This is a modern-English version of Cyclopedia of Commerce, Accountancy, Business Administration, v. 04 (of 10), originally written by American School of Correspondence.

It has been thoroughly updated, including changes to sentence structure, words, spelling,

and grammar—to ensure clarity for contemporary readers, while preserving the original spirit and nuance. If

you click on a paragraph, you will see the original text that we modified, and you can toggle between the two versions.

Scroll to the bottom of this page and you will find a free ePUB download link for this book.

THE BUSY RETAIL STORE OF THE L. E. WATERMAN COMPANY

At the "Pen Corner," 173 Broadway, New York City

THE BUSY RETAIL STORE OF THE L. E. WATERMAN COMPANY

At "Pen Corner," 173 Broadway, New York City

Cyclopedia

of

of

Commerce, Accountancy,

Business Administration

Commerce, Accounting,

Business Management

Volume 4

Volume 4

A General Reference Work on

A General Reference Guide on

ACCOUNTING, AUDITING, BOOKKEEPING, COMMERCIAL LAW, BUSINESS

MANAGEMENT, ADMINISTRATIVE AND INDUSTRIAL ORGANIZATION,

BANKING, ADVERTISING, SELLING, OFFICE AND FACTORY

RECORDS, COST KEEPING, SYSTEMATIZING, ETC.

ACCOUNTING, AUDITING, BOOKKEEPING, COMMERCIAL LAW, BUSINESS

MANAGEMENT, ADMINISTRATIVE AND INDUSTRIAL ORGANIZATION,

BANKING, ADVERTISING, SELLING, OFFICE AND FACTORY

RECORDS, COST KEEPING, SYSTEMATIZING, ETC.

Prepared by a Corps of

Prepared by a team of

AUDITORS, ACCOUNTANTS, ATTORNEYS, AND SPECIALISTS IN BUSINESS METHODS AND MANAGEMENT

AUDITORS, ACCOUNTANTS, LAWYERS, AND BUSINESS METHODS AND MANAGEMENT SPECIALISTS

Illustrated with Over Two Thousand Engravings

Illustrated with More Than Two Thousand Images

TEN VOLUMES

10 volumes

CHICAGO

AMERICAN TECHNICAL SOCIETY

1910

CHICAGO

AMERICAN TECHNICAL SOCIETY

1910

Copyright, 1909

Copyright, 1909

BY

BY

AMERICAN SCHOOL OF CORRESPONDENCE

AMERICAN SCHOOL OF CORRESPONDENCE

Copyright, 1909

Copyright, 1909

BY

BY

AMERICAN TECHNICAL SOCIETY

AMERICAN TECHNICAL SOCIETY

Entered at Stationers' Hall, London

All Rights Reserved

Entered at Stationers' Hall, London

All Rights Reserved

Authors and Collaborators

JAMES BRAY GRIFFITH, Managing Editor

JAMES BRAY GRIFFITH, Managing Editor

Head, Dept. of Commerce, Accountancy, and Business Administration, American School of Correspondence.

Head, Department of Commerce, Accounting, and Business Administration, American School of Correspondence.

ROBERT H. MONTGOMERY

ROBERT H. MONTGOMERY

Of the Firm of Lybrand, Ross Bros. & Montgomery, Certified Public Accountants.

Of the firm Lybrand, Ross Bros. & Montgomery, Certified Public Accountants.

Editor of the American Edition of Dicksee's Auditing.

Editor of the American Edition of Dicksee's Auditing.

Formerly Lecturer on Auditing at the Evening School of Accounts and Finance of the University of Pennsylvania, and the School of Commerce, Accounts, and Finance of the New York University.

Former Lecturer on Auditing at the Evening School of Accounts and Finance at the University of Pennsylvania, and at the School of Commerce, Accounts, and Finance at New York University.

ARTHUR LOWES DICKINSON, F. C. A., C. P. A.

ARTHUR LOWES DICKINSON, F.C.A., C.P.A.

Of the Firms of Jones, Caesar, Dickinson, Wilmot & Company, Certified Public Accountants, and Price, Waterhouse & Company, Chartered Accountants.

Of the firms of Jones, Caesar, Dickinson, Wilmot & Company, Certified Public Accountants, and Price, Waterhouse & Company, Chartered Accountants.

WILLIAM M. LYBRAND, C. P. A.

WILLIAM M. LYBRAND, CPA

Of the Firm of Lybrand, Ross Bros. & Montgomery, Certified Public Accountants.

Of the firm Lybrand, Ross Bros. & Montgomery, Certified Public Accountants.

F. H. MACPHERSON, C. A., C. P. A.

F. H. MACPHERSON, C. A., C. P. A.

Of the Firm of F. H. Macpherson & Co., Certified Public Accountants.

Of the firm F. H. Macpherson & Co., Certified Public Accountants.

CHAS. A. SWEETLAND

CHAS. A. SWEETLAND

Consulting Public Accountant.

Public Accountant Consultant.

Author of "Loose-Leaf Bookkeeping," and "Anti-Confusion Business Methods."

Author of "Loose-Leaf Bookkeeping" and "Anti-Confusion Business Methods."

E. C. LANDIS

E.C. Landis

Of the System Department, Burroughs Adding Machine Company.

Of the System Department, Burroughs Adding Machine Company.

HARRIS C. TROW, S. B.

Harris C. Trow, S.B.

Editor-in-Chief, Textbook Department, American School of Correspondence.

Editor-in-Chief, Textbook Department, American School of Correspondence.

CECIL B. SMEETON, F. I. A.

CECIL B. SMEETON, F. I. A.

Public Accountant and Auditor.

Public Accountant & Auditor.

President, Incorporated Accountants' Society of Illinois.

President, Incorporated Accountants' Society of Illinois.

Fellow, Institute of Accounts, New York.

Fellow, Institute of Accountants, New York.

JOHN A. CHAMBERLAIN, A. B., LL. B.

JOHN A. CHAMBERLAIN, B.A., J.D.

Of the Cleveland Bar.

Cleveland Bar Association.

Lecturer on Suretyship, Western Reserve Law School.

Lecturer on Suretyship, Western Reserve Law School.

Author of "Principles of Business Law."

Author of "Principles of Business Law."

HUGH WRIGHT

Hugh Wright

Auditor, Westlake Construction Company.

Auditor, Westlake Construction Co.

GLENN M. HOBBS, Ph. D.

GLENN M. HOBBS, Ph.D.

Secretary, American School of Correspondence.

Secretary, American Correspondence School.

JESSIE M. SHEPHERD, A. B.

JESSIE M. SHEPHERD, A.B.

Associate Editor, Textbook Department, American School of Correspondence.

Associate Editor, Textbook Department, American School of Correspondence.

GEORGE C. RUSSELL

GEORGE C. RUSSELL

Systematizer.

Organizer.

Formerly Manager, System Department, Elliott-Fisher Company.

Formerly Manager, Systems Department, Elliott-Fisher Company.

OSCAR E. PERRIGO, M. E.

OSCAR E. PERRIGO, M.E.

Specialist in Industrial Organization.

Industrial Organization Specialist.

Author of "Machine-Shop Economics and Systems," etc.

Author of "Machine-Shop Economics and Systems," etc.

DARWIN S. HATCH, B. S.

DARWIN S. HATCH, B.S.

Assistant Editor, Textbook Department, American School of Correspondence.

Assistant Editor, Textbook Department, American School of Correspondence.

CHAS. E. HATHAWAY

CHAS. E. HATHAWAY

Cost Expert.

Cost Specialist.

Chief Accountant, Fore River Shipbuilding Co.

Chief Accountant, Fore River Shipbuilding Co.

CHAS. WILBUR LEIGH, B. S.

CHAS. WILBUR LEIGH, B.S.

Associate Professor of Mathematics, Armour Institute of Technology.

Associate Professor of Mathematics, Armour Institute of Technology.

L. W. LEWIS

L. W. Lewis

Advertising Manager, The McCaskey Register Co.

Advertising Manager, The McCaskey Register Co.

MARTIN W. RUSSELL

MARTIN W. RUSSELL

[4]Registrar and Treasurer, American School of Correspondence.

[4]Registrar and Treasurer, American School of Correspondence.

HALBERT P. GILLETTE, C. E.

HALBERT P. GILLETTE, C.E.

Managing Editor, Engineering-Contracting.

Managing Editor, Engineering-Contracting.

Author of "Handbook of Cost Data for Contractors and Engineers."

Author of "Handbook of Cost Data for Contractors and Engineers."

R. T. MILLER, JR., A. M., LL. B.

R. T. MILLER, JR., A.M., J.D.

President, American School of Correspondence.

President, American School of Online Learning.

WILLIAM SCHUTTE

WILLIAM SCHUTTE

Manager of Advertising, National Cash Register Co.

Manager of Advertising, National Cash Register Company

E. ST. ELMO LEWIS

E. St. Elmo Lewis

Advertising Manager, Burroughs Adding Machine Company.

Advertising Manager, Burroughs Adding Machine Company.

Author of "The Credit Man and His Work" and "Financial Advertising."

Author of "The Credit Man and His Work" and "Financial Advertising."

RICHARD T. DANA

RICHARD T. DANA

Consulting Engineer.

Consultant Engineer.

Chief Engineer, Construction Service Co.

Chief Engineer, Construction Services LLC

P. H. BOGARDUS

P. H. BOGARDUS

Publicity Manager, American School of Correspondence.

Publicity Manager, American School of Correspondence.

WILLIAM G. NICHOLS

WILLIAM G. NICHOLS

General Manufacturing Agent for the China Mfg. Co., The Webster Mfg. Co., and the Pembroke Mills.

General Manufacturing Agent for China Mfg. Co., The Webster Mfg. Co., and Pembroke Mills.

Author of "Cost Finding" and "Cotton Mills."

Author of "Cost Finding" and "Cotton Mills."

C. H. HUNTER

C. H. Hunter

Advertising Manager, Elliott-Fisher Co.

Advertising Manager, Elliott-Fisher Co.

FRANK C. MORSE

FRANK C. MORSE

Filing Expert.

Filing Specialist.

Secretary, Browne-Morse Co.

Secretary, Browne-Morse Co.

H. E. K'BERG

H.E. K'BERG

Expert on Loose-Leaf Systems.

Loose-Leaf Systems Expert.

Formerly Manager, Business Systems Department, Burroughs Adding Machine Co.

Formerly Manager of the Business Systems Department at Burroughs Adding Machine Co.

EDWARD B. WAITE

EDWARD B. WAITE

Head, Instruction Department, American School of Correspondence.

Head, Instruction Department, American School of Correspondence.

Authorities Consulted

The editors have freely consulted the standard technical and business literature of America and Europe in the preparation of these volumes. They desire to express their indebtedness, particularly, to the following eminent authorities, whose well-known treatises should be in the library of everyone interested in modern business methods.

The editors have freely referenced the standard technical and business literature from America and Europe while preparing these volumes. They want to acknowledge their debt, especially to the following respected authorities, whose well-known works should be in the library of anyone interested in modern business practices.

Grateful acknowledgment is made also of the valuable service rendered by the many manufacturers and specialists in office and factory methods, whose coöperation has made it possible to include in these volumes suitable illustrations of the latest equipment for office use; as well as those financial, mercantile, and manufacturing concerns who have supplied illustrations of offices, factories, shops, and buildings, typical of the commercial and industrial life of America.

Grateful acknowledgment is made also of the valuable service provided by the many manufacturers and specialists in office and factory methods, whose cooperation has made it possible to include in these volumes suitable illustrations of the latest equipment for office use; as well as those financial, mercantile, and manufacturing companies that have supplied illustrations of offices, factories, shops, and buildings, typical of the commercial and industrial life of America.

JOSEPH HARDCASTLE, C. P. A.

JOSEPH HARDCASTLE, CPA

Formerly Professor of Principles and Practice of Accounts, School of Commerce, Accounts, and Finance, New York University.

Formerly a Professor of Principles and Practice of Accounting at the School of Commerce, Accounts, and Finance, New York University.

Author of "Accounts of Executors and Testamentary Trustees."

Author of "Accounts of Executors and Estate Trustees."

HORACE LUCIAN ARNOLD

HORACE LUCIAN ARNOLD

Specialist in Factory Organization and Accounting.

Specialist in Factory Management and Accounting.

Author of "The Complete Cost Keeper," and "Factory Manager and Accountant."

Author of "The Complete Cost Keeper" and "Factory Manager and Accountant."

JOHN F. J. MULHALL, P. A.

JOHN F. J. MULHALL, P. A.

Specialist in Corporation Accounts.

Corporation Accounts Specialist.

Author of "Quasi Public Corporation Accounting and Management."

Author of "Quasi Public Corporation Accounting and Management."

SHERWIN CODY

SHERWIN CODY

Advertising and Sales Specialist.

Ads and Sales Specialist.

Author of "How to Do Business by Letter," and "Art of Writing and Speaking the English Language."

Author of "How to Do Business by Letter" and "Art of Writing and Speaking the English Language."

FREDERICK TIPSON, C. P. A.

FREDERICK TIPSON, CPA

Author of "Theory of Accounts."

Author of "Theory of Accounts."

CHARLES BUXTON GOING

CHARLES BUXTON IS LEAVING

Managing Editor of The Engineering Magazine.

Managing Editor of *The Engineering Magazine*.

Associate in Mechanical Engineering, Columbia University.

Associate in Mechanical Engineering, Columbia University.

Corresponding Member, Canadian Mining Institute.

Corresponding Member, Canadian Mining Institute.

F. E. WEBNER

F. E. WEBNER

Public Accountant.

Public Accountant.

Specialist in Factory Accounting.

Factory Accounting Specialist.

[6]Contributor to The Engineering Press.

Contributor to The Engineering Press.

AMOS K. FISKE

AMOS K. FISKE

Associate Editor of the New York Journal of Commerce.

Associate Editor of the New York Journal of Commerce.

Author of "The Modern Bank."

Author of "The Modern Bank."

JOSEPH FRENCH JOHNSON

Joseph French Johnson

Dean of the New York University School of Commerce, Accounts, and Finance.

Dean of the NYU School of Business, Accounting, and Finance.

Editor, The Journal of Accountancy.

Editor, The Journal of Accountancy.

Author of "Money, Exchange, and Banking."

Author of "Money, Exchange, and Banking."

M. U. OVERLAND

M. U. Overland

Of the New York Bar.

Of the New York State Bar.

Author of "Classified Corporation Laws of All the States."

Author of "Classified Corporation Laws of All the States."

THOMAS CONYNGTON

THOMAS CONYNGTON

Of the New York Bar.

Of the New York State Bar.

Author of "Corporate Management," "Corporate Organization," "The Modern Corporation," and "Partnership Relations."

Author of "Corporate Management," "Corporate Organization," "The Modern Corporation," and "Partnership Relations."

THEOPHILUS PARSONS, LL. D.

THEOPHILUS PARSONS, Ph.D.

Author of "The Laws of Business."

Author of "The Laws of Business."

E. ST. ELMO LEWIS

E. St. Elmo Lewis

Advertising Manager, Burroughs Adding Machine Company.

Advertising Manager, Burroughs Adding Machine Company.

Formerly Manager of Publicity, National Cash Register Co.

Formerly the Publicity Manager at National Cash Register Co.

Author of "The Credit Man and His Work," and "Financial Advertising."

Author of "The Credit Man and His Work" and "Financial Advertising."

T. E. YOUNG, B. A., F. R. A. S.

T. E. YOUNG, B. A., F. R. A. S.

Ex-President of the Institute of Actuaries.

Ex-President of the Institute of Actuaries.

Member of the Actuary Society of America.

Member of the American Society of Actuaries.

Author of "Insurance."

Author of "Insurance."

LAWRENCE R. DICKSEE, F. C. A.

LAWRENCE R. DICKSEE, F. C. A.

Professor of Accounting at the University of Birmingham.

Professor of Accounting at the University of Birmingham.

Author of "Advanced Accounting," "Auditing," "Bookkeeping for Company Secretary," etc.

Author of "Advanced Accounting," "Auditing," "Bookkeeping for Company Secretary," and more.

FRANCIS W. PIXLEY

FRANCIS W. PIXLEY

Author of "Auditors, Their Duties and Responsibilities," and "Accountancy."

Author of "Auditors, Their Duties and Responsibilities," and "Accountancy."

CHARLES U. CARPENTER

CHARLES U. CARPENTER

General Manager, The Herring-Hall-Marvin Safe Co.

General Manager, The Herring-Hall-Marvin Safe Company.

Formerly General Manager, National Cash Register Co.

Formerly General Manager, National Cash Register Co.

[7]Author of "Profit Making Management."

Author of "Profit-Making Management."

C. E. KNOEPPEL

C. E. KNOEPPEL

Specialist in Cost Analysis and Factory Betterment.

Specialist in Cost Analysis and Factory Improvement.

Author of "Systematic Foundry Operation and Foundry Costing," "Maximum Production through Organization and Supervision," and other papers.

Author of "Systematic Foundry Operation and Foundry Costing," "Maximum Production through Organization and Supervision," and various other articles.

HARRINGTON EMERSON, M. A.

Harrington Emerson, M.A.

Consulting Engineer.

Consultant Engineer.

Director of Organization and Betterment Work on the Santa Fe System.

Director of Organization and Improvement Work on the Santa Fe System.

Originator of the Emerson Efficiency System.

Originator of the Emerson Efficiency System.

Author of "Efficiency as a Basis for Operation and Wages."

Author of "Efficiency as a Foundation for Operations and Pay."

ELMER H. BEACH

ELMER H. BEACH

Specialist in Accounting Methods.

Accounting Methods Specialist.

Editor, Beach's Magazine of Business.

Editor, Beach's Business Magazine.

Founder of The Bookkeeper.

Founder of The Bookkeeper.

Editor of The American Business and Accounting Encyclopedia.

Editor of The American Business and Accounting Encyclopedia.

J. J. RAHILL, C. P. A.

J. J. RAHILL, C. P. A.

Member, California Society of Public Accountants.

Member, California Society of Public Accountants.

Author of "Corporation Accounting and Corporation Law."

Author of "Corporate Accounting and Corporate Law."

FRANK BROOKER, C. P. A.

FRANK BROOKER, CPA

Ex-New York State Examiner of Certified Public Accountants.

Former New York State CPA Examiner.

Ex-President, American Association of Public Accountants.

Ex-President, American Association of Public Accountants.

Author of "American Accountants' Manual."

Author of "American Accountants Manual."

CLINTON E. WOODS, M. E.

CLINTON E. WOODS, M.E.

Specialist in Industrial Organization.

Industrial Organization Specialist.

Formerly Comptroller, Sears, Roebuck & Co.

Formerly Controller, Sears, Roebuck & Co.

Author of "Organizing a Factory," and "Woods' Reports."

Author of "Organizing a Factory" and "Woods' Reports."

CHARLES E. SPRAGUE, C. P. A.

CHARLES E. SPRAGUE, CPA

President of the Union Dime Savings Bank, New York.

President of the Union Dime Savings Bank, New York.

Author of "The Accountancy of Investment," "Extended Bond Tables," and "Problems and Studies in the Accountancy of Investment."

Author of "The Accountancy of Investment," "Extended Bond Tables," and "Problems and Studies in the Accountancy of Investment."

CHARLES WALDO HASKINS, C. P. A., L. H. M.

CHARLES WALDO HASKINS, CPA, LHM

Author of "Business Education and Accountancy."

Author of "Business Education and Accounting."

JOHN J. CRAWFORD

JOHN J. CRAWFORD

Author of "Bank Directors, Their Powers, Duties, and Liabilities."

Author of "Bank Directors, Their Powers, Duties, and Liabilities."

DR. F. A. CLEVELAND

Dr. F.A. Cleveland

Of the Wharton School of Finance, University of Pennsylvania.

Of the Wharton School of Finance, University of Pennsylvania.

Author of "Funds and Their Uses."

Author of "Funds and Their Uses."

CHICAGO SALES AND DISPLAY ROOMS OF THE NEW HAVEN CLOCK COMPANY

CHICAGO SALES AND DISPLAY ROOMS OF THE NEW HAVEN CLOCK COMPANY

Foreword

With the unprecedented increase in our commercial activities has come a demand for better business methods. Methods which were adequate for the business of a less active commercial era, have given way to systems and labor-saving ideas in keeping with the financial and industrial progress of the world.

With the massive growth in our business activities, there's a need for better business practices. The methods that worked during a less active commercial time have been replaced by systems and labor-saving ideas that match the financial and industrial advancements of the world.

Out of this progress has risen a new literature—the literature of business. But with the rapid advancement in the science of business, its literature can scarcely be said to have kept pace, at least, not to the same extent as in other sciences and professions. Much excellent material dealing with special phases of business activity has been prepared, but this is so scattered that the student desiring to acquire a comprehensive business library has found himself confronted by serious difficulties. He has been obliged, to a great extent, to make his selections blindly, resulting in many duplications of material without securing needed information on important phases of the subject.

Out of this progress has emerged a new type of literature—the literature of business. However, with the rapid advancements in the field of business, its literature hasn't really kept up, at least not to the same degree as other fields and professions. While there's a lot of great material covering specific aspects of business activities, it's so scattered that anyone looking to build a comprehensive business library faces significant challenges. They've often had to choose resources without clear guidance, which has led to a lot of duplicated content without obtaining essential information on important topics.

In the belief that a demand exists for a library which shall embrace the best practice in all branches of business—from buying to selling, from simple bookkeeping to the administration of the financial affairs of a great corporation—these volumes have been prepared. Prepared primarily for[9] use as instruction books for the American School of Correspondence, the material from which the Cyclopedia has been compiled embraces the latest ideas with explanations of the most approved methods of modern business.

In the belief that there is a need for a library that covers the best practices in all areas of business—from purchasing to sales, from basic bookkeeping to managing the financial operations of a large corporation—these volumes have been created. They are mainly designed to serve as instructional books for[9] the American School of Correspondence. The content used to compile the Cyclopedia includes the latest concepts along with explanations of the most effective modern business methods.

Editors and writers have been selected because of their familiarity with, and experience in handling various subjects pertaining to Commerce, Accountancy, and Business Administration. Writers with practical business experience have received preference over those with theoretical training; practicability has been considered of greater importance than literary excellence.

Editors and writers have been chosen for their knowledge and experience in dealing with various topics related to Commerce, Accountancy, and Business Administration. Writers with hands-on business experience have been prioritized over those with purely theoretical training; practical skills have been deemed more important than literary quality.

In addition to covering the entire general field of business, this Cyclopedia contains much specialized information not heretofore published in any form. This specialization is particularly apparent in those sections which treat of accounting and methods of management for Department Stores, Contractors, Publishers and Printers, Insurance, and Real Estate. The value of this information will be recognized by every student of business.

In addition to covering the entire general field of business, this Cyclopedia contains a lot of specialized information that hasn’t been published before. This specialization is especially noticeable in the sections that focus on accounting and management methods for department stores, contractors, publishers and printers, insurance, and real estate. Every business student will appreciate the value of this information.

The principal value which is claimed for this Cyclopedia is as a reference work, but, comprising as it does the material used by the School in its correspondence courses, it is offered with the confident expectation that it will prove of great value to the trained man who desires to become conversant with phases of business practice with which he is unfamiliar, and to those holding advanced clerical and managerial positions.

The main value of this Cyclopedia is as a reference resource. However, since it includes the content used by the School in its correspondence courses, it is presented with the strong belief that it will be highly valuable to professionals looking to get familiar with aspects of business practice they don’t know yet, as well as to those in senior clerical and managerial roles.

In conclusion, grateful acknowledgment is made to authors and collaborators, to whose hearty cooperation the excellence of this work is due.

In conclusion, we sincerely thank the authors and collaborators, whose enthusiastic support made the quality of this work possible.

Table of Contents

(For professional standing of authors, see list of Authors and Collaborators at front of volume.)

(For the professional status of authors, see the list of Authors and Collaborators at the beginning of the volume.)

VOLUME IV

Volume 4

| Accounting Theory | By James B. Griffith | Page __A_TAG_PLACEHOLDER_0__ |

| Dictionary of Commercial Terms—Commercial Abbreviations—Objects of Bookkeeping—Methods—Single Entry—Double Entry—Advantages of Double Entry —Classes of Account Books—Recording Transactions—Promissory Notes—Bank Deposits—Sample Transactions—Classes of Accounts—Classes of Assets—Revenue Accounts—Rules for Journalizing—Rules for Posting—Trial Balance—Sample Ledger Accounts—Treatment of Cash Discounts—Profit and Loss—Merchandise Inventory Accounts—Balance Sheet—Journalizing Notes—Journalizing Drafts | ||

| Sole Proprietorship and Partnership Accounts | By James B. Griffith | Page __A_TAG_PLACEHOLDER_0__ |

| Retail Business—Proprietors' Accounts—Inventory—Retail Coal Books— Uncollectible Accounts—Sales Tickets—Departmental Records—Partnership Agreements—Kinds of Partners—Participation in Profits—Interest on Investments—Capital and Personal Accounts—Opening and Closing Partnership Books—Model Set of Books | ||

| Corporate and Manufacturing Accounts | By James B. Griffith | Page __A_TAG_PLACEHOLDER_0__ |

| Classification of Corporations—Joint Stock Company—Creation of Corporation —Stockholders—Stock Certificates—Capitalization—Capital and Capital Stock —Stock Subscriptions—Management of Corporations—Powers of Directors and Officers—Dividends—Closing Transfer Books—Sale of Stock Below Par—Corporation Bookkeeping—Books Required—Opening Entries—Changing Books from Partnership to Corporation—Stock Donated to Employes—Reserves—Computing Sinking Funds—Premium and Interest on Bonds—Manufacturing and Cost Accounts—Factory Assets—Factory Expenses—Balance Ledger | ||

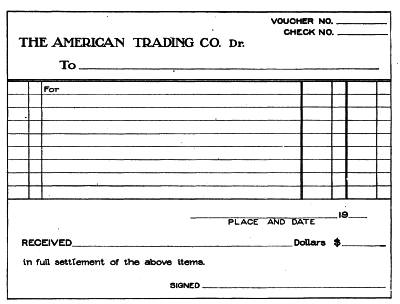

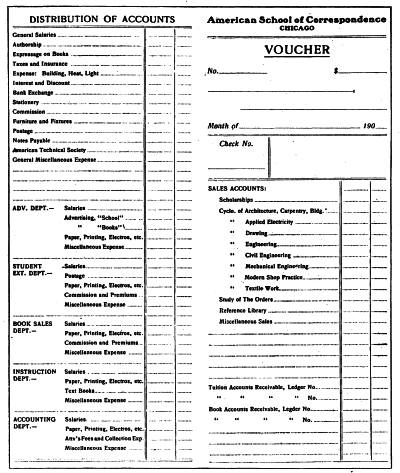

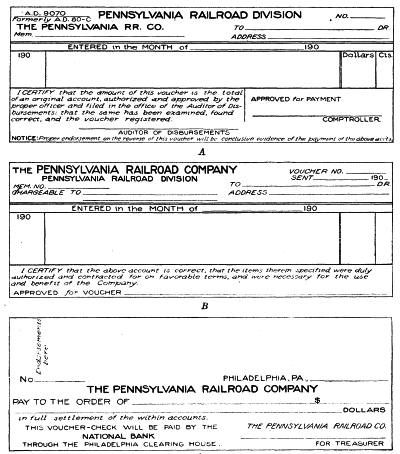

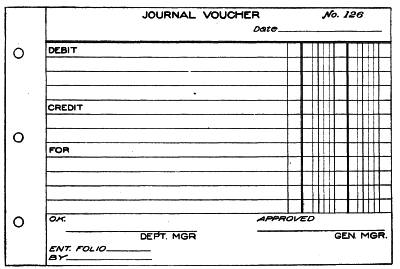

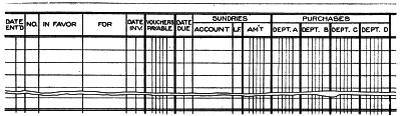

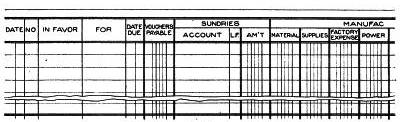

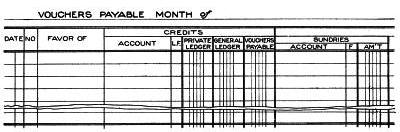

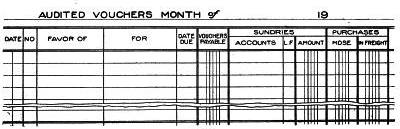

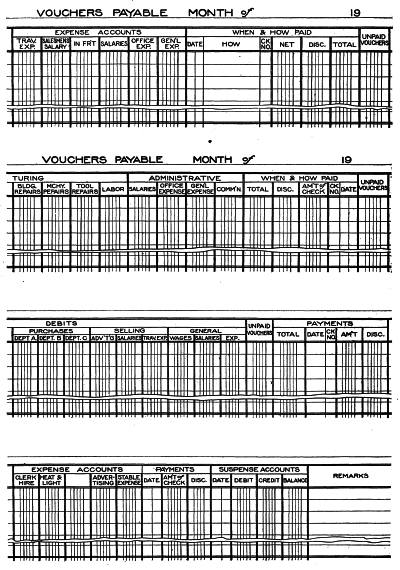

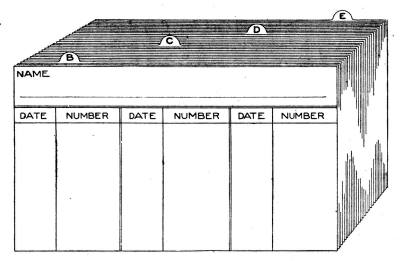

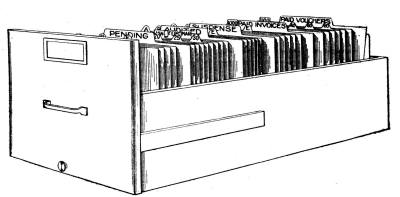

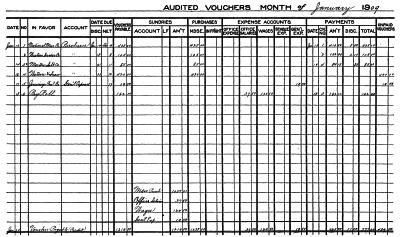

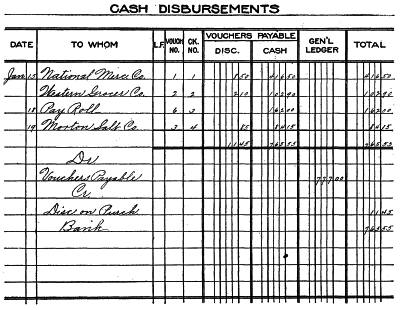

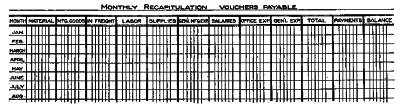

| The Voucher Accounting System | By James B. Griffith | Page __A_TAG_PLACEHOLDER_0__ |

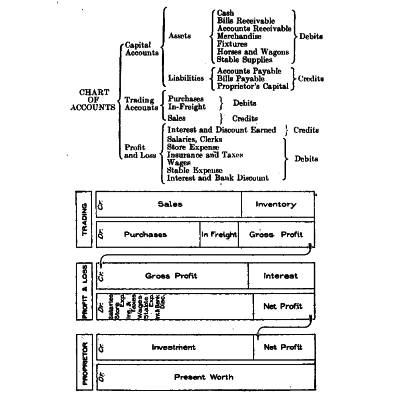

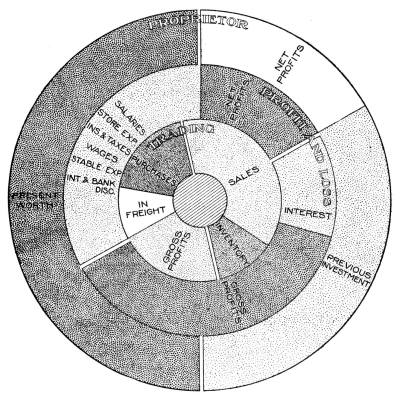

| Use of Vouchers—Voucher Checks—Journal Vouchers—Voucher Register— Operation of System—Auditing Invoices—Executing Vouchers—Paying, Filing, and Indexing Vouchers—Voucher File—Demonstration of System—Voucher Accounting—Unit System—Combined Purchase Ledger and Invoice File—Private Ledger—Private Journal—General Ledger—Manufacturing Accounts—Charting Accounts—Chart of Trading Business—Chart of Manufacturing Accounts—Examples of Charts—Explanation of Charts | ||

| Review Questions | Page __A_TAG_PLACEHOLDER_0__ | |

| Index | Page __A_TAG_PLACEHOLDER_0__ | |

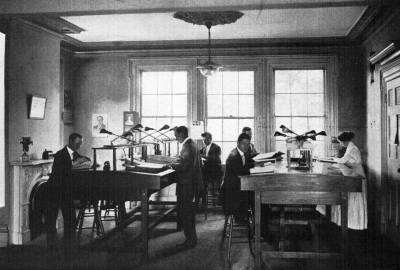

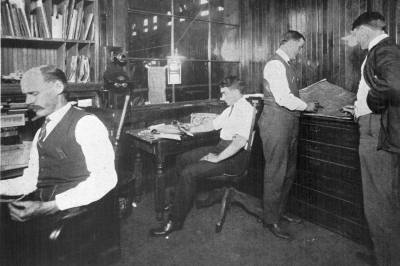

THE ACCOUNTING DEPARTMENT IN THE OFFICES OF THE GREEN FUEL ECONOMIZER COMPANY, MATTEAWAN, N. Y.

THE ACCOUNTING DEPARTMENT IN THE OFFICES OF THE GREEN FUEL ECONOMIZER COMPANY, MATTEAWAN, NY.

THEORY OF ACCOUNTS

PART I

Like every other special branch of study, the Theory and Practice of Accounts has its own special vocabulary of technical terms. In all literature of accounting and business methods in general, these terms are frequently employed; and the student will find it not only advantageous, but in fact absolutely necessary, to familiarize himself thoroughly with their use.

Like every other specialized field, the Theory and Practice of Accounts has its own unique set of technical terms. In all accounting and business literature, these terms are commonly used; and students will find it not only helpful but actually essential to become well-acquainted with their usage.

The commercial terms and definitions in the following list are the ones most commonly used in business. Great care has been exercised in preparing a list that is practical and in making the definitions clear.

The commercial terms and definitions in the list below are the ones most frequently used in business. Care has been taken to create a practical list and to ensure the definitions are clear.

DICTIONARY OF COMMERCIAL TERMS

Business Terms Dictionary

Acceptance—When a draft or bill of exchange is presented to the payer, he writes across the face "Accepted" or "Accepted for payment at ..." and signs his name. It is then termed an acceptance.

Acceptance—When a draft or bill of exchange is presented to the payer, he writes across the front "Accepted" or "Accepted for payment at ..." and signs his name. It is then called an acceptance.

Accommodation Note—A note given without consideration of value received; usually done to enable the payee to raise money.

Accommodation Note—A note issued without any value being exchanged; typically done to allow the payee to obtain financing.

Account—

Profile—

(a) A statement of debits and credits.

(a) A statement of money going in and out.

(b) A record of transactions with a particular person or persons, or with respect to a particular object.

(b) A list of transactions involving a specific person or people, or related to a specific item.

Account Books—Books in which records of business transactions or accounts are kept.

Account Books—Books that keep records of business transactions or accounts.

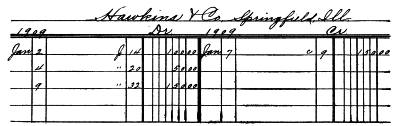

Account Current—An account of transactions during the present month, week, or other current period. An open account.

Account Current—A record of transactions that take place during the current month, week, or other ongoing period. An open account.

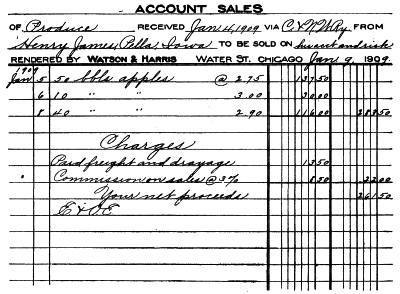

Account Sales—A statement in detail covering sales, expenses, and net proceeds made by a commission merchant to one who has consigned goods to him.

Account Sales—A detailed report that outlines sales, expenses, and net earnings made by a commission merchant for someone who has entrusted goods to them.

Accrued; Accrued Interest—

Earned; Earned Interest—

(a) Accumulated interest not payable until a specified date.

(a) Interest that builds up but is not due until a specific date.

(b) Accumulated rent.

Accumulated rent.

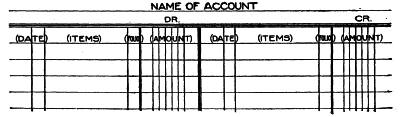

Specimen Account

Sample Account

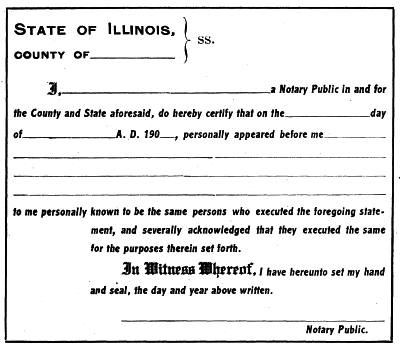

Acknowledgment—A certificate to the genuineness of a document signed and sworn to before an authorized official, as a Notary Public.

Acknowledgment—A certificate verifying the authenticity of a document that is signed and sworn before an authorized official, like a Notary Public.

Administrator—One appointed by the court to settle an estate.

Administrator—A person chosen by the court to manage an estate.

Ad Valorem—According to value. A term used to indicate that duties are payable on the value rather than on the weight or quantity of articles.

Ad Valorem—Based on value. A term used to indicate that duties are charged on the value instead of the weight or amount of items.

Adventure—As used in business, this term signifies a venture or speculation.

Adventure—In a business context, this term refers to a venture or a risky undertaking.

Account Sales

Sales Account

Advice—Information with reference to a business transaction; notice of shipment; notice of draft. Transmitted by letter or telegram.

Advice—Information related to a business transaction; notification of shipment; notification of draft. Sent by letter or telegram.

Affidavit—A statement or declaration made under oath, before an authorized official.

Affidavit—A statement or declaration made under oath in front of an authorized official.

Agent—One authorized to act or transact business for another.

Agent—Someone allowed to act or conduct business on behalf of another person.

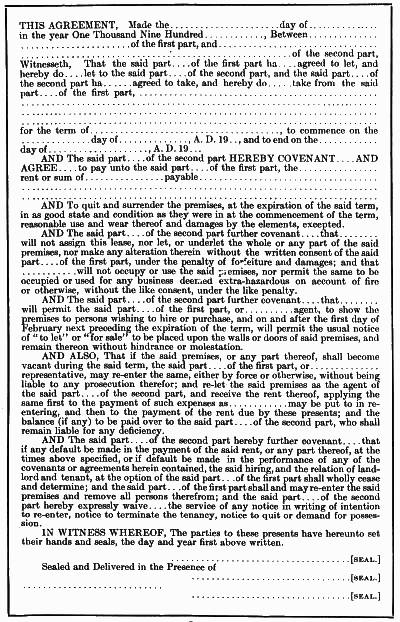

Agreement—A mutual contract entered into by two or more persons.

Agreement—A mutual contract made by two or more people.

Acknowledgment

Recognition

Allowance—An abatement; a credit for inferior goods, error in quantity, etc.

Allowance—A reduction; a credit for subpar products, mistakes in quantity, etc.

Annual Statement—A yearly summary of the transactions of a business.

Annual Statement—A yearly overview of a business's transactions.

Annuity—An amount payable to or received from another each year for a term of years or for life.

Annuity—An amount paid to or received from someone each year for a set number of years or for life.

Antedate—To date a document or paper ahead of the actual time of its execution.

Antedate—To date a document or paper earlier than when it was actually created.

Appraise—To place a value on goods or property. An estimate made for the purpose of assessing duties or taxes.

Appraise—To determine the worth of goods or property. An estimate done to evaluate duties or taxes.

Appreciation—An increase in value. Real estate may increase in value on account of the demand for property in the immediate vicinity.

Appreciation—An increase in value. Real estate can go up in value due to the demand for properties in the surrounding area.

Approbation or Approval Sales. Goods delivered to customers with the understanding that if not found satisfactory they are to be returned within a definite period and without payment.

Approbation or Approval Sales. Products are delivered to customers with the understanding that if they are not satisfactory, they can be returned within a specific timeframe and without payment.

Articles—A collection of merchandise; parts of a written agreement, as "Articles of Association."

Articles—A group of goods; elements of a written contract, such as "Articles of Association."

Arbitrate—To determine or settle disputes between two or more parties, as settlement of differences between employer and employees.

Arbitrate—To resolve or settle conflicts between two or more parties, such as resolving differences between employers and employees.

Assets—All of the property, goods, possessions of value of a person or persons in business.

Assets—All property, goods, and valuable possessions owned by an individual or individuals in a business.

Assign—To transfer or convey to another for the benefit of creditors.

Assign—To give or transfer to someone else for the benefit of creditors.

Assignee—The person to whom the property or business is transferred. Usually acts as a trustee of the creditors.

Assignee—The person who receives the property or business. Typically serves as a trustee for the creditors.

Assignment—The debtor's transfer or conveyance of his property to a trustee.

Assignment—The debtor's transfer or handing over of their property to a trustee.

Assignor—The debtor who makes an assignment, or transfers property for the benefit of creditors.

Assignor—The debtor who makes an assignment or transfers property for the benefit of creditors.

Association—A body organized for a common object.

Association—A group formed for a shared purpose.

Attachment—A legal seizure of goods to satisfy a debt or claim.

Attachment—A legal process where goods are seized to settle a debt or claim.

Auxiliary—Books of record other than books of original entry or principal books of account. Books used for purposes of distribution or the gathering of statistics are "auxiliary" books.

Auxiliary—Books used for record-keeping that aren't main books of account or original entry. Books intended for distribution or for collecting statistics are considered "auxiliary" books.

Audit—To verify the accuracy of accounts by examining or checking records pertaining thereto.

Audit—To confirm the accuracy of accounts by reviewing or checking related records.

Average—As applied to accounts, the mean time which bills of different dates have to run, or an average due date for several accounts. Determining the due date is sometimes referred to as averaging accounts.

Average—In relation to accounts, the average time that bills from different dates have to be paid, or a typical due date for multiple accounts. Figuring out the due date is sometimes called averaging accounts.

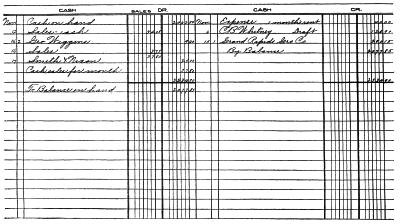

Balance—The difference between the debit and credit sides of an account. To close an account by entering the amount on the lesser side necessary to make the two sides balance.

Balance—The difference between the debit and credit sides of an account. To close an account by entering the amount on the smaller side needed to make the two sides equal.

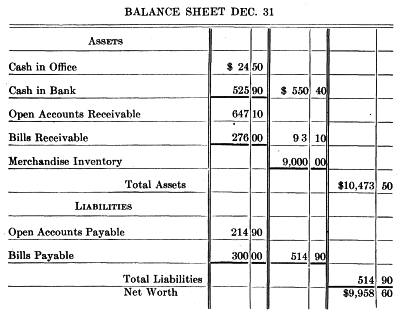

Balance Sheet—A statement or summary in condensed form made for the purpose of showing the standing or condition of a business.

Balance Sheet—A statement or summary in a simplified format created to show the status or condition of a business.

Balance of Trade—The balance or difference in value between the imports and exports of a country.

Balance of Trade—The balance or the difference in value between a country's imports and exports.

Bale—The form in which certain commodities are marketed. A bale of cotton, bale of hay, etc.

Bale—The way in which certain products are sold. A bale of cotton, a bale of hay, etc.

Bank Balance—The net amount to the credit of a depositor at the bank.

Bank Balance—The total amount credited to a depositor's account at the bank.

Bank Note—A note issued by a bank, payable on demand, which passes for money.

Bank Note—A note issued by a bank that can be cashed at any time and is accepted as money.

Bank Draft—An order drawn by one bank on another for the purpose of paying money.

Bank Draft—A written order from one bank to another to transfer funds.

Bank Pass-Book—A small book furnished to a depositor by his bank, in which are entered the amounts of deposits and sometimes the checks or withdrawals.

Bank Pass-Book—A small booklet provided to a depositor by their bank, which contains the amounts of deposits and sometimes the checks or withdrawals.

Bankrupt—A person, firm, or corporation whose liabilities exceed their assets; who are unable to meet their obligations.

Bankrupt—A person, business, or company whose debts are greater than their assets; who cannot meet their financial obligations.

Bill—A statement or record of goods bought or sold, or of services rendered.

Bill—A document that lists goods purchased or sold, or services provided.

Bill

Bill

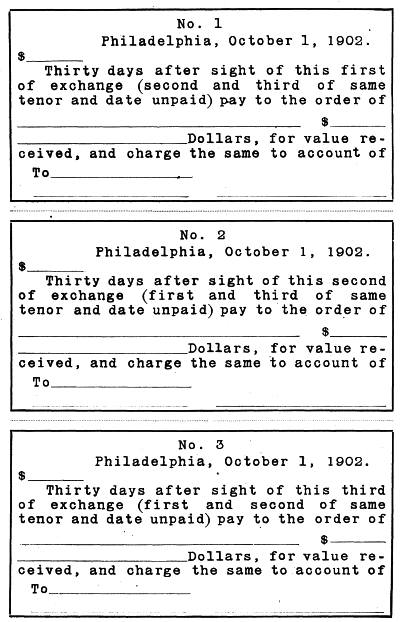

Bill of Exchange—An order on a given person or bank to pay a specified amount to the person and at the time named in the bill. The term is more commonly used to apply to orders on another country, being made in triplicate.

Bill of Exchange—A request made to a specific person or bank to pay a certain amount to the individual named at the time specified in the bill. This term is often used in the context of requests directed at another country and is typically issued in three copies.

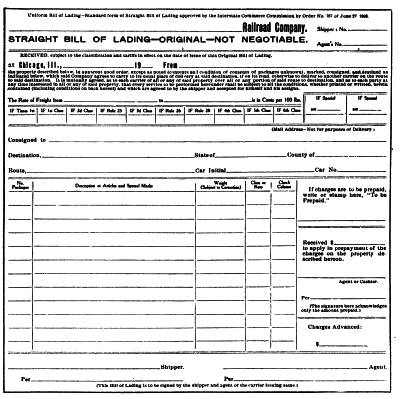

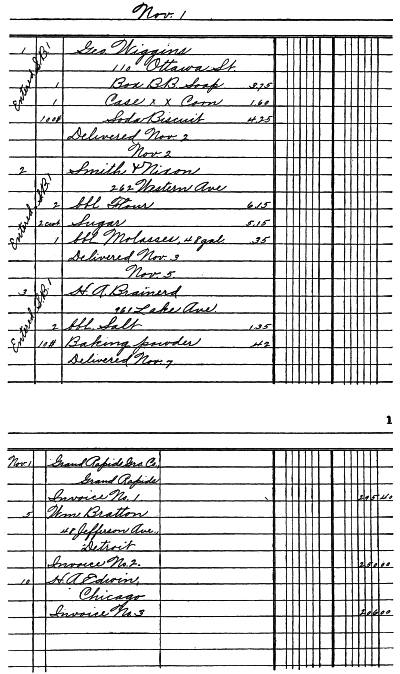

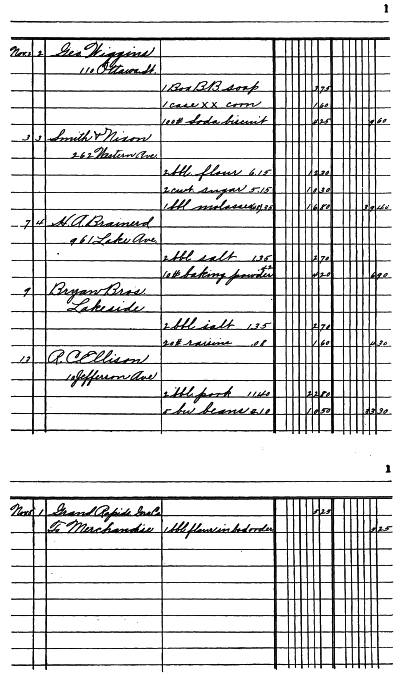

Bill of Lading—A receipt issued by the representative of a common carrier, for goods accepted for transportation to a specified point and at a given rate. It is a contract, and, when transferred to a third party, becomes an absolute title to the goods.

Bill of Lading—A receipt given by a representative of a common carrier for goods accepted for transport to a specific location at a set rate. It acts as a contract, and when passed to a third party, it serves as complete ownership of the goods.

Bill of Lading

Shipping Document

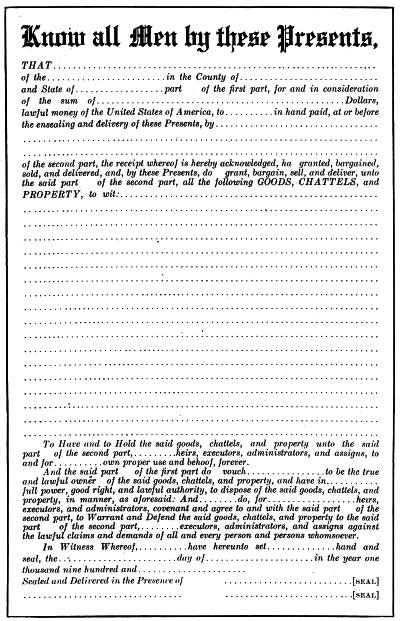

Bill of Sale—A written document executed by the seller, transferring title to personal property.

Bill of Sale—A written document created by the seller that transfers ownership of personal property.

Bill Head—The blank or form on which a bill is made. For illustration, see Bill.

Bill Head—The blank or form used to create a bill. For example, see Bill.

Bill of Exchange

Draft

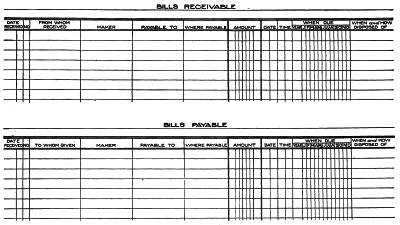

Bills Payable—Promissory notes and acceptances which we are to pay.

Bills Payable—Promissory notes and acceptances that we need to pay.

Bills Receivable—Promissory notes and acceptances which are to be paid to us.

Bills Receivable—Promissory notes and acceptances that are due to us.

Blanks—Papers or books ruled or printed in suitable form for business records.

Blanks—Papers or books designed or printed for use as business records.

Blotter—A book in which are entered memoranda of transactions which are later copied into other books. Also known as a day book.

Blotter—A record book where notes of transactions are written down and later transferred to other books. Also referred to as a day book.

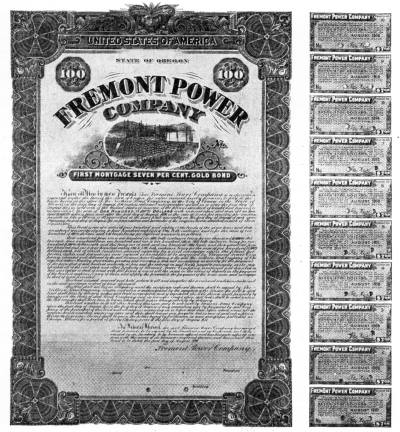

Bond—A written agreement binding a person to do or not to do certain things specified therein. A negotiable instrument secured by mortgage or other security, binding the maker to pay certain sums on specific dates.

Bond—A written agreement that requires a person to do or refrain from doing certain things described in it. A negotiable instrument backed by a mortgage or other security, obligating the issuer to pay specific amounts on predetermined dates.

Bonded Goods—Goods stored in a government warehouse, or in bonded cars, bonds having been given by the owner for the payment of import duties or internal revenue taxes when removed.

Bonded Goods—Goods kept in a government warehouse, or in bonded vehicles, with bonds provided by the owner for the payment of import duties or internal revenue taxes upon removal.

Bonus—An amount paid in excess of the sum originally agreed upon. A premium or gift—for example, a sum paid to a salesman as extra compensation for making a certain number of sales.

Bonus—An amount paid beyond what was originally agreed upon. A premium or gift—for example, a sum paid to a salesperson as extra compensation for achieving a certain number of sales.

Book Account—A charge or evidence of indebtedness on the books of account not secured by note or other written promise.

Book Account—A charge or proof of debt recorded in the accounting books that is not backed by a note or any other written agreement.

Brand—A class of goods. A symbol or name used to designate a specific article. A trade mark.

Brand—A category of products. A symbol or name used to identify a specific item. A trademark.

Broker—One who acts as agent or middleman between buyer and seller.

Broker—Someone who acts as an agent or middleman between a buyer and a seller.

Brokerage—The commissions or fees paid the broker for his services. Also a term used to designate his business.

Brokerage—The commissions or fees paid to the broker for their services. Also a term used to refer to their business.

Bullion—Uncoined gold or silver.

Bullion—Unminted gold or silver.

Call Loans—Loans made payable on demand or when called for.

Call Loans—Loans that must be paid back on demand or when requested.

Cancel—To render null and void; to annul.

Cancel—To make something invalid; to void.

Capital—Property or money invested in a business.

Capital—Money or assets put into a business.

Capital Stock—A term used to indicate the subscriptions of all stockholders to the capital of a corporation.

Capital Stock—A term used to refer to the contributions of all shareholders to the capital of a corporation.

Cartage—The charges made for hauling goods by wagon, or otherwise than by freight or express.

Cartage—The fees charged for transporting goods by wagon or any method other than by freight or express.

Cash Sales—Sales for which immediate payment is received in contradistinction to sales of goods on credit.

Cash Sales—Sales where payment is received immediately, as opposed to sales of goods on credit.

Bill of Sale

Sales Agreement

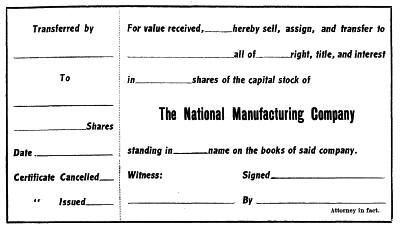

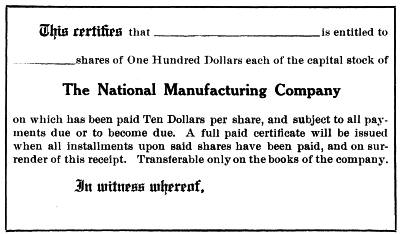

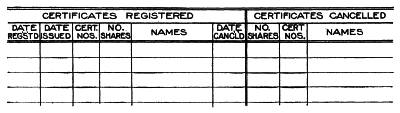

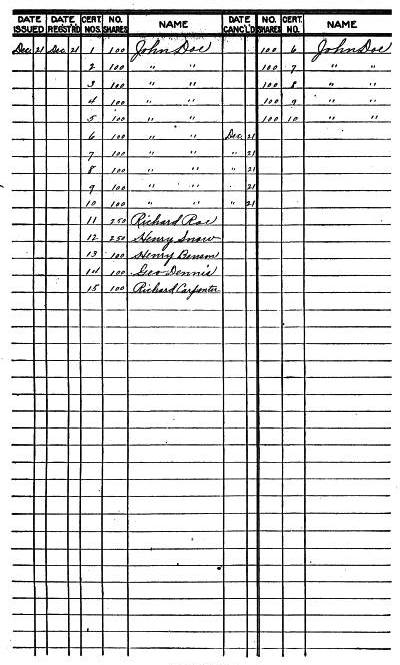

Certificate of Stock—A written statement or declaration of the purchase of a specified number of shares of the capital stock of a corporation. An evidence of ownership.

Certificate of Stock—A written statement or declaration confirming the purchase of a specific number of shares of a corporation's capital stock. It serves as proof of ownership.

Certified Check—A check, the payment of which is guaranteed by the bank on which it is drawn.

Certified Check—A check whose payment is guaranteed by the bank that issued it.

Charges—The expense involved in handling goods or in performing a specific act—as, for example, charges for storage, freight charges, etc. Also a synonym for debits.

Charges—The cost associated with handling goods or carrying out a particular task—such as charges for storage, freight charges, etc. Also a synonym for debits.

Chart—A classified exhibit of the components of a business organization, showing the authority and responsibilities of the members. Grouping of the accounts of a business with respect to their relation to one another.

Chart—A categorized display of the elements of a business organization, illustrating the authority and responsibilities of its members. An arrangement of the accounts of a business in relation to each other.

Charter—To hire a car, ship, or other instrument of transportation. A document defining the rights and duties of a corporation.

Charter—To rent a car, ship, or other mode of transportation. A document outlining the rights and responsibilities of a corporation.

Check—An order on a bank to pay to a certain person, or to the order of such person, a specified sum, which sum is to be charged to the account of the drawer of the check.

Check—An order given to a bank to pay a specific amount to a certain person, or to the order of that person, with that amount being deducted from the account of the person who wrote the check.

Clearing House—An exchange established by banks in cities, for their convenience in making daily settlements. The checks and drafts on the different banks are exchanged without the formality of presenting them personally at each bank. A balance is found, and this amount only is paid in cash.

Clearing House—A network set up by banks in cities to make daily transactions easier. Checks and drafts from various banks are exchanged without having to deliver them in person to each bank. A balance is calculated, and only that amount is paid in cash.

Closing an Account—Making an entry that will balance the account.

Closing an Account—Making an entry that balances the account.

Collateral—Pledges of security—as stocks, bonds, etc.—to protect an obligation or insure the payment of a loan.

Collateral—Promises of security—like stocks, bonds, etc.—to safeguard an obligation or ensure the payment of a loan.

Commission—A percentage or share of the proceeds allowed for the sale of merchandise—as the pay of a commission merchant for selling a car of flour.

Commission—A percentage or share of the profits earned from the sale of merchandise—given as payment to a commission merchant for selling a car of flour.

Commission Merchant—One who sells goods on commission. Similar to a broker.

Commission Merchant—Someone who sells goods on commission. It's similar to a broker.

Commercial Paper—Negotiable paper used in business.

Commercial Paper—A type of negotiable instrument used in business transactions.

Common Law—Law based upon the precedent of usage, though not contained in the statutes.

Common Law—Law based on established customs and precedents, even though it isn't written in statutes.

Company—A corporation; also used to designate partners whose names are not known.

Company—A business; also used to refer to partners whose names are not known.

Compromise—To settle an account for less than the amount claimed. To agree upon a settlement.

Compromise—To settle an account for less than the claimed amount. To come to an agreement on a settlement.

Certificate of Stock

Stock Certificate

Consideration—The price or money paid or to be paid which induces the entering into a contract by two or more persons.

Consideration—The price or money that is paid or will be paid to encourage two or more people to enter into a contract.

Consignee—The party to whom goods are shipped. A person to whom goods are sent to be sold on commission is a consignee. The goods so sent are known as a consignment, and the sender is the consignor.

Consignee—The person or entity that receives goods that are shipped. Someone who receives goods to sell on commission is called a consignee. The items sent are referred to as a consignment, and the sender is called the consignor.

Consul—An agent of the Government, residing in a foreign part, who guards the interests of his own Government.

Consul—An official of the Government living in a foreign country, who protects the interests of their own Government.

Contra—On the opposite side—as a contra account.

Contra—On the other side—as a contra account.

Contract—A written agreement between two or more persons to perform or not to perform some specified act or acts.

Contract—A written agreement between two or more people to do or not do certain specified actions.

Contingent Assets and Liabilities—Resources or liabilities whose value depends upon certain conditions.

Contingent Assets and Liabilities—Resources or debts whose value depends on specific conditions.

Contingent Fund—A sum put aside to provide for an anticipated obligation; a reserve fund.

Contingent Fund—A set amount of money saved to cover an expected obligation; a reserve fund.

Conveyance—A term used to describe certain forms of legal documents transferring from one person to another, title to property or collateral.

Conveyance—A term used to describe specific types of legal documents that transfer ownership of property or collateral from one person to another.

Copyright—A right granted to an author or publisher to control the publication of any writing, or the reproduction of a photograph, painting, etc.

Copyright—A right given to an author or publisher to manage the publication of any writing, or the reproduction of a photograph, painting, etc.

Counterfeit—A spurious coin, or bank or treasury note.

Counterfeit—A fake coin, or a forged bank or treasury note.

Coupon—A certificate detached from a bond, which entitles the holder to the payment of interest.

Coupon—A certificate taken from a bond that gives the holder the right to receive interest payments.

Coupon Bond—Bonds to which are attached coupons calling for the payment of interest. The coupons, when detached, become negotiable paper.

Coupon Bond—Bonds that have coupons attached for interest payments. The coupons, once removed, become negotiable instruments.

Credentials—Letters or testimonials conveying authority.

Credentials—Letters or references verifying authority.

Creditor—One whom we owe; one who gives credit.

Creditor—Someone we owe money to; a person or organization that extends credit.

Currency—The coin or paper money constituting the circulating medium of a country.

Currency—The coins or paper money that make up the money used in a country.

Debenture—A certified evidence of debt. See Bond.

Debenture—A document that proves a debt. See Bond.

Debit—To charge; to record an amount due.

Debit—To charge; to list an amount owed.

Deed—A written document or contract transferring title to real estate.

Deed—A written document or contract that transfers ownership of real estate.

Defalcation—The appropriating to one's own use, of money intrusted to him by another; embezzlement.

Defalcation—Taking money that has been entrusted to you by someone else for your own use; embezzlement.

Deferred Bonds—Bonds which are to be paid when some condition is fulfilled in the future.

Deferred Bonds—Bonds that will be paid when a certain condition is met in the future.

Delivery Receipt—An acknowledgment of the delivery of goods. Largely used by merchants in the delivery of goods to customers.

Delivery Receipt—A confirmation of the delivery of goods. Mainly used by sellers when delivering goods to customers.

Demand Note—A promissory note or acceptance payable on presentation or on demand.

Demand Note—A promissory note or acceptance that is payable upon presentation or when requested.

Deposit—The money placed in custody of the bank, subject to order.

Deposit—The money held in the bank's care, available on request.

Depreciation—A reduction in the value of property. In a manufacturing plant, buildings and machinery depreciate in value through wear and tear; a residence property may depreciate owing to the nature of a nearby building.

Depreciation—A decrease in the value of property. In a manufacturing facility, buildings and machinery lose value due to wear and tear; a residential property may lose value because of the type of nearby construction.

Delivery Receipt

Delivery Confirmation

Discount—An allowance or abatement made for the payment of a bill within a specified period. The interest paid in advance on money borrowed from a bank.

Discount—A deduction or reduction given for paying a bill within a certain timeframe. The interest paid upfront on money borrowed from a bank.

Dishonor—Refusal to accept a draft, or failure to pay a written obligation when due.

Dishonor—Refusing to accept a draft or failing to pay a written obligation when it's due.

Demand Note

Request for Payment

Dividend—The profits which are distributed among the stockholders of a corporation.

Dividend—The profits that are shared with the shareholders of a corporation.

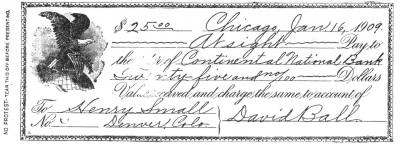

Draft—A written order for the payment of money—usually made through some bank.

Draft—A written request for the payment of money—typically made through a bank.

Drawer—The person by whom the draft is made; the one who requested the payment of money by the drawee.

Drawer—The person who creates the draft; the one who asked the drawee to make the payment.

Drayage—Synonymous with cartage.

Drayage—Same as cartage.

Due Bill—A written acknowledgment of an amount due; of the same effect as a demand note.

Due Bill—A written acknowledgment of an amount owed; it has the same effect as a demand note.

Dunning—Soliciting or urgently pressing the payment of a debt.

Dunning—Requesting or urgently demanding payment for a debt.

Duplicate—A copy of a paper or document; the act of making a copy.

Duplicate—A copy of a paper or document; the act of creating a copy.

Duty—The tax paid on imported goods.

Duty—The tax charged on imported items.

Doubtful—Of questionable value. We refer to an account as "doubtful" when we question the likelihood of its payment.

Doubtful—Of questionable value. We call an account "doubtful" when we are uncertain about the likelihood of it being paid.

Draft

Draft

Earnest—An advance payment, applying on the purchase price, made to bind an oral bargain.

Earnest—An upfront payment applied to the purchase price, made to secure an oral agreement.

Embezzlement—See Defalcation.

Embezzlement—See Misappropriation.

Exchange—The charge made by a bank for the collection of drafts or checks.

Exchange—The fee a bank charges for collecting drafts or checks.

Exports—Commodities sent to another country.

Exports—Goods sent to another country.

Extend—To set a later date for payment; to add several items and carry the totals to the proper column.

Extend—To push back the payment deadline; to combine multiple items and move the totals to the correct column.

Face Value—The amount for which a commercial paper is drawn.

Face Value—The amount that a commercial paper is written for.

Facsimile—An exact duplicate or exact copy.

Fax—A precise duplicate or replica.

Financial Statement—A term used in the same sense as balance sheet or annual statement.

Financial Statement—A term used in the same way as balance sheet or annual statement.

Fiscal—A financial or business year, in contradistinction to a calendar year. The fiscal year of a business may commence and end on any date—usually on the date on which it was started.

Fiscal—A financial or business year, as opposed to a calendar year. A business's fiscal year can start and end on any date—usually on the date it was launched.

Fixed Assets—Permanent assets acquired by a firm or corporation to enable them to conduct a business. Includes real estate, building, machinery, horses and wagons, etc.

Fixed Assets—Long-term assets purchased by a company or organization to help them operate their business. This includes real estate, buildings, machinery, horses, wagons, and so on.

Fixed Charges—Those charges in connection with the operation of a business which occur at regular intervals, such as rent, taxes, etc.

Fixed Charges—These are costs related to running a business that happen regularly, like rent, taxes, etc.

Fixtures—A fixed asset represented by that part of the furniture not readily removable, such as gas and electric light fixtures.

Fixtures—A fixed asset defined as part of the furniture that can't be easily removed, like gas and electric light fixtures.

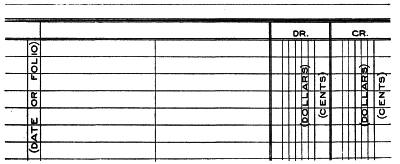

Folio—A column provided in account books, in which to enter the page numbers of other books from or to which records are transferred.

Folio—A column in accounting books where you enter the page numbers of other books that records are moved from or to.

Footing—The sum or amount of a column of figures.

Footing—The total or amount of a column of numbers.

Foreign Exchange—Drafts on foreign cities.

Foreign Exchange—Drafts on other cities.

Freight—The charges paid for the transportation of goods.

Freight—The fees charged for shipping goods.

Gain—The increase in value of assets or profit resulting from a transaction or transactions.

Gain—The rise in value of assets or profit resulting from a transaction or transactions.

Gauging—Measuring the liquid contents of casks or barrels.

Gauging—Measuring the liquid contents of casks or barrels.

Going Business—A term used to designate a business in actual operation. Goodwill or the reputation of a business has a value so long as the business is in operation, or keeps going. When a business is discontinued, only the physical assets or actual properties owned by the business are of value.

Going Business—A term used to describe a business that is currently operating. Goodwill or the reputation of a business is valuable as long as the business is active. When a business shuts down, only the physical assets or actual properties owned by the business hold value.

Good Will—The monetary value of the reputation of a business over and above its visible assets; the value of a business name.

Good Will—The financial worth of a business's reputation beyond its tangible assets; the value of a brand name.

Gross—The entire amount in contradistinction to the net amount—as gross weight or gross profit.

Gross—The total amount compared to the net amount—like gross weight or gross profit.

Guarantee or Guaranty—Surety for the maintenance of quality or the performance of contracts.

Guarantee or Guaranty—Assurance for maintaining quality or fulfilling contracts.

Honor—To pay a promissory note when due; to accept or pay a draft.

Honor—To pay a promissory note when it's due; to accept or pay a draft.

Hypothecate—To deposit as collateral security for a loan.

Hypothecate—To put up as collateral for a loan.

Import—To bring goods into the country.

Import—To bring products into the country.

Income—The receipts of a business.

Income—The revenue of a business.

Income Bonds—Bonds on which the payment of interest is contingent on profits earned. If the interest is passed on account of lack of funds, the holder of the bond has no claim.

Income Bonds—Bonds whose interest payments depend on the profits that are made. If the interest is skipped due to insufficient funds, the bondholder has no rights to claim it.

Indemnity—Security against a form of loss which has occurred or may occur—as fire insurance, against loss by fire.

Indemnity—Protection against a type of loss that has happened or could happen—like fire insurance, which covers loss due to fire.

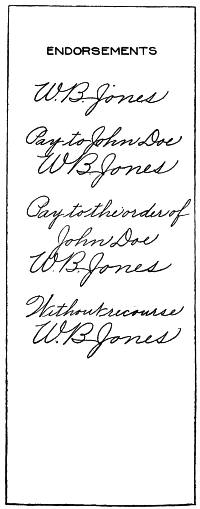

Indorse—To guarantee the payment of commercial paper by writing one's name on the back.

Indorse—To ensure the payment of a check or other financial document by signing your name on the back.

Indorsee—The person to whom a paper is indorsed.

Indorsee—The person to whom a document is endorsed.

Lease

Rent

Indorser—The person who guarantees payment; the one who indorses.

Indorser—The person who guarantees payment; the one who endorses.

Infringe; Infringement—To trespass upon another's rights—as infringement of a patent or copyright.

Infringe; Infringement—To violate someone else's rights—such as infringing on a patent or copyright.

Installment—An account or note the payment of which is to be made in several parts, at stated intervals.

Installment—An account or note that you pay off in multiple parts, at regular intervals.

Insolvent—Unable to pay one's obligations.

Broke—Unable to pay debts.

Instant—Principally used in correspondence to indicate the present month.

Instant—Mainly used in correspondence to refer to the current month.

Insurance Policy—A contract between an insurance company and the insured.

Insurance Policy—A contract between an insurance company and the person being insured.

Interest—The sum or premium paid for the use of money; one's share in a business or a particular property.

Interest—The amount or fee paid for borrowing money; your share in a business or specific asset.

Inventory—An itemized schedule of the property or goods belonging to a business.

Inventory—A detailed list of the items or goods owned by a business.

Investment—Money paid for goods or property to be held; not for speculation.

Investment—Money spent on goods or property to be owned; not for speculation.

Invoice—A list of goods bought or sold. See Bill.

Invoice—A list of items purchased or sold. See Bill.

Jobber—One who buys from manufacturers and sells to retailers; a middleman.

Jobber—A person who purchases from manufacturers and sells to retailers; an intermediary.

Job Lot—An incomplete assortment of goods to be disposed of in a lump. Usually indicates small portions or remnants of a stock, the bulk of which has been sold.

Job Lot—A mixed collection of items that are to be sold together. Typically refers to leftover or remaining parts of inventory, most of which has already been sold.

Joint Stock—Property owned in common by several individuals known as stockholders.

Joint Stock—Property that is collectively owned by multiple individuals known as stockholders.

Leakage—An allowance for waste of liquids in transit; refers particularly to liquids shipped in casks.

Leakage—A provision for the loss of liquids during transport; specifically relates to liquids that are shipped in barrels.

Lease—A written agreement covering the use of property during a specified period, at a stated rental.

Lease—A written agreement that outlines the use of property for a specific period, at an agreed-upon rental rate.

Legal Tender—The lawful amount to be offered in payment of an obligation. Bank notes or other currency which passes for money.

Legal Tender—The official amount that must be offered to settle a debt. Banknotes or other forms of currency that are accepted as money.

Lessee—One who receives a lease. The lessor makes it.

Lessee—A person who rents or leases a property. The lessor creates the lease.

Letter of Advice—A letter giving notice of some act in which the one receiving the advice has an interest—as making a shipment, notice of draft, etc.

Letter of Advice—A letter informing someone about an action that they have an interest in, such as a shipment, notice of payment, etc.

Letter of Credit—A letter which authorizes the receiving, by the holder, of credit to a stated amount. Principally used by travelers to secure credit from foreign bankers.

Letter of Credit—A document that allows the holder to receive credit for a specific amount. It is mainly used by travelers to obtain credit from banks abroad.

Liabilities—The obligations or debts of a firm, corporation, or individual.

Liabilities—The responsibilities or debts of a business, company, or individual.

License—Permission, usually granted by a municipality, to conduct a specified business.

License—Approval, typically given by a local government, to operate a particular business.

Liquidation—The closing-out of a business or an estate.

Liquidation—The process of shutting down a business or settling an estate.

Loss and Gain—The amount of profits or losses of a business.

Loss and Gain—The total profits or losses of a business.

Maker—One who signs a note.

Maker—Person who signs a note.

Manifest—A list or schedule of the articles in a ship's cargo, or of the goods comprising a shipment.

Manifest—A list or schedule of the items in a ship's cargo or the goods included in a shipment.

Order

Order

Maturity—The time when an obligation or an account is due.

Maturity—The point in time when a debt or account needs to be paid.

Mercantile Agency—A company which obtains and keeps for the use of its customers information showing the standing of business firms.

Mercantile Agency—A company that gathers and maintains information for its customers about the status of business firms.

Merchandise—The stock in trade, or goods bought to be sold again.

Merchandise—The inventory or items purchased to be resold.

Money Order—An order instructing a third party to pay money to the person named. A form in which money is transmitted.

Money Order—A request directing another party to pay money to the person specified. A document used to send money.

Monopoly—The exclusive control of the manufacture or sale of an article.

Monopoly—The sole control over the production or sale of a product.

Mortgage—A temporary transfer of title to land, goods, or chattels to secure payment of a debt.

Mortgage—A temporary transfer of ownership of property, goods, or personal items to secure repayment of a loan.

Mortgagor—One who gives a mortgage. The one to whom the mortgage is given is the mortgagee.

Mortgagor—The person who gives a mortgage. The person who receives the mortgage is the mortgagee.

Negotiable—An agreement or any commercial paper which can be transferred by delivery or endorsement—as a bank note or promissory note.

Negotiable—An agreement or any commercial document that can be transferred by delivery or endorsement, like a banknote or promissory note.

Net—Less all charges or deductions. Gross assets less liabilities leaves net capital; gross income less all expenses leaves net profit; etc.

Net—Total amount after deducting all charges or deductions. Gross assets minus liabilities equals net capital; gross income minus all expenses equals net profit; etc.

Nominal—Having no actual existence; exists in name only.

Nominal—Having no real existence; exists only in name.

Obligation—Indebtedness.

Responsibility—Debt.

Open Account—An account which has not been paid.

Open Account—An account that hasn’t been settled.

Opening Entries—The entries made in the books when it is desired to open the accounts of a business.

Opening Entries—The entries recorded in the books when you want to start the accounts for a business.

Option—The right to be the first purchaser; a privilege.

Option—The right to be the first buyer; a special privilege.

Orders—Requests for the shipment of goods.

Orders—Requests to send goods.

Original Entry—The first record made of a charge or credit which becomes the basis of proof of the account.

Original Entry—The first entry noted for a charge or credit that serves as the proof of the account.

Overdraw—To draw a check for a greater amount than the drawer has on deposit in a bank.

Overdraw—To write a check for more money than what the account holder has available in the bank.

Par—Face value.

Par—Face value.

Partnership—A firm; a union of two or more persons for the transaction of business or the ownership of property.

Partnership—A collaboration; a group of two or more people coming together to conduct business or own property.

Payee—The one to whom money is to be paid. The one who pays the money is the payer.

Payee—The person who will receive the payment. The person who makes the payment is the payer.

Per Annum—By the year.

Yearly

Per Cent or Per Centum—By the hundred.

Percent—By the hundred.

Per Diem—By the day.

Daily Rate

Personal Account—Any account with an individual, firm, or corporation.

Personal Account—Any account belonging to an individual, business, or corporation.

Personal Property—All property other than real estate.

Personal Property—Everything that isn't real estate.

Petty Cash—A term used to signify small expenditures in actual cash.

Petty Cash—A term used to refer to small cash expenses.

Postdate—To date ahead; after the real date.

Postdate—To date in advance; after the actual date.

Post—To transfer amounts from books of entry to the ledger, which is the book of final record.

Post—To move amounts from the journals to the ledger, which is the final record book.

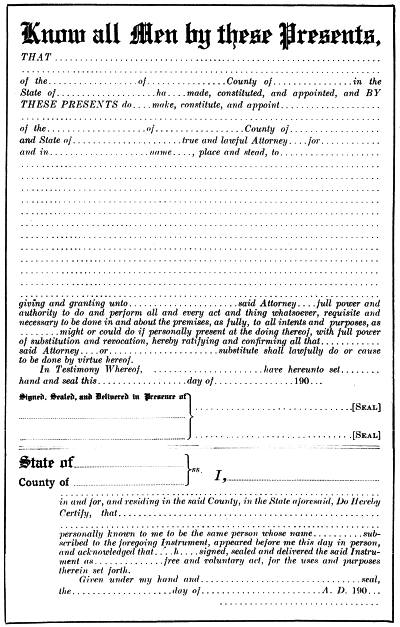

Power of Attorney—Authority to act for and in the name of another in business transactions.

Power of Attorney—The right to act on behalf of someone else in business dealings.

Preferred Stock—Stock which participates in the profits before any dividend can be paid on the common or ordinary stock.

Preferred Stock—Stock that earns a share of the profits before any dividends are paid on common or ordinary stock.

Premium—The amount paid above par value; the amount paid to an insurance company for insurance against loss.

Premium—The amount paid over the par value; the amount paid to an insurance company for coverage against loss.

Present Worth—The net capital of an individual.

Present Worth—The net assets of a person.

Proceeds—The amount realized from a sale of property.

Proceeds—The amount received from selling a property.

Profit and Loss—Synonymous with loss and gain.

Profit and Loss—The same as loss and gain.

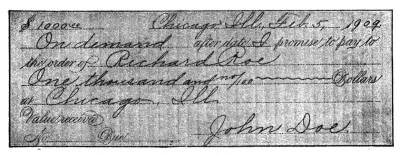

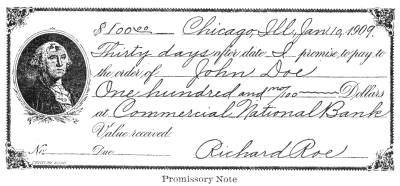

Promissory Note—A promise, signed by the maker or makers, to pay a stated sum at a specified time and place.

Promissory Note—A promise, signed by the individual or individuals, to pay a specific amount at a designated time and location.

Promissory Note

Promissory Note

Pro Rata—A distribution of money or goods in proportionate parts.

Pro Rata—Distributing money or goods in proportional amounts.

Protest—A formal notice acknowledged before a notary that a note or draft was not paid at maturity, and that the maker will be held responsible for the payment.

Protest—A formal notice recognized by a notary that a note or draft wasn’t paid on time, and that the issuer will be responsible for the payment.

Quotation—A price named for a given article or for services.

Quotation—A price listed for a specific item or for services.

Ratify—To approve; to sanction the acts of an agent.

Ratify—To approve; to endorse the actions of an agent.

Raw Material—Material to be manufactured into other products—as iron ore, pig iron, lumber, etc.

Raw Material—Material that will be made into other products—such as iron ore, pig iron, lumber, etc.

Real Estate—Primarily refers to land, although buildings are frequently included.

Real Estate—Mainly refers to land, though buildings are often included.

Rebate—An allowance or deduction. See Allowance.

Rebate—A discount or deduction. See Allowance.

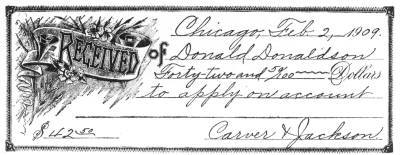

Receipt—An acknowledgment that money or something of value has been received.

Receipt—A confirmation that money or something valuable has been received.

Receiver—One appointed to take charge of the affairs of a corporation, either solvent or insolvent, and administer its affairs under orders of the court.

Receiver—A person designated to manage the operations of a corporation, whether it is financially stable or not, and oversee its activities under the direction of the court.

Remittance—Money or funds of any character transmitted from one place to another.

Remittance—Money or funds of any type sent from one location to another.

Power of Attorney

POA

Renewal Note—A new note given to take the place of a note that is due.

Renewal Note—A new note issued to replace a note that is due.

Rent—A payment for the use of property owned by another.

Rent—A payment for using someone else's property.

Resources—Synonymous with assets.

Resources—Same as assets.

Revenue—Income of a business.

Revenue—Business income.

Revoke—To recall authority of another to act as agent.

Revoke—To take back the authority of someone else to act on your behalf.

Royalty—A stipulated amount paid to the owner of a mine, patent, copyright, etc., usually based on sales. The owner of a copyright receives a royalty based on the number of books sold.

Royalty—A specified payment made to the owner of a mine, patent, copyright, etc., typically calculated on sales. The owner of a copyright earns a royalty based on the number of books sold.

Receipt

Receipt

Schedule—Inventory of goods or statement of prices.

Schedule—List of items or price list.

Sight Draft—A draft payable on presentation or at sight.

Sight Draft—A draft that's payable when it's presented or upon sight.

Solvent—Able to pay one's debts.

Solvent—Able to pay bills.

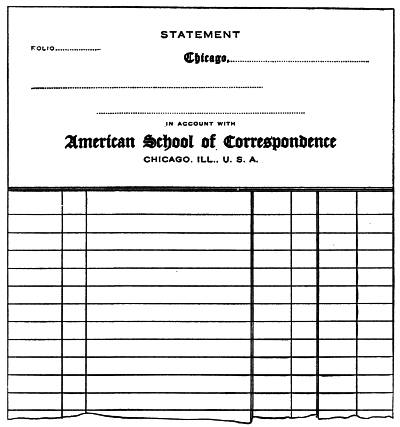

Statement—Commonly used to designate a list of bills to customers during a stated period. Also used to designate a financial summary showing profits and losses of a business.

Statement—Typically refers to a list of bills for customers over a specific time frame. It’s also used to refer to a financial summary that outlines a business's profits and losses.

Stockholder—An owner of stock in a corporation or joint stock company.

Stockholder—A person who owns shares in a corporation or joint stock company.

Storage—The charge for keeping goods in a store or warehouse.

Storage—The fee for holding items in a store or warehouse.

Surety—One who has guaranteed or made himself responsible for the acts of another.

Surety—Someone who has guaranteed or made themselves responsible for the actions of another person.

Syndicate—A combination of capitalists, usually temporary, for the conduct of some financial enterprise.

Syndicate—A temporary group of investors that come together to manage a financial project.

Tare—The amount deducted from gross weights to cover weight of packages—as crates, boxes, barrels, etc.

Tare—The weight that is subtracted from the total weight to account for the weight of the containers—like crates, boxes, barrels, etc.

Tariff—A schedule of prices, as freight tariff. The duties imposed on imports or exports.

Tariff—A list of prices, like a freight tariff. The fees charged on goods brought into or sent out of a country.

Terms—The conditions governing a given sale. "Terms cash" means that payment is to be made as soon as goods are delivered.

Terms—The conditions that apply to a particular sale. "Terms cash" means that payment is due as soon as the goods are delivered.

Tickler—Memoranda of matters requiring attention in the future, arranged according to dates.

Tickler—Notes on things that need to be addressed later, organized by date.

Time Draft—A draft which matures at some future date.

Time Draft—A draft that is due at a later date.

Trade Discount—The discount allowed by a manufacturer to a jobber or by a jobber to a retailer.

Trade Discount—The discount given by a manufacturer to a wholesaler or by a wholesaler to a retailer.

Statement

Statement

Trade Mark—See Brand.

Trademark—See Brand.

Ultimo—Principally used in correspondence to designate last month.

Ultimo—Mainly used in letters to refer to last month.

Valid—Legal or binding; usually applied to a properly executed contract.

Valid—Legal or binding; typically used to describe a properly executed contract.

Value Received—Used in notes to indicate that value has been given.

Value Received—Used in notes to show that value has been given.

Void—Without legal force; not binding.