not usually for a longer period than four months.

To sale a note means to sell it for less than its face value. The discount rates depend on the security provided, the nature of the loan, or the current conditions of the money market. For typical commercial paper, the rates range from four to eight percent. Notes that commercial businesses issue and receive, which are then discounted by banks, usually have a duration of no more than four months.

VIII. THE CLEARING-HOUSE SYSTEM

In large cities cheques representing millions of dollars are deposited in the banks every day. The separate collection of these would be almost impossible were it not for the clearing-house system. Each large city has its clearing-house. It is an establishment formed by the banks themselves, and for their own convenience. The leading banks of a city connect themselves with the clearing-house of that city, and through other banks with the clearing-houses of other cities, particularly New York. Country banks connect themselves with one or more clearing-houses through city banks, which do their[22] business for them. The New York banks, largely through private bankers, branches of foreign banking houses, connect themselves with London, so that each bank in the world is connected indirectly with every other bank in the world, and in London is the final clearing-house of the world.

In big cities, millions of dollars in checks are deposited in banks every day. Collecting these individually would be nearly impossible without the clearing-house system. Each major city has its own clearing-house, set up by the banks for their convenience. The leading banks in a city connect with that city's clearing-house and, through other banks, with the clearing-houses of other cities, especially New York. Rural banks connect to one or more clearing-houses through city banks that handle their[22] business. The New York banks, mainly through private bankers and branches of foreign banks, connect with London, making it so that each bank in the world is indirectly linked to every other bank, with London serving as the ultimate clearing-house globally.

The benefits of the clearing-house system.

The benefits of the clearing-house system.

Suppose that the above diagram represents the banks and clearing-house of a city, and also the two business houses of Brown and Smith. Brown keeps his money on deposit in Bank E, and Smith in Bank B. Brown sends (by mail) a cheque to Smith in payment of a bill. Now, Smith can come all the way to Bank E, and, if he is properly identified, can collect the cheque. He does not do this, however, but deposits Brown's cheque in[23] Bank B, the bank where he does his banking business. Now, B cannot send to E to get the money. It could do this, perhaps, if it had only one cheque, but it has taken in hundreds of cheques, some, perhaps, on every bank in town, and on many banks out of town. It would take a hundred messengers to collect them. So, instead of B's going to E, they meet half-way, or at a central point called a clearing-house, and there collect their cheques. B may have $5000 in cheques on E, and E may have $4000 in cheques on B, so that the exchange can be made—that is, the cheques can be paid by E paying the difference of $1000, which is done, not direct, but through the officers of the clearing-house. Now Bank E's messenger carries Brown's cheque back with him and enters it up against Brown's account. This in simple language is the primary idea of the clearing-house.

Suppose the diagram above represents the banks and clearinghouse of a city, as well as the two businesses of Brown and Smith. Brown has his money deposited in Bank E, and Smith in Bank B. Brown sends a check to Smith by mail to pay a bill. Instead of traveling all the way to Bank E to cash the check—if he can prove his identity—Smith decides to deposit Brown's check at Bank B, where he usually banks. Bank B can't just send someone to Bank E to collect the money. It might manage this if it only had one check, but it's taken in hundreds of checks, some from every bank in town and even from many banks outside of it. It would take a hundred messengers to collect them all. So, instead of Bank B going to Bank E, they meet halfway, at a central location called a clearinghouse, to settle their checks. Bank B might have $5,000 in checks from Bank E, and Bank E could have $4,000 in checks from Bank B, allowing for an exchange. This means Bank E can clear the checks by simply paying the $1,000 difference, done indirectly through the clearinghouse officers. Then, the messenger from Bank E takes Brown's check back with him and credits it to Brown's account. This is basically the main idea of the clearinghouse.

The clearings in New York in one day amount to from one to two hundred millions of dollars. By clearings we mean the value of the cheques which are cleared—that is, which change hands through the clearing-house. Usually once a week (in some cities oftener) the banks of a city make to their clearing-house a report, based on daily balances, of their condition.

The clearings in New York in one day total between one and two hundred million dollars. By clearings, we mean the value of the checks that are cleared—that is, those that are processed through the clearing-house. Typically, once a week (and sometimes more often in certain cities), the banks in a city submit a report to their clearing-house, based on daily balances, regarding their status.

The process of a cheque.

The process of a cheque.

To illustrate the connection between banks at distant points let us suppose that B of Media, Pennsylvania, who keeps his money on deposit in the First National Bank of Media, sends a cheque in payment of a bill to K of South Evanston, Illinois. K deposits the cheque in the Citizens Bank of his town and receives immediate credit for it upon his bank-book, just the same as though the cheque were drawn upon the same or a near-by bank. The Citizens Bank simply sends the cheque, with other distant cheques, to its correspondent, the National Bank of the Republic, Chicago, on deposit, in many instances in about the same sense that K deposited the cheque in the Citizens Bank. The National Bank of the Republic sends the cheque, with other cheques, to its New York correspondent, the National Park Bank. It may possibly send to Philadelphia direct, or even to Media; but this is very unlikely. The National Park Bank sends the cheque to its Philadelphia correspondent, say the Penn National Bank. Now the clearing-house clerk of the Penn National carries the cheque to the Philadelphia clearing-house and enters it, with other cheques, on the First National of Media. Custom, however, differs very greatly in this particular. Many near-by country banks clear through city banks; others clear less directly. If the First National Bank of Philadelphia is known at the clearing-house as the representative of the First National Bank of Media it likely has money belonging to this Media bank on deposit. In that case the cheque is charged up against the account of the First National of Philadelphia. This bank then sends the cheque to the First National of Media, by which it is charged up against B. This system of collection of cheques is about as perfect as is the post-office system of carrying registered mail.

To show how banks at different locations are connected, let’s imagine that B from Media, Pennsylvania, who has his money deposited at the First National Bank of Media, sends a check to K in South Evanston, Illinois, to pay a bill. K deposits the check at his local Citizens Bank and gets immediate credit in his bank account, just like if the check was drawn from the same bank or one nearby. The Citizens Bank then forwards the check, along with other checks from far away, to its partner, the National Bank of the Republic in Chicago, essentially in the same way K deposited it at his bank. The National Bank of the Republic sends the check, along with others, to its New York partner, the National Park Bank. It might send it directly to Philadelphia or even back to Media, but that's not very likely. The National Park Bank then sends the check to its Philadelphia partner, like the Penn National Bank. The clerk at the Penn National takes the check to the Philadelphia clearinghouse and processes it with other checks for the First National Bank of Media. However, practices in this area can vary widely. Some nearby rural banks clear transactions through city banks, while others take a more indirect approach. If the First National Bank of Philadelphia is recognized at the clearinghouse as the representative bank for the First National Bank of Media, it likely has funds from Media's bank on deposit. In that case, the check is deducted from the account of the First National Bank of Philadelphia. Then, this bank sends the check to the First National Bank of Media, which charges it to B’s account. This system for collecting checks is nearly as efficient as the post office's method for handling registered mail.

Backs of two paid checks.

Backs of two paid checks.

[26]Now, the banks and clearing-houses through which the cheque passes on its way home stamp their indorsements and other information upon the back. Our illustration shows the backs of two cheques which have "travelled." Millions of dollars are collected by banks daily in this way, and all without expense to their customers. It is estimated that these collections cost the New York City banks more than two million dollars a year in loss of interest while the cheques are en route. Ten thousand collection letters are sent out daily by the banks of New York City alone.

[26]Now, the banks and clearinghouses that process the cheque on its way home stamp their endorsements and other details on the back. Our illustration shows the backs of two cheques that have "travelled." Millions of dollars are collected by banks every day this way, all at no cost to their customers. It's estimated that these collections cost New York City banks over two million dollars a year in lost interest while the cheques are in transit. Ten thousand collection letters are sent out daily by the banks in New York City alone.

IX. COMMERCIAL DRAFTS

A commercial draft bears a close resemblance to a letter from one person to another requesting that a certain sum of money be paid to the person who calls, or to the bank or firm for whom he is acting. For instance, the draft shown in the first illustration might be worded something like this:[27]

A commercial invoice looks a lot like a letter from one person to another asking for a specific amount of money to be paid to the person making the request or to the bank or company they represent. For example, the draft displayed in the first illustration could be written like this:[27]

St. Louis, Mo., Feb. 22, 1899.

St. Louis, MO, Feb. 22, 1899.

Mr. Robert Elsmere,

Mr. Robert Elsmere,

Jefferson City, Mo.

Jefferson City, MO

My dear Sir:

Dear Sir:

Will you kindly pay to the messenger from the —— Bank who will call to-morrow the sum of three hundred and ninety-seven dollars and charge to my account?

Could you please pay the messenger from the Sure, please provide the text you'd like me to modernize. Bank who will come tomorrow the amount of three hundred and ninety-seven dollars and charge it to my account?

Yours, very truly,

Best regards,

David Grieve.

David Grieve.

A sight draft created from the letter above.

A sight draft created from the letter above.

Commercial usage, however, recognises a particular form in which this letter is to be written, and the address of the person for whom it is intended is usually written at the lower left-hand corner instead of on an envelope. Commercial drafts usually reach the persons upon whom they are drawn through the medium of the banks rather than directly by mail. Let us illustrate. Suppose that A of Chicago owes B of Buffalo $200, and B desires to collect the amount by means of a draft. He fills in a blank draft, signs it, and addresses it on the[28] lower left-hand corner to A. Instead of sending it by mail he takes it to his bank—that is, deposits it for collection. It will reach a Chicago bank in about the same way that cheques for collection go from one place to another. A messenger from the Chicago bank will carry the draft to A's office and present it for payment or for acceptance. If it is a sight draft—that is, a draft payable when A sees it—he may give cash for it at once and take the draft as his receipt. If he has not the money convenient he may write across the face "Accepted, payable at (his) Bank," as in the illustration. It will then reach his bank and be paid as his personal cheque would be, and should be entered in his cheque-book. Banks usually give one day upon sight drafts. The draft will not be presented a second time, but will be held at the bank until the close of the banking hours the next day, where A can call to pay if he chooses. Leniency in the matter of time will depend largely upon B's instructions and the bank's attitude toward A. If the draft is a time draft—that is, if B gives A time, a certain number of days, in which to pay it—A, if he wishes to pay the draft, accepts it. He does this by writing the word accepted with the date and his signature across the face of the draft. He may make it payable at his bank as he would a note, if he so desires. He then returns the draft to the messenger, and if the time is long the draft is returned to B; if only a few days, the bank holds it for collection.

Commercial usage, however, specifies a particular format for this letter, and the address of the person it’s intended for is usually written in the lower left-hand corner instead of on an envelope. Commercial drafts typically reach the parties they’re drawn on through banks rather than directly by mail. Let’s illustrate. Suppose A in Chicago owes B in Buffalo $200, and B wants to collect that amount via a draft. He fills out a blank draft, signs it, and addresses it in the[28] lower left-hand corner to A. Instead of mailing it, he takes it to his bank—meaning he deposits it for collection. It will get to a Chicago bank in a similar way that cheques for collection travel from one place to another. A messenger from the Chicago bank will carry the draft to A's office and present it for payment or acceptance. If it’s a sight draft—that is, a draft payable when A sees it—he might pay cash for it right away and take the draft as his receipt. If he doesn’t have the cash on hand, he might write across the face "Accepted, payable at (his) Bank," like in the illustration. It will then go to his bank and be paid just like his personal cheque would be, and he should record it in his cheque book. Banks usually allow one day for sight drafts. The draft won’t be presented a second time but will be kept at the bank until the end of banking hours the next day, where A can go to pay if he wants. Any leniency regarding time will largely depend on B's instructions and the bank's view of A. If the draft is a time draft—that is, if B gives A a certain number of days to pay—it means A needs to accept it if he wants to pay. He does this by writing the word accepted with the date and his signature across the front of the draft. He can make it payable at his bank as he would a note if he wishes. He then gives the draft back to the messenger, and if the time frame is long, the draft is sent back to B; if it’s only a few days, the bank holds it for collection.

A sight draft.

A sight draft.

No. 2. A ten-day sight draft that has been accepted.

No. 2. A ten-day sight draft that has been accepted.

No. 3. An accepted sight draft.

No. 3. An accepted sight draft.

No. 4. A time draft.

No. 4. A time draft.

[30]An accepted draft is really a promissory note, though it is more often called an acceptance. When a man pays or accepts a draft he is said to honour it. In the foregoing illustration A is not obliged either to pay or to accept the draft. It is not binding upon him any more than a letter would be. He can refuse payment just as easily and as readily as he could decline to pay a collector who calls for payment of a bill. Of course, if a man habitually refuses to honour legitimate drafts it may injure his credit with banks and business houses.

[30]An accepted draft is basically a promissory note, although it's more commonly referred to as an acceptance. When someone pays or accepts a draft, it's said that they honour it. In the previous example, A is not required to pay or accept the draft. It's not binding on him any more than a letter would be. He can refuse to pay just as easily as he could turn down a collector asking for payment of a bill. However, if someone consistently refuses to honour legitimate drafts, it could hurt their credit with banks and businesses.

It is a very common thing to collect distant accounts by means of commercial drafts. A debtor is more likely to meet—that is, to pay—a draft than he is to reply to a letter and inclose his cheque. It is really more convenient, and safer, too, for there is some risk in sending personal cheques through the mail. There are some houses that make all their payments by cheques, while there are others which prefer to have their creditors at a distance draw on them for the amounts due.

It’s quite common to collect payments from far away using commercial drafts. A debtor is more likely to pay a draft than to respond to a letter and include a check. It’s actually more convenient and safer, as sending personal checks through the mail carries some risk. Some companies handle all their payments by checks, while others prefer to let their creditors draw on them for what’s owed.

If a business man who has been accustomed to honour drafts continues for a period to dishonour them, the banks through which the drafts pass naturally conclude that he is unable to meet his liabilities.

If a businessman who is used to honoring drafts suddenly starts dishonoring them for a while, the banks handling those drafts will naturally assume he can't meet his obligations.

Some houses deposit their drafts for collection in their[31] home banks, while others have a custom of sending them direct to some bank in or near the place where the debtor resides. If the place is a very small one the collection is sometimes made through one of the express companies.

Some companies send their drafts for collection to their[31] home banks, while others prefer to send them directly to a bank in or near where the debtor lives. In very small towns, collection is sometimes handled by one of the express companies.

When goods are sold for distinct periods of credit, and it is generally understood that maturing accounts are subject to sight drafts, there should be no need of notifying the debtor in advance. Some houses, however, make a general custom of sending notices ten days in advance, stating that a draft will be drawn if cheque is not received in the meantime.

When items are sold on credit for specific time periods, and it's commonly understood that due accounts are subject to sight drafts, there shouldn't be a need to notify the debtor beforehand. Some businesses, however, have a standard practice of sending notices ten days in advance, indicating that a draft will be issued if payment isn't received in the meantime.

Notice the illustrations. The protest notice at the left of Nos. 1, 2, and 4 is intended for the bank presenting the draft for payment. The reason for this will be fully explained in our lesson on protested paper. (See Lesson XIII.) No. 2 shows an accepted draft payable to the order of a bank in the city upon which it is drawn. No. 1 is payable to the order of a bank in the city of the drawer. No. 3 is a sight draft payable to the order of a bank and accepted payable at a bank. No. 4 is a time draft payable to "ourselves"—that is, the Pennsylvania Steel Company.

Notice the illustrations. The protest notice on the left of Nos. 1, 2, and 4 is meant for the bank presenting the draft for payment. The reason for this will be fully explained in our lesson on protested paper. (See Lesson 13.) No. 2 shows an accepted draft payable to the order of a bank in the city where it is drawn. No. 1 is payable to the order of a bank in the drawer’s city. No. 3 is a sight draft payable to the order of a bank and accepted for payment at a bank. No. 4 is a time draft payable to "ourselves"—that is, the Pennsylvania Steel Company.

Drafts are often discounted at banks before acceptance where the credit of the drawer is good. In such cases the drafts which are dishonoured are charged up against the drawer's account.

Drafts are often ignored at banks before they’re accepted if the drawer's credit is solid. In these situations, the drafts that are rejected are charged to the drawer's account.

X. FOREIGN EXCHANGE

It is quite in order that we should follow lessons on the clearing-house and commercial drafts with a lesson on foreign exchange.

It makes sense for us to follow lessons on the clearinghouse and business drafts with a lesson on foreign exchange.

We learned in the last lesson that commercial drafts are made use of to facilitate the collection of accounts.[32] They are simply formal demands for the payment of legitimate debts. When these formal demands are made upon foreign debtors they are called bills of exchange; and the process of buying and selling these drafts, the drafts themselves, and the fluctuations in price, all are included in the general name exchange.

We learned in the last lesson that commercial drafts are used to help collect accounts.[32] They are basically formal requests for the payment of valid debts. When these formal requests are made to foreign debtors, they are called bills of exchange; and the process of buying and selling these drafts, the drafts themselves, and the price changes, are all included under the general term exchange.

Currency exchange.

Currency exchange.

To illustrate the principles of exchange let us suppose that the following transactions have occurred:

To show how the principles of exchange work, let's say that these transactions have taken place:

- C of Boston has sold goods, £2000, to H of Hamburg.

- D of Chicago has sold goods, £5000, to F of Glasgow.

- M of Chicago has sold goods, £3000, to K of London.

- E of Philadelphia has sold goods, £6000, to R of Paris.

- P of New York has sold goods, £1000, to G of Paris.

C draws on H for £2000, sells the draft to a banking-house in Boston; they send to Bank A of New York, and[33] the New York bank to their London correspondent, say Bank B, with instructions to collect from Hamburg.

C takes a loan from H for £2000, sells the draft to a bank in Boston; they send it to Bank A in New York, and[33] the New York bank to their London correspondent, let's say Bank B, with orders to collect from Hamburg.

D draws in a similar way on F. E draws on R, and P on G. Suppose that M instead of drawing on K receives a draft drawn by Bank B of London on Bank A of New York, payable to M's order.

D draws in a similar way on F. E draws on R, and P on G. Suppose that M, instead of drawing on K, receives a draft drawn by Bank B of London on Bank A of New York, payable to M's order.

America has sold goods worth £17,000 to Europe.

U.S. has sold products valued at £17,000 to Europe.

Europe . . . . . . owes £17,000 to . . . . . America

Europe . . . . . . owes £17,000 to . . . . . USA

But B has paid A £3000.

But B has paid A £3,000.

____________

____________

B . . . . . . therefore owes £14,000 to . . . . . . A

B . . . . . . therefore owes £14,000 to . . . . . . A

Now it will cost B a considerable sum of money to ship £14,000 in gold to A, for all exchanges between Europe and America are payable in gold. Suppose that S of New York owes T of London £14,000, and T draws on S and takes the draft to Bank B in London and offers it for sale. Will B offer more or less than £14,000 for the bill of exchange or draft? He will offer more. It will be cheaper for him to pay a premium for the draft than to ship gold, for he can send this draft to Bank A to pay his indebtedness, and A can collect from S.

Now it will cost B a significant amount of money to ship £14,000 in gold to A, since all transactions between Europe and America are done in gold. Let’s say S in New York owes T in London £14,000. If T draws a draft on S and takes it to Bank B in London to sell it, will B offer more or less than £14,000 for that draft? He will offer more. It will be cheaper for him to pay a premium for the draft than to ship gold, because he can send this draft to Bank A to settle his debt, and A can collect from S.

In the money market in New York there is a constant supply of exchanges (drafts) on London, and in London a constant supply of exchanges on New York.

In the New York money market, there's a steady supply of exchanges (drafts) on London, and in London, there's a steady supply of exchanges on New York.

Experience has shown that at all times the number of persons in Europe indebted to American business houses is about (though of course not actually) the same as the number of persons in America indebted to European houses. Hence when A of New York wishes to make a payment to B of London he does not send the actual money, but goes into the market—that is, to a banker doing a foreign business—and buys a draft, called a bill of exchange, which is in reality the banker's order on his London correspondent, asking the latter to pay the money to the person named. It may be that[34] about the same time some London merchant who owes money in New York goes to the very same London banker and buys a draft on the New York bank. In this way the one draft cancels the other, and when there is a difference at the end of the week or month the actual gold is sent across to balance the account.

Experience has shown that at any given time, the number of people in Europe who owe money to American businesses is roughly (though not precisely) the same as the number of people in America who owe money to European businesses. So, when A from New York wants to pay B in London, he doesn’t send actual cash; instead, he goes to the market—specifically, a banker that deals in foreign transactions—and buys a draft, known as a bill of exchange. This is essentially the banker's request to his London counterpart to pay the specified amount to the named individual. Meanwhile, it’s possible that around the same time, some merchant in London who owes money in New York heads to that same London banker and purchases a draft for the New York bank. In this way, one draft offsets the other, and any difference at the end of the week or month is settled by sending gold across to balance the account.

These exchanges have a sort of commodity value, and like all commodities, depend upon the law of supply and demand. When gold is being shipped abroad we say that the balance of trade is against us—that is, we are buying more from Europe than Europe is buying from us, and the gold is shipped to pay the balance or difference.