This is a modern-English version of Cyclopedia of Commerce, Accountancy, Business Administration, v. 05 (of 10), originally written by American School of Correspondence.

It has been thoroughly updated, including changes to sentence structure, words, spelling,

and grammar—to ensure clarity for contemporary readers, while preserving the original spirit and nuance. If

you click on a paragraph, you will see the original text that we modified, and you can toggle between the two versions.

Scroll to the bottom of this page and you will find a free ePUB download link for this book.

Transcriber's Note:

Transcriber's Note:

The cover image was created by the transcriber and is placed in the public domain.

The cover image was made by the transcriber and is in the public domain.

A VIEW IN UNION STOCK YARDS, CHICAGO, ILL.

The Greatest Live Stock Market in the World

A VIEW IN UNION STOCK YARDS, CHICAGO, ILL.

The Largest Livestock Market in the World

Cyclopedia

of

Commerce, Accountancy, Business Administration

Authors and Collaborators

- JAMES BRAY GRIFFITH, Managing Editor

- Head, Dept. of Commerce, Accountancy, and Business Administration, American School of Correspondence.

- ROBERT H. MONTGOMERY

- Of the Firm of Lybrand, Ross Bros. & Montgomery, Certified Public Accountants.

- Editor of the American Edition of Dicksee's Auditing.

- Formerly Lecturer on Auditing at the Evening School of Accounts and Finance of the University of Pennsylvania, and the School of Commerce, Accounts, and Finance of the New York University.

- ARTHUR LOWES DICKINSON, F. C. A., C. P. A.

- Of the Firms of Jones, Caesar, Dickinson, Wilmot & Company, Certified Public Accountants, and Price, Waterhouse & Company, Chartered Accountants.

- Of the Firm of Lybrand, Ross Bros. & Montgomery, Certified Public Accountants.

- F. H. MACPHERSON, C. A., C. P. A.

- Of the Firm of F. H. Macpherson & Co., Certified Public Accountants.

- CHAS. A. SWEETLAND

- Consulting Public Accountant.

- Author of "Loose-Leaf Bookkeeping," and "Anti-Confusion Business Methods."

- E. C. LANDIS

- Of the System Department, Burroughs Adding Machine Company.

- Editor-in-Chief, Textbook Department, American School of Correspondence.

- CECIL B. SMEETON, F. I. A.

- Public Accountant and Auditor.

- President, Incorporated Accountants' Society of Illinois.

- Fellow, Institute of Accounts, New York.

3

- JOHN A. CHAMBERLAIN, A. B., LL. B.

- Of the Cleveland Bar.

- Lecturer on Suretyship, Western Reserve Law School.

- Author of "Principles of Business Law."

- HUGH WRIGHT

- Auditor, Westlake Construction Company.

- GLENN M. HOBBS, Ph. D.

- Secretary, American School of Correspondence.

- JESSIE M. SHEPHERD, A. B.

- Associate Editor, Textbook Department, American School of Correspondence.

- GEORGE C. RUSSELL

- Systematizer.

- Formerly Manager, System Department, Elliott-Fisher Company.

- OSCAR E. PERRIGO, M. E.

- Specialist in Industrial Organization.

- Author of "Machine-Shop Economics and Systems," etc.

- DARWIN S. HATCH, B. S.

- Assistant Editor, Textbook Department, American School of Correspondence.

- CHAS. E. HATHAWAY

- Cost Expert.

- Chief Accountant, Fore River Shipbuilding Co.

- CHAS. WILBUR LEIGH, B. S.

- Associate Professor of Mathematics, Armour Institute of Technology.

- L. W. LEWIS

- Advertising Manager, The McCaskey Register Co.

- MARTIN W. RUSSELL

- Registrar and Treasurer, American School of Correspondence.

4

- HALBERT P. GILLETTE, C. E.

- Managing Editor, Engineering-Contracting.

- Author of "Handbook of Cost Data for Contractors and Engineers."

- R. T. MILLER, JR., A. M., LL. B.

- President, American School of Correspondence.

- WILLIAM SCHUTTE

- Manager of Advertising, National Cash Register Co.

- E. ST. ELMO LEWIS

- Advertising Manager, Burroughs Adding Machine Company.

- Author of "The Credit Man and His Work" and "Financial Advertising."

- RICHARD T. DANA

- Consulting Engineer.

- Chief Engineer, Construction Service Co.

- P. H. BOGARDUS

- Publicity Manager, American School of Correspondence.

- WILLIAM G. NICHOLS

- General Manufacturing Agent for the China Mfg. Co., The Webster Mfg. Co., and the Pembroke Mills.

- Author of "Cost Finding" and "Cotton Mills."

- C. H. HUNTER

- Advertising Manager, Elliott-Fisher Co.

- FRANK C. MORSE

- Filing Expert.

- Secretary, Browne-Morse Co.

- H. E. K'BERG

- Expert on Loose-Leaf Systems.

- Formerly Manager, Business Systems Department, Burroughs Adding Machine Co.

- EDWARD B. WAITE

- Head, Instruction Department, American School of Correspondence.

Authorities Consulted

The editors have freely consulted the standard technical and business literature of America and Europe in the preparation of these volumes. They desire to express their indebtedness, particularly, to the following eminent authorities, whose well-known treatises should be in the library of everyone interested in modern business methods.

The editors have consulted the standard technical and business literature from America and Europe in creating these volumes. They want to express their gratitude, especially to the following respected authorities, whose well-known works should be in the library of anyone interested in modern business methods.

Grateful acknowledgment is made also of the valuable service rendered by the many manufacturers and specialists in office and factory methods, whose coöperation has made it possible to include in these volumes suitable illustrations of the latest equipment for office use; as well as those financial, mercantile, and manufacturing concerns who have supplied illustrations of offices, factories, shops, and buildings, typical of the commercial and industrial life of America.

Grateful acknowledgment is made also of the valuable service rendered by the many manufacturers and specialists in office and factory methods, whose cooperation has made it possible to include in these volumes suitable illustrations of the latest equipment for office use; as well as those financial, mercantile, and manufacturing companies that have provided illustrations of offices, factories, shops, and buildings, typical of the commercial and industrial life of America.

- JOSEPH HARDCASTLE, C. P. A.

- Formerly Professor of Principles and Practice of Accounts, School of Commerce, Accounts, and Finance, New York University.

- Author of "Accounts of Executors and Testamentary Trustees."

- HORACE LUCIAN ARNOLD

- Specialist in Factory Organization and Accounting.

- Author of "The Complete Cost Keeper," and "Factory Manager and Accountant."

- JOHN F. J. MULHALL, P. A.

- Specialist in Corporation Accounts.

- Author of "Quasi Public Corporation Accounting and Management."

- SHERWIN CODY

- Advertising and Sales Specialist.

- Author of "How to Do Business by Letter," and "Art of Writing and Speaking the English Language."

- FREDERICK TIPSON, C. P. A.

- Author of "Theory of Accounts."

- CHARLES BUXTON GOING

- Managing Editor of The Engineering Magazine.

- Associate in Mechanical Engineering, Columbia University.

- Corresponding Member, Canadian Mining Institute.

- F. E. WEBNER

- Public Accountant.

- Specialist in Factory Accounting.

- Contributor to The Engineering Press.

6

- AMOS K. FISKE

- Associate Editor of the New York Journal of Commerce.

- Author of "The Modern Bank."

- JOSEPH FRENCH JOHNSON

- Dean of the New York University School of Commerce, Accounts, and Finance.

- Editor, The Journal of Accountancy.

- Author of "Money, Exchange, and Banking."

- M. U. OVERLAND

- Of the New York Bar.

- Author of "Classified Corporation Laws of All the States."

- THOMAS CONYNGTON

- Of the New York Bar.

- Author of "Corporate Management," "Corporate Organization," "The Modern Corporation," and "Partnership Relations."

- THEOPHILUS PARSONS, LL. D.

- Author of "The Laws of Business."

- E. ST. ELMO LEWIS

- Advertising Manager, Burroughs Adding Machine Company.

- Formerly Manager of Publicity, National Cash Register Co.

- Author of "The Credit Man and His Work," and "Financial Advertising."

- T. E. YOUNG, B. A., F. R. A. S.

- Ex-President of the Institute of Actuaries.

- Member of the Actuary Society of America.

- Author of "Insurance."

- LAWRENCE R. DICKSEE, F. C. A.

- Professor of Accounting at the University of Birmingham.

- Author of "Advanced Accounting," "Auditing," "Bookkeeping for Company Secretary," etc.

- FRANCIS W. PIXLEY

- Author of "Auditors, Their Duties and Responsibilities," and "Accountancy."

- CHARLES U. CARPENTER

- General Manager, The Herring-Hall-Marvin Safe Co.

- Formerly General Manager, National Cash Register Co.

- Author of "Profit Making Management."

7

- C. E. KNOEPPEL

- Specialist in Cost Analysis and Factory Betterment.

- Author of "Systematic Foundry Operation and Foundry Costing," "Maximum Production through Organization and Supervision," and other papers.

- HARRINGTON EMERSON, M. A.

- Consulting Engineer.

- Director of Organization and Betterment Work on the Santa Fe System.

- Originator of the Emerson Efficiency System.

- Author of "Efficiency as a Basis for Operation and Wages."

- ELMER H. BEACH

- Specialist in Accounting Methods.

- Editor, Beach's Magazine of Business.

- Founder of The Bookkeeper.

- Editor of The American Business and Accounting Encyclopedia.

- J. J. RAHILL, C. P. A.

- Member, California Society of Public Accountants.

- Author of "Corporation Accounting and Corporation Law."

- FRANK BROOKER, C. P. A.

- Ex-New York State Examiner of Certified Public Accountants.

- Ex-President, American Association of Public Accountants.

- Author of "American Accountants' Manual."

- CLINTON E. WOODS, M. E.

- Specialist in Industrial Organization.

- Formerly Comptroller, Sears, Roebuck & Co.

- Author of "Organizing a Factory," and "Woods' Reports."

- CHARLES E. SPRAGUE, C. P. A.

- President of the Union Dime Savings Bank, New York.

- Author of "The Accountancy of Investment," "Extended Bond Tables," and "Problems and Studies in the Accountancy of Investment."

- CHARLES WALDO HASKINS, C. P. A., L. H. M.

- Author of "Business Education and Accountancy."

- JOHN J. CRAWFORD

- Author of "Bank Directors, Their Powers, Duties, and Liabilities."

- DR. F. A. CLEVELAND

- Of the Wharton School of Finance, University of Pennsylvania.

- Author of "Funds and Their Uses."

GENERAL SALES OFFICES, SWIFT & CO., CHICAGO, ILL.

GENERAL SALES OFFICES, SWIFT & CO., CHICAGO, IL.

Foreword

With the unprecedented increase in our commercial activities has come a demand for better business methods. Methods which were adequate for the business of a less active commercial era, have given way to systems and labor-saving ideas in keeping with the financial and industrial progress of the world.

With the unprecedented growth in our business activities has come a demand for better business methods. Techniques that were sufficient for a less active commercial period have been replaced by systems and time-saving ideas that match the financial and industrial advancements of the world.

¶ Out of this progress has risen a new literature—the literature of business. But with the rapid advancement in the science of business, its literature can scarcely be said to have kept pace, at least, not to the same extent as in other sciences and professions. Much excellent material dealing with special phases of business activity has been prepared, but this is so scattered that the student desiring to acquire a comprehensive business library has found himself confronted by serious difficulties. He has been obliged, to a great extent, to make his selections blindly, resulting in many duplications of material without securing needed information on important phases of the subject.

¶ From this progress has emerged a new kind of literature—the literature of business. However, with the fast growth in the field of business, its literature has hardly kept up, at least not to the same degree as in other fields and professions. While a lot of excellent content addressing specific aspects of business activity has been produced, it's so dispersed that students looking to build a comprehensive business library face significant challenges. They often have to make their choices without clear guidance, leading to a lot of repeated material without getting essential information on crucial areas of the subject.

¶ In the belief that a demand exists for a library which shall embrace the best practice in all branches of business—from buying to selling, from simple bookkeeping to the administration of the financial affairs of a great corporation—these volumes have been prepared. Prepared primarily for 9use as instruction books for the American School of Correspondence, the material from which the Cyclopedia has been compiled embraces the latest ideas with explanations of the most approved methods of modern business.

¶ Believing there is a demand for a library that covers the best practices in all areas of business—from purchasing to sales, and from basic bookkeeping to managing the financial affairs of a large corporation—these volumes have been created. They are primarily intended as instructional books for the American School of Correspondence. The content that makes up the Cyclopedia includes the latest concepts along with explanations of the most widely accepted methods in modern business.

¶ Editors and writers have been selected because of their familiarity with, and experience in handling various subjects pertaining to Commerce, Accountancy, and Business Administration. Writers with practical business experience have received preference over those with theoretical training; practicability has been considered of greater importance than literary excellence.

¶ Editors and writers have been chosen for their knowledge and experience in dealing with various topics related to Commerce, Accounting, and Business Administration. Writers with real-world business experience were preferred over those with just academic training; practicality was seen as more important than literary skill.

¶ In addition to covering the entire general field of business, this Cyclopedia contains much specialized information not heretofore published in any form. This specialization is particularly apparent in those sections which treat of accounting and methods of management for Department Stores, Contractors, Publishers and Printers, Insurance, and Real Estate. The value of this information will be recognized by every student of business.

¶ In addition to covering the whole general area of business, this Cyclopedia includes a lot of specialized information that hasn't been published anywhere else. This specialization is especially noticeable in the sections that discuss accounting and management methods for department stores, contractors, publishers and printers, insurance, and real estate. Every business student will see the value of this information.

¶ The principal value which is claimed for this Cyclopedia is as a reference work, but, comprising as it does the material used by the School in its correspondence courses, it is offered with the confident expectation that it will prove of great value to the trained man who desires to become conversant with phases of business practice with which he is unfamiliar, and to those holding advanced clerical and managerial positions.

¶ The main value of this Cyclopedia is as a reference tool, but since it also includes the material used in the School’s correspondence courses, it is provided with the strong belief that it will be very beneficial for professionals who want to familiarize themselves with aspects of business practices they might not know, as well as for those in advanced clerical and managerial roles.

¶ In conclusion, grateful acknowledgment is made to authors and collaborators, to whose hearty coöperation the excellence of this work is due.

¶ In conclusion, we sincerely thank the authors and contributors, whose enthusiastic cooperation made this work outstanding.

Table of Contents

VOLUME V

| Wholesale, Commission, and Storage Accounts | By James B. Griffith[1] | Page [2]11 | |

| Wholesale Business—Controlling Accounts—Sample Transactions—Order and Sales Record—Abstract of Sales—Sales Expense—Trial Balance Book—Commission and Brokerage Business—Merchandise Broker—Manufacturer's Agent—Shipments—Agents' or Factors' Account—Principal's Account—Commission Account—Produce Shipper's Books—Commission Merchants' Books—Consignment Ledger Account—Storage Accounts—Special Records | |||

| Single-Entry Bookkeeping | By James B. Griffith | Page 91 | |

| Distinctive Features—Books Used—Debit and Credit—Posting—Proprietor's Account—Proving Work—Model Set—Determining Profit—Closing Books—Changing to Double Entry—Trial Balances and Comparative Statements—Comparative Statements—Proof without Trial Balance—Book Inventories—Demonstration of Proof—Reverse or Slip Posting—Special Accounting Forms—Cash Books—Cash Journals—Tabular Sales Books—Pay-Roll Records | |||

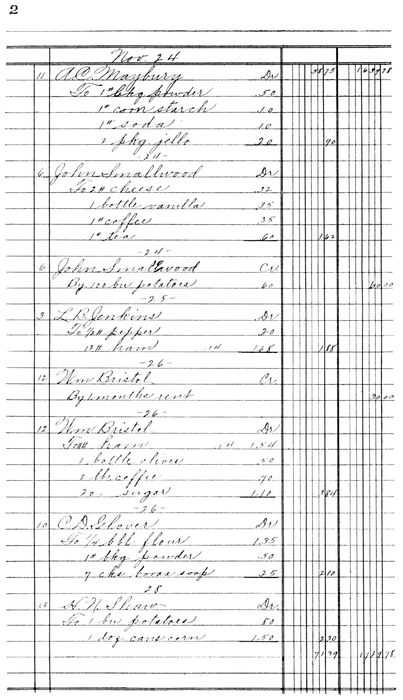

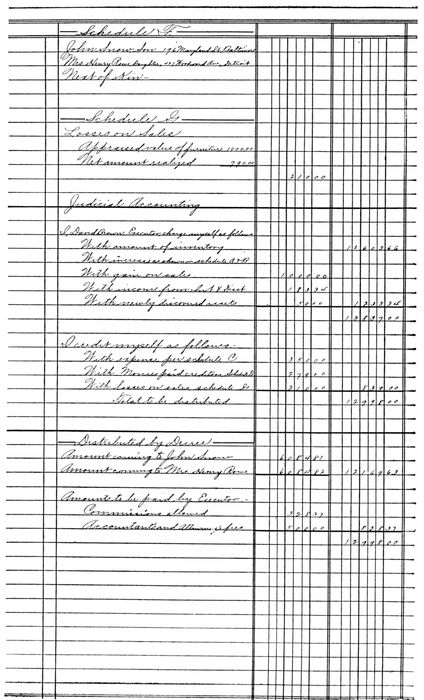

| Trustees and Executors Accounts | By James B. Griffith | Page 163 | |

| Executors' Accounting—Inventory—Intermediate Account—Final Account—Schedules—Form of Account—Sample Accounts—Accounts with Trust Provisions—Exercise—Realization and Liquidation Account—Statement of Affairs—Resources and Liabilities—Balance Sheet—Affairs of a Bankrupt—Appraiser—Statement of Affairs—Deficiency of Account | |||

| Brokerage Accounts | By Chas. A. Sweetland | Page 195 | |

| Grain Purchases—Bulls and Bears—Broker's Commission—Securities—Transfers—Clearing House—Ring Settlement—Commodities Handled—Cornering Market—Value of Wire—Settlement of Contracts by Offset—Adjustment of Balances or Settlement—Commission Allowed Brokers—Books and Forms Used—Glossary of Board of Trade Terms | |||

| Billing and Order Management | By Geo. C. Russell | Page 235 | |

| European Methods—Machines for Manifolding—Development of Billing Machines—Loose-Leaf Sales Sheets and Invoices—Duplicate Invoices—Condensed Billing—Traffic Department Records—Analysis of Quantities and Amounts—Unit Billing—Back Orders—Split Orders—Loose-Leaf Sheets—Binders—Designing Stationery—Styles of Type—Carbon Papers—Blinds—How to Handle Orders on Billing Machine—Invoices in Blanket Form—Tabulators—Computing Machines in Billing—The Colored Sheet System—Compound Forms—Retail Dry Goods Billing—Devices of the Future | |||

| Review Questions | Page 303 | ||

| Index | Page 319 | ||

1. For professional standing of authors, see list of Authors and Collaborators at front of volume.

__A_TAG_PLACEHOLDER_0__.For the professional credentials of authors, check the list of Authors and Collaborators at the front of the volume.

2. For page numbers, see foot of pages.

OFFICE, FARWELL, OZMUN, KIRK & CO. (WHOLESALE HARDWARE), ST. PAUL, MINN.

OFFICE, FARWELL, OZMUN, KIRK & CO. (WHOLESALE HARDWARE), ST. PAUL, MINN.

WHOLESALE, COMMISSION, AND STORAGE ACCOUNTS

WHOLESALE BUSINESS

In this section complete methods of bookkeeping as practiced in wholesale houses are demonstrated. Numerous modern methods that are readily adaptable to other lines of business are illustrated and explained in detail.

In this section, complete bookkeeping methods used in wholesale businesses are demonstrated. Several modern techniques that can be easily adapted to other types of businesses are illustrated and explained in detail.

DIVIDING THE LEDGER

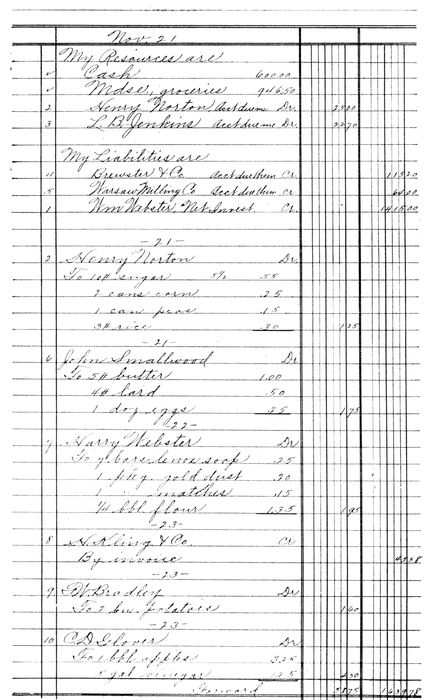

1. There are many advantages in dividing the ledger into sections. The subdivisions most commonly used are purchase ledger, sales ledger, and general ledger. Such divisions greatly facilitate posting and reduce the chances of error. While it is advisable in most cases to use a separate book for each division, the three ledgers may be combined in one book by setting aside a section for each. This practice is not recommended except where the number of accounts is small, when general and purchase ledgers or purchase and sales ledgers may be combined. The division of the ledger into three sections does not necessitate radical changes, either in form or method of handling, in the other books.

1. There are many benefits to dividing the ledger into sections. The most common subdivisions are the purchase ledger, sales ledger, and general ledger. These divisions make posting much easier and lower the chances of mistakes. While it's usually best to have a separate book for each section, the three ledgers can be put together in one book by allocating a section for each. This approach is not recommended unless the number of accounts is small, in which case the general and purchase ledgers or purchase and sales ledgers can be combined. Dividing the ledger into three sections doesn't require major changes in either the format or method of handling other books.

2. Purchase Ledger. The purchase ledger contains only accounts with those from whom we are making purchases. The balances of the accounts in this ledger will be on the credit side and represent a liability. The total balance of the purchase ledger is the amount we owe on open accounts. If, for example, our purchases on account during a stated period amount to $964.50, and the amount paid on account by us is $320.30, we still owe $644.20. If the work is correct the combined balances of all open accounts in the purchase ledger will exactly equal this amount.

2. Purchase Ledger. The purchase ledger includes only accounts with the suppliers from whom we are buying. The account balances in this ledger will be on the credit side and represent a liability. The total balance of the purchase ledger is the amount we owe on outstanding accounts. For instance, if our purchases on account during a specific period total $964.50, and we’ve paid $320.30 on those accounts, we still owe $644.20. If everything is accurate, the combined balances of all outstanding accounts in the purchase ledger will match this amount perfectly.

123. Sales Ledger. The sales ledger contains only accounts with customers to whom goods are sold on account. The balances of the accounts in the sales ledger will be on the debit side and represent an asset. The total balance of the sales ledger is the amount that our customers owe us on open accounts. Suppose that a business is started with no open accounts receivable—during a stated period the sales on account amount to $1,427.75, and the total payments received on account are $965.50—the amount still outstanding is $462.25, and this amount should exactly equal the combined balances of all the open accounts in the sales ledger.

123. Sales Ledger. The sales ledger includes only accounts for customers to whom goods are sold on credit. The balances of the accounts in the sales ledger will show on the debit side and represent an asset. The total balance of the sales ledger is the sum that our customers owe us on open accounts. For example, if a business starts with no open accounts receivable—and during a specific period sales on credit total $1,427.75, while the total payments received amount to $965.50—the outstanding amount is $462.25. This amount should exactly match the combined balances of all the open accounts in the sales ledger.

The sales ledger is sometimes subdivided into two or more parts. The divisions may be City and Country or they may be according to the letters of the alphabet—as A-K, L-Z, etc.

The sales ledger is sometimes divided into two or more sections. The divisions might be by City and Country or they could be based on the letters of the alphabet—like A-K, L-Z, etc.

4. Accounts in Both Ledgers. Occasionally one from whom we are purchasing goods will also be a customer. For reasons which will appear later, accounts should, in these cases, be opened in both the purchase ledger and the sales ledger. When settlement of such an account is made, the necessary adjusting entries are made through the journal.

4. Accounts in Both Ledgers. Sometimes, a supplier we're buying goods from is also a customer. For reasons that will be explained later, we should open accounts in both the purchase ledger and the sales ledger in these situations. When it's time to settle such an account, the necessary adjusting entries are made through the journal.

5. General Ledger. The general ledger contains the investment accounts of the proprietor or partners, and all real, representative, and nominal accounts. Accounts with the purchase and sales ledgers are also kept in this ledger. These are controlling accounts which represent at all times the total balances of the purchase and sales ledgers.

5. General Ledger. The general ledger includes the investment accounts of the owner or partners, as well as all real, representative, and nominal accounts. Accounts related to the purchase and sales ledgers are also maintained in this ledger. These are controlling accounts that consistently reflect the total balances of the purchase and sales ledgers.

When statements of the other ledgers have been made and proved correct, a trial balance of the general ledger is made.

When the statements from the other ledgers have been completed and verified, a trial balance of the general ledger is created.

CONTROLLING ACCOUNTS

6. A controlling account is one which exhibits a summary of all of the accounts in a ledger, or of all accounts of the same class.

6. A controlling account is one that shows a summary of all the accounts in a ledger or all accounts of the same type.

The sales account, with which the student has been made acquainted, exhibits net sales, while a sales controlling account exhibits a summary of all accounts in the sales ledger. The debits to the sales controlling account represent the total debits to customers' accounts as shown by the sales book or the journal. The credits to the sales controlling account represent the total credits to customers as shown by the cash book and the journal. This account is variously styled 13Sales Ledger Account, Accounts Receivable Account, or Sales Controlling Account.

The sales account that the student has learned about shows net sales, while a sales controlling account provides a summary of all accounts in the sales ledger. The debits in the sales controlling account indicate the total debits to customers' accounts, as recorded in the sales book or journal. The credits in the sales controlling account represent the total credits to customers, as noted in the cash book and journal. This account is commonly known as the 13Sales Ledger Account, Accounts Receivable Account, or Sales Controlling Account.

A purchase controlling account exhibits a summary of all accounts in the purchase ledger. It is called a Purchase Ledger Account, Accounts Payable Account, or Purchase Controlling Account.

A purchase controlling account shows a summary of all accounts in the purchase ledger. It's referred to as a Purchase Ledger Account, Accounts Payable Account, or Purchase Controlling Account.

These controlling accounts are kept in the general ledger and show at all times the totals of accounts receivable and accounts payable, without the necessity of listing the individual balances. At the end of the month statements of the balances of the accounts in purchase and sales ledgers are made, and the totals of these balances must agree with the balances of the controlling accounts.

These control accounts are maintained in the general ledger and always display the totals for accounts receivable and accounts payable, without needing to list each individual balance. At the end of the month, statements of the balances in the purchase and sales ledgers are created, and these totals must match the balances in the control accounts.

The operation of these controlling accounts demonstrates one of the most apparent advantages of the division of the ledger. If an error is made in posting to an account in the sales ledger it is discovered as soon as the statement of the sales ledger is made, and can be located without referring to purchase or general ledger accounts. Without the ledger division and the use of controlling accounts, there would be nothing to assist in locating an error in the trial balance in any particular section of the ledger.

The operation of these controlling accounts shows one of the clearest benefits of splitting the ledger. If there's a mistake in posting to an account in the sales ledger, it’s spotted as soon as the sales ledger statement is prepared, and it can be found without needing to check the purchase or general ledger accounts. Without the ledger division and the use of controlling accounts, it would be challenging to identify an error in the trial balance within any specific part of the ledger.

ORDER BLANKS

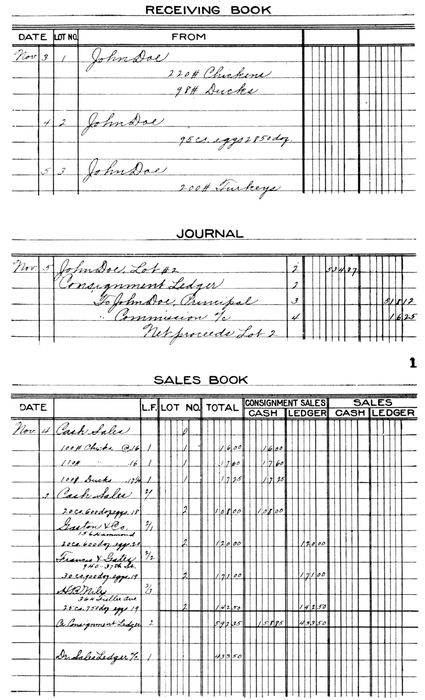

7. In a wholesale business it is customary to have all orders entered on specially ruled order blanks of a uniform size. These orders are filed in a binder designed for the purpose, which takes the place of the old style order book.

7. In a wholesale business, it's standard to have all orders recorded on specially designed order forms of a consistent size. These orders are stored in a binder made for that purpose, replacing the old-fashioned order book.

These order blanks are furnished to salesmen who send in their orders on them. When an order is received direct from the customer it, also, is transcribed on one of these blanks so that all order records will be uniform. One very appreciable advantage in the use of this loose sheet system of order blanks is that all unfilled orders are kept in a binder by themselves.

These order forms are provided to salespeople who submit their orders using them. When an order comes directly from the customer, it is also written on one of these forms to ensure that all order records are consistent. One significant benefit of using this loose sheet system for order forms is that all pending orders are stored in a binder separately.

8. Filling Orders. Each day the orders to be filled should be placed in a temporary binder or holder and sent to the warehouse. The packer will check quantities shipped and return the order, together with the shipping receipt from the railroad or express company, to the bookkeeping department.

8. Filling Orders. Each day, the orders to be filled should be placed in a temporary binder or holder and sent to the warehouse. The packer will check the quantities shipped and return the order, along with the shipping receipt from the railroad or express company, to the bookkeeping department.

The amounts are extended, and the invoice is made out from this order blank. The sale is next recorded in the sales book. Instead 14of entering each item in the sales book the totals for each department are entered in the proper column. Each sale is numbered in the sales book as illustrated and the same number is placed on the order. These orders are then filed in the binder for filled orders in exact numerical order, which brings them also in the order of the dates of shipment.

The amounts are extended, and the invoice is created from this order blank. The sale is then recorded in the sales book. Instead of entering each item in the sales book, the totals for each department are entered in the appropriate column. Each sale is numbered in the sales book as shown, and the same number is assigned to the order. These orders are then filed in the binder for completed orders in exact numerical order, which also organizes them by the dates of shipment.

Order Blank

Order Form

SALES BOOK

9. The sales book used in this set exhibits some features not heretofore shown. At the right are three columns for the distribution of sales. At the left, in addition to columns for number, date, and folio, are two columns headed cash and sales ledger. All cash sales are entered in the cash column, and all sales on account are entered in the sales ledger column. At the end of the week or month the total of the sales ledger column is posted to the debit of the sales ledger account in the general ledger, while the totals of the sales columns at the right are posted to the credit of the sales account in the general ledger.

9. The sales book used in this set has some features that haven't been shown before. On the right, there are three columns for tracking sales distribution. On the left, in addition to columns for number, date, and folio, there are two columns labeled cash and sales ledger. All cash sales are recorded in the cash column, while all sales on account are recorded in the sales ledger column. At the end of the week or month, the total from the sales ledger column is posted as a debit to the sales ledger account in the general ledger, and the totals from the sales columns on the right are posted as a credit to the sales account in the general ledger.

INVOICE REGISTER

10. A form of purchase book, which also combines an invoice register, is shown in this set. Unlike the forms of purchase book with which the student has been made familiar, this invoice register gives full particulars as to terms, discount, when due, and when and how paid.

10. This set includes a type of purchase book that also serves as an invoice register. Unlike the purchase book forms the student is used to, this invoice register provides complete details on terms, discounts, due dates, and information on when and how payments are made.

The combined footings of the two department columns must of course agree with the footing of the amount column. At the end of the month the total of the amount column is posted to the credit of purchase ledger account in the general ledger, and the totals of the department columns are posted to the debit of the purchase account in the general ledger.

The combined footings of the two department columns must obviously match the footing of the amount column. At the end of the month, the total of the amount column is entered as a credit in the purchase ledger account in the general ledger, and the totals of the department columns are entered as a debit in the purchase account in the general ledger.

The details of payment are kept in the invoice register as a memorandum only. This provides a convenient record of unpaid invoices, showing when each is due.

The payment details are recorded in the invoice register as a memo only. This gives a handy record of unpaid invoices, indicating when each one is due.

CASH BOOK

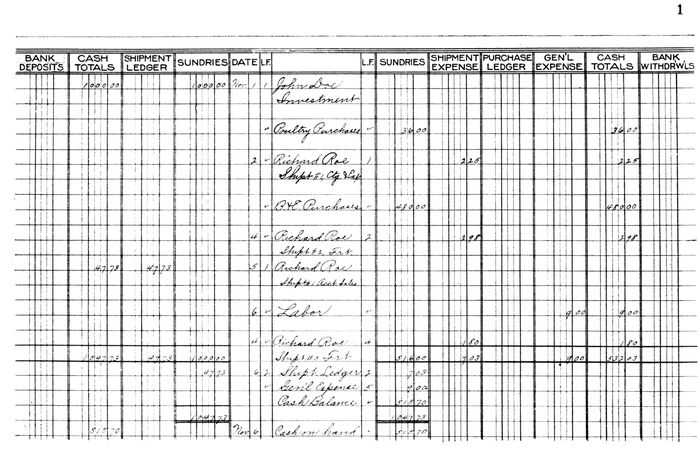

11. In this set we introduce a columnar cash book which also serves as a journal for cash transaction and is known as a cash journal. The principal advantage of a columnar book lies in the opportunity to introduce columns with special headings for accounts to which entries are frequent. Not only does this permit of carrying footings to the end of the month with one posting to the ledger account, but it provides a convenient classification of receipts and expenditures with a complete segregation of items of a given class.

11. In this section, we introduce a columnar cash book that also functions as a journal for cash transactions, referred to as a cash journal. The main benefit of a columnar book is that it allows for the addition of columns with specific headings for accounts that have frequent entries. This not only enables month-end totals to be posted to the ledger account with a single entry but also offers an organized way to classify receipts and expenses, keeping items of the same type clearly separated.

In the form illustrated, columns are provided on the debit side for cash, purchase ledger (subdivided for discount and amount), bank deposits, and sundries; on the credit side, cash, sales ledger (subdivided for discount and amount), cash sales, bank withdrawals, and sundries. At first glance it might appear that this form is a departure from the regular form of cash book, but it should be remembered that the cash columns are the only ones having anything to do with the cash account. A cash receipt is entered in the cash debit column, but the amount is credited to its source through the proper credit column; thus a payment received on account is debited to cash and credited through the sales ledger column. A deposit is credited to cash and debited to bank deposits; the payment of a purchase ledger 16account by check is credited to bank withdrawals, and debited to purchase ledger account.

In the form shown, there are columns on the debit side for cash, purchase ledger (broken down into discount and amount), bank deposits, and miscellaneous items; on the credit side, there are columns for cash, sales ledger (broken down into discount and amount), cash sales, bank withdrawals, and miscellaneous items. At first glance, it might seem like this form is different from the usual cash book, but it's important to note that the cash columns are the only ones related to the cash account. A cash receipt is recorded in the cash debit column, but the amount is credited to its source through the appropriate credit column; for example, a payment received on account is debited to cash and credited through the sales ledger column. A deposit is credited to cash and debited to bank deposits; a purchase ledger account payment made by check is credited to bank withdrawals and debited to the purchase ledger account.

The discount columns are memorandum columns only, the net cash being entered in the amount columns under purchase and sales ledger. These columns are included that the total payment may be posted to personal accounts in purchase or sales ledger. The totals of these columns are to be posted to discount and interest columns at the end of the month.

The discount columns are just for records; the actual cash will be recorded in the amount columns under the purchase and sales ledger. These columns are included so that the total payment can be posted to personal accounts in the purchase or sales ledger. The totals from these columns will be posted to the discount and interest columns at the end of the month.

The total amount to be posted to the debit of the purchase ledger account and to the credit of sales ledger account is made up of the totals of the discount and amount columns.

The total to be charged to the purchase ledger account and credited to the sales ledger account consists of the totals from the discount and amount columns.

The sundries columns are provided for all entries for which there are no special columns and are used principally for transactions affecting general ledger accounts. These columns are sometimes used for ordinary journal entries not involving an exchange of cash, but their use for this purpose is strongly advised against. The cash book should be used exclusively for recording cash transactions. When columnar purchase, sales, and cash books are used, the journal is only needed for adjusting and closing entries, and for this purpose it is best to provide an ordinary two-column journal.

The sundries columns are meant for any entries that don't have specific columns and are mainly used for transactions impacting general ledger accounts. These columns can sometimes be used for regular journal entries that don't involve cash transactions, but it's highly recommended not to use them for this purpose. The cash book should only be used for recording cash transactions. When using columnar purchase, sales, and cash books, the journal is only required for adjusting and closing entries, and it's best to have a standard two-column journal for this purpose.

SUBDIVISION OF EXPENSE ACCOUNT

12. In every business there are several classes of expense and it is very useful to know the exact amount of each class. When all expenses are charged under one head, it is impossible to determine without considerable checking, whether or not any particular class of expense is more than it should be. It is customary, therefore, to subdivide expense and to open accounts in the ledger for different classes of expense. Some subdivisions in common use are rent (paid), insurance, taxes, interest and discount, in freight, out freight, salaries, labor, fuel, office supplies, telegraph and telephone, postage, general expense, etc. The exact subdivisions used must of necessity be governed by the nature of the business. For instance, the item of telegraph and telephone charges may be of importance in one business, while in another, the number of such charges would be so small that a separate account is not warranted.

12. In every business, there are different types of expenses, and it’s really helpful to know the exact amount for each type. When all expenses are grouped together under one category, it’s hard to figure out—without a lot of checking—if any specific type of expense is higher than it should be. So, it’s common practice to break down expenses and create separate accounts in the ledger for various types of expenses. Some common categories include rent (paid), insurance, taxes, interest and discount, incoming freight, outgoing freight, salaries, labor, fuel, office supplies, telegraph and telephone, postage, general expenses, and so on. The exact categories used should depend on the nature of the business. For example, telegraph and telephone charges might be significant in one business, while in another, those charges might be so minimal that a separate account isn’t necessary.

PETTY CASH VOUCHER

13. A form of envelope voucher for petty cash is illustrated. A strong manilla envelope in what is known as size #10 takes the place of the petty cash book. It is ruled for a record of payments, and a receipt for each payment is placed in the envelope. At the bottom is a space for a distribution of the amounts to the proper accounts. When the petty cash fund is depleted—or at stated intervals—a check is drawn for the amount expended and it is charged through the cash book, leaving petty cash intact. The amount of the petty cash fund is considered as cash on hand, and the voucher envelope accounts for any part of the fund not actually in the cash drawer. Petty cash should be used sparingly, as it is intended only for small expense items when it is inconvenient to give a check. When the books are closed, the petty cash expenditures may be charged through the cash book as cash payments, instead of drawing a check.

13. An example of an envelope voucher for petty cash is shown. A sturdy manila envelope in size #10 serves as the petty cash book. It's designed to keep track of payments, and a receipt for each payment is placed inside the envelope. At the bottom, there’s a space to allocate the amounts to the appropriate accounts. When the petty cash fund runs low—or at scheduled times—a check is issued for the amount spent, and it is recorded in the cash book, keeping the petty cash balance unchanged. The amount in the petty cash fund is treated as cash on hand, and the voucher envelope accounts for any part of the fund that isn’t physically in the cash drawer. Petty cash should be used carefully, as it’s meant only for small expenses when giving a check isn't practical. When the books are closed, petty cash expenditures can be recorded in the cash book as cash payments instead of issuing a check.

Petty Cash Voucher

Petty Cash Receipt

TREATMENT OF PROTESTED PAPER

14. When a note, draft, or check is protested, the bank will charge us with the protest fee in addition to the face of the paper. The total amount must then be charged to the one from whom the paper was received. Suppose the check of Jones & Laughlin for $100.00 goes to protest and is returned to us with a protest fee of $2.50—the entry will be:

14. When a note, draft, or check is protested, the bank will charge us the protest fee plus the amount of the paper. The full amount then needs to be charged to the person from whom we received the paper. For example, if a check from Jones & Laughlin for $100.00 gets protested and is returned to us with a protest fee of $2.50, the entry will be:

| Jones & Laughlin | $102.50 | |

| Bank | $102.50 | |

| Check No. 16 given to First Nat. | ||

| Bank to cover J. & L. check for | ||

| $100.00, protest fee $2.50. |

SAMPLE TRANSACTIONS

15. D. A. Hall is engaged in the business of a wholesale dealer in men's and boys' clothing. On Feb. 1st. his balance sheet is as follows:

15. D. A. Hall is in the wholesale business of selling men's and boys' clothing. On February 1st, his balance sheet is as follows:

| Balance Sheet, Feb. 1st, 1909. | ||||

|---|---|---|---|---|

| Assets | ||||

| Cash | ||||

| In Bank | $1,765.20 | |||

| In Office | 125.00 | |||

| Total Cash | $1,890.20 | |||

| Accounts and Bills Receivable | ||||

| Bills Receivable | 850.00 | |||

| Henry James, Due | ||||

| Feb. 5 | 350.00 | |||

| David Traver & Co., Due | ||||

| Feb. 15 | 500.00 | |||

| Accounts Receivable | 1,124.00 | |||

| Frank Weitz | 234.00 | |||

| John Gorham | 150.00 | |||

| George Golden | 300.00 | |||

| Clayton & Co. | 275.00 | |||

| Henry Ames | 165.00 | |||

| Total Accounts and Bills Rec. | 1,974.00 | |||

| 19Inventory | ||||

| Men's clothing | $2,240.00 | |||

| Boys' " | 1,200.00 | |||

| Total Inventory | $3,440.00 | |||

| Total Assets | $7,304.20 | |||

| Liabilities | ||||

| Accounts and Bills Payable | ||||

| Bills Payable | 650.00 | |||

| Henry Weir & Co., Due | ||||

| Feb. 7 | 450.00 | |||

| A. Stein & Co., Due | ||||

| March 1 | 200.00 | |||

| Accounts Payable | 675.00 | |||

| D. Meyer & Bro. | 150.00 | |||

| Altman & Sons | 350.00 | |||

| Garson & Co. | 175.00 | |||

| Total Accounts and Bills | ||||

| Payable | 1,325.00 | |||

| Total Liabilities | 1,325.00 | |||

| Present Worth | 5,979.20 | |||

The following transactions are entered on the books:

The following transactions are recorded in the books:

| —Feb. 1st— | |||

| Sold to D. A. Marcus & Son | |||

| 10 overcoats | 7.50 | 75.00 | |

| 10 men's suits | 6.75 | 67.50 | 142.50 |

| —1st— | |||

| Sold to H. A. Branch | |||

| 15 boys' suits | 3.50 | 52.50 | |

| —1st— | |||

| Rec'd from Geo. Golden | |||

| Cash on account | 150.00 | ||

| —2nd— | |||

| Deposited in 1st Nat. Bank | 150.00 | ||

| 20—2nd— | |||

| Sold to John Gorham | |||

| 10 men's suits | 7.00 | 70.00 | |

| 10 men's suits | 6.50 | 65.00 | $135.00 |

| —2nd— | |||

| Sold to Larson & Anderson | |||

| 5 boys' suits | 2.75 | 13.75 | |

| 10 men's suits | 6.50 | 65.00 | 78.75 |

| —2nd— | |||

| Sold for cash | |||

| Men's clothing | 37.50 | ||

| —3rd— | |||

| Sold to Tallman & Co. | |||

| 15 men's overcoats | 7.25 | 108.75 | |

| —3rd— | |||

| Paid 1 month's rent, Ck. | |||

| No. 1 | 75.00 | ||

| —3rd— | |||

| Received from John Gorham | |||

| Cash on account | 150.00 | ||

| —4th— | |||

| Bought from Carson & Scott | |||

| 36 men's corduroy coats | 3.00 | 108.00 | |

| 12 men's corduroy coats | 3.50 | 42.00 | 150.00 |

| Terms 2/10, 1/30, n/60 | |||

| —4th— | |||

| Deposited in 1st Nat. Bank | 187.50 | ||

| —4th— | |||

| Sold to Harris & Rogers | |||

| 12 men's corduroy coats | 3.75 | 45.00 | |

| 5 overcoats | 8.00 | 40.00 | 85.00 |

| —4th— | |||

| Received from Frank Weitz | |||

| Note at 30 days, 6% | 234.00 | ||

| 21—5th— | |||

| Sent to D. Meyer & Bro. Ck. | |||

| No. 2 | $150.00 | ||

| —5th— | |||

| Received from Henry James | |||

| Cash to apply on note | 200.00 | ||

| Cash for interest | 1.75 | $201.75 | |

| New note 30 days, 6% | 150.00 | ||

| —5th— | |||

| Bought from Adler & Co. | |||

| 50 men's suits | 6.25 | 312.50 | |

| Terms 3/10, 1/30, n/60 | |||

| —5th— | |||

| Paid salesman's salary Ck. | |||

| No. 3 | 25.00 | ||

| —5th— | |||

| Drew for personal use Ck. | |||

| No. 4 | 50.00 | ||

| —7th— | |||

| Sold to Henry Ames | |||

| 20 men's suits | 7.50 | 150.00 | |

| 10 boy's suits | 2.75 | 27.50 | 177.50 |

| —7th— | |||

| Sold to Ackley & Son | |||

| 10 boy's overcoats | 3.00 | 30.00 | |

| 10 boy's suits | 2.75 | 27.50 | 57.50 |

| —7th— | |||

| Received from Clayton & Co. | |||

| Check to apply on acct. | 200.00 | ||

| —7th— | |||

| Deposited in 1st Nat. Bank | 401.75 | ||

| —7th— | |||

| Paid our note to H. Weir & Co. | |||

| Check No. 5 | 450.00 | ||

| 22—8th— | |||

| Sold to H. J. Andrews | |||

| 10 men's overcoats | 8.00 | 80.00 | |

| 12 men's corduroy coats | 4.50 | 54.00 | $134.00 |

| —8th— | |||

| Paid express on shipment from | |||

| Carson & Scott, Ck. No. 6 | .90 | ||

| —8th— | |||

| Received from Henry Ames | |||

| Cash on account | 165.00 | ||

| —8th— | |||

| Sold for cash | |||

| 1 job lot boy's clothing | 87.50 | ||

| —9th— | |||

| Deposited in 1st Nat. Bank | 252.50 | ||

| —9th— | |||

| Received from bank, check of | |||

| Clayton & Co., protested | |||

| for non-payment. | |||

| Amount of check | 200.00 | ||

| Protest fees | 2.50 | ||

| —10th— | |||

| Sold to Harris & Landis | |||

| 10 men's overcoats | 7.75 | 77.50 | |

| —10th— | |||

| Sold to Frank Weitz | |||

| 12 men's corduroy coats | 3.75 | 45.00 | |

| —10th— | |||

| Paid Carson & Scott | |||

| Check No. 7 | 147.00 | ||

| Discount 2% | 3.00 | ||

| —10th— | |||

| Paid electric light bill | |||

| Check No. 8 | 3.75 | ||

| 23—10th— | |||

| Received from Clayton & Co. | |||

| Cash to redeem protested | |||

| check | $202.50 | ||

| —10th— | |||

| Inventory at close of business, | |||

| Feb. 10 | |||

| Men's clothing | 1,898.75 | ||

| Boy's clothing | 1,247.75 | ||

Journal entries are to be made to get the accounts, as shown on Feb. 1st, recorded on the books. The transactions are properly entered in journal, cash book, sales book, and invoice register, and posted to ledger. The accounts in the general ledger are closed into trading, and profit and loss—the net profit is credited to proprietor's account—a trial balance is taken after the ledger is closed, and a balance sheet is made. Statements are prepared from sales and purchase ledgers, which agree with the balances of their controlling accounts. All accounts in the general ledger are properly ruled and balances carried forward.

Journal entries need to be made to record the accounts, as shown on Feb. 1st, in the books. The transactions are correctly entered in the journal, cash book, sales book, and invoice register, and then posted to the ledger. The accounts in the general ledger are closed into trading and profit and loss—the net profit is credited to the proprietor's account. A trial balance is taken after the ledger is closed, and a balance sheet is created. Statements are generated from the sales and purchase ledgers, which match the balances of their controlling accounts. All accounts in the general ledger are properly organized, and balances are carried forward.

Opening Entry in Journal

Journal Entry Start

Adjusting Journal Entries

Adjusting Journal Entries

Sales Book and Invoice Register

Sales Record and Invoice Log

SCENE IN SOUTH WATER STREET, WHERE THE COMMISSION HOUSES OF CHICAGO'S GREAT PRODUCE MARKETS ARE LOCATED

SCENE ON SOUTH WATER STREET, WHERE THE COMMISSION HOUSES OF CHICAGO'S MAJOR PRODUCE MARKETS ARE SITUATED

Columnar Cash Journal

Cash Journal Spreadsheet

Columnar Cash Journal

Cash Journal Spreadsheet

Sales Ledger

Sales Record

Sales Ledger

Sales Record

Sales and Purchase Ledgers

Sales and Purchase Records

Purchase and General Ledgers

Purchasing and General Ledgers

General Ledger

General Ledger

General Ledger

General Ledger

General Ledger

General Ledger

Statement of Sales and Purchase Ledger

Statement of Sales and Purchase Ledger

Balance Sheet and Trial Balance of General Ledger

Balance Sheet and Trial Balance of General Ledger

EXERCISES

16. The following transactions are recorded on the books of Parker and Hoadley, Omaha, Neb., wholesale dealers in tea and coffee. In recording these transactions use is made of the books and forms illustrated in this section.

16. The following transactions are logged in the records of Parker and Hoadley, Omaha, Neb., wholesale sellers of tea and coffee. When documenting these transactions, the books and forms shown in this section are used.

A partnership is formed on this date between K. J. Parker and D. C. Hoadley for the purpose of conducting a wholesale tea and coffee business, in the name of Parker & Hoadley, the principal place of business to be Omaha, Neb. Parker invests $3,000.00 cash. Hoadley invests $2,000.00 cash. It is agreed that profits are to be shared on the basis of capital invested, capital to draw interest at 6%, and interest at 6% to be paid on withdrawals. The books are to be closed monthly and the profits divided between the partners. Hoadley is to assume the entire responsibility for the conduct and management of the business, for which he is to receive a salary of $150.00 per month, payable in installments of $75.00 on the 15th and 31st of each month.

A partnership is established on this date between K. J. Parker and D. C. Hoadley to run a wholesale tea and coffee business under the name Parker & Hoadley, with the main office located in Omaha, Nebraska. Parker is contributing $3,000 in cash, while Hoadley is contributing $2,000 in cash. They agree that profits will be shared based on their capital investments, with the capital earning 6% interest, and 6% interest will be paid on any withdrawals. The financial records will be closed monthly, and profits will be divided between the partners. Hoadley will take full responsibility for managing the business and will receive a salary of $150 per month, paid in two installments of $75 on the 15th and 31st of each month.

Deposited in Western National Bank $5,000.00.

Deposited $5,000.00 in Western National Bank.

Withdrew from bank, Ck. No. 1 petty cash $25.00.

Withdrew from bank, Check No. 1 petty cash $25.00.

Bought from Leggitt & Co., New York, 30 chests Japan tea, 1,455# at .37½, 20 chests Oolong tea, 972# at .40; terms net 30, 2/10, f. o. b. N. Y.

Bought from Leggitt & Co., New York, 30 chests of Japanese tea, 1,455 lbs at $0.375, 20 chests of Oolong tea, 972 lbs at $0.40; terms net 30, 2/10, f.o.b. N.Y.

Bought from Laughlin & Co., Chicago, 20 sacks Rio coffee, 1,020# at .22½, 20 sacks Java coffee, 985# at .25; 20 sacks Mocha coffee, 970# at .25; terms net 30, 2/10, f. o. b. Omaha.

Bought from Laughlin & Co., Chicago, 20 sacks of Rio coffee, 1,020 lbs at $0.225, 20 sacks of Java coffee, 985 lbs at $0.25; 20 sacks of Mocha coffee, 970 lbs at $0.25; terms net 30, 2/10, f. o. b. Omaha.

Paid rent of store 1 month to James Roberts, Ck. No. 2, $60.00.

Paid rent for the store for 1 month to James Roberts, Check No. 2, $60.00.

Sold to Ames & Johnson, 92 12th St., on account, 3 chests Japan tea, 149# at .48; sack Rio coffee, 50# at .28; 1 sack Java coffee, 52# at .32.

Sold to Ames & Johnson, 92 12th St., on account, 3 chests of Japan tea, 149# at $0.48; 1 sack of Rio coffee, 50# at $0.28; 1 sack of Java coffee, 52# at $0.32.

Sold to Landis & Snow, So. Omaha, on account, 2 chests Oolong tea, 101# at .52; 1 sack Mocha coffee, 47# at .32; 2 sacks Rio coffee, 98# at .28.

Sold to Landis & Snow, So. Omaha, on account, 2 chests Oolong tea, 101# at $0.52; 1 sack Mocha coffee, 47# at $0.32; 2 sacks Rio coffee, 98# at $0.28.

Sold to J. C. Peters & Son, 267 Roberts St., 3 chests Oolong tea, 146# at .52, 5 sacks Rio coffee, 252# at .48.

Sold to J. C. Peters & Son, 267 Roberts St., 3 chests of Oolong tea, 146# at $0.52, 5 sacks of Rio coffee, 252# at $0.48.

39 Bought for cash from Harris & Co., 1 office desk and chair $45.00, gave Ck. No. 3 in payment.

39 Bought for cash from Harris & Co., 1 office desk and chair for $45.00, paid with Check No. 3.

Paid freight on coffee from New York by Ck. No. 4, 12.93.

Paid freight on coffee from New York by Ck. No. 4, 12.93.

Sold to Wright & Noble, 146 7th St., 2 sacks Java coffee, 99# at .32; 2 sacks Mocha coffee, 101# at .32.

Sold to Wright & Noble, 146 7th St., 2 bags of Java coffee, 99# at .32; 2 bags of Mocha coffee, 101# at .32.

Sold to Horgis & Co., 84 Jackson St., 5 chests Japan tea, 248# at .48.

Sold to Horgis & Co., 84 Jackson St., 5 chests of Japanese tea, 248 pounds at $0.48.

Sold to Winters & James, 92 Hastings St., 4 chests Japan tea, 201# at .48; 3 chests Oolong tea, 138# at .52; 2 sacks Java coffee, 97# at .32.

Sold to Winters & James, 92 Hastings St., 4 chests of Japanese tea, 201# at .48; 3 chests of Oolong tea, 138# at .52; 2 sacks of Java coffee, 97# at .32.

Sold for cash 1 sack Rio coffee, 47# at .28; 1 chest Japan tea, 45# at .48.

Sold for cash: 1 sack of Rio coffee, 47# at $0.28; 1 chest of Japan tea, 45# at $0.48.

Sold to Cobb & Willet, 892 Park Av., 2 chests Japan tea, 92# at .48; 1 chest Oolong tea, 47# at .52; 1 sack Rio coffee, 44# at .28; 1 sack Java coffee, 45# at .32; 1 sack Mocha coffee, 43# at .32.

Sold to Cobb & Willet, 892 Park Ave., 2 chests of Japanese tea, 92# at .48; 1 chest of Oolong tea, 47# at .52; 1 sack of Rio coffee, 44# at .28; 1 sack of Java coffee, 45# at .32; 1 sack of Mocha coffee, 43# at .32.

Sold to Young & Criger, 62 Watson St., 5 sacks Mocha coffee, 205# at .32; 3 chests Oolong tea, 127# at .52.

Sold to Young & Criger, 62 Watson St., 5 sacks of Mocha coffee, 205# at $0.32; 3 chests of Oolong tea, 127# at $0.52.

Bought from Japan Importing Co., San Francisco, 60 chests Japan tea, 2,700# at .36, f. o. b. Omaha, net cash; gave our note at 10 days without interest in payment.

Bought from Japan Importing Co., San Francisco, 60 chests of Japan tea, 2,700 pounds at $0.36, f.o.b. Omaha, net cash; provided our note for 10 days without interest as payment.

Paid account of Leggitt & Co., less 2% discount, Ck. No. 5.

Paid account of Leggitt & Co., minus 2% discount, Check No. 5.

Ames & Johnson paid their account, less 2% cash discount.

Ames & Johnson paid their bill, taking a 2% cash discount.

Deposited cash received to date.

Cash deposited to date.

Sold to Wade & Francis, 92 Bluff St., 10 chests Japan tea, 448# at .48.

Sold to Wade & Francis, 92 Bluff St., 10 chests of Japanese tea, 448# at .48.

Paid for telegram—petty cash—.40.

Paid for telegram—petty cash—$0.40.

Received check from Landis & Snow in full settlement of their account.

Received check from Landis & Snow for the full amount owed on their account.

Sold to J. C. Peters & Son, 5 sacks Java coffee, 231# at .32.

Sold to J. C. Peters & Son, 5 sacks of Java coffee, 231 lbs at $0.32.

Sold for cash 3 sacks Rio coffee, 127# at .28; 2 sacks Mocha coffee, 89# at .32; 3 sacks Japan tea, 131# at .48.

Sold for cash 3 sacks of Rio coffee, 127# at $0.28; 2 sacks of Mocha coffee, 89# at $0.32; 3 sacks of Japan tea, 131# at $0.48.

Deposited cash on hand, also check of Landis & Snow.

Deposited cash on hand, also a check from Landis & Snow.

40 Sold to Ames & Johnson, 2 sacks Mocha coffee, 91# at .32; 2 chests Oolong tea, 87# at .52.

40 Sold to Ames & Johnson, 2 sacks of Mocha coffee, 91# at $0.32; 2 chests of Oolong tea, 87# at $0.52.

Sold to Wright & Noble, 3 chests Japan tea, 129# at .48; 1 chest Oolong tea, 42# at .52.

Sold to Wright & Noble, 3 chests of Japanese tea, 129# at .48; 1 chest of Oolong tea, 42# at .52.

Paid for fuel by check No. 6 to Rogers Coal Co., 12.00.

Paid for fuel by check No. 6 to Rogers Coal Co., $12.00.

Paid clerk's salary, check No. 7, 10.00.

Paid clerk's salary, check No. 7, $10.00.

Paid for labor, check No. 8, 16.50.

Paid for labor, check No. 8, $16.50.

Sold to Watkins & Fish, 64 Prairie Av., 5 chests Oolong tea, 207# at .52.

Sold to Watkins & Fish, 64 Prairie Ave., 5 chests of Oolong tea, 207 lbs at $0.52.

Bought from Western Grocer Co., Chicago, 50 chests Oolong tea, 418# at .39; 20 sacks Rio coffee, 876# at .22¼; 10 sacks Java coffee, 434# at .25; 15 sacks Mocha coffee, 653# at .25; terms 30 days net, 2/10, f. o. b. Omaha.

Bought from Western Grocer Co., Chicago, 50 chests of Oolong tea, 418 lbs at $0.39; 20 sacks of Rio coffee, 876 lbs at $0.22¼; 10 sacks of Java coffee, 434 lbs at $0.25; 15 sacks of Mocha coffee, 653 lbs at $0.25; terms 30 days net, 2% discount if paid within 10 days, freight on board Omaha.

Received from Wright & Noble cash in payment of our bill of Jan. 4th, less 2% cash discount.

Received from Wright & Noble cash to pay our bill from January 4th, minus a 2% cash discount.

Received from bank, check of Landis & Snow protested for non-payment, protest fees added 1.90.

Received from the bank, check from Landis & Snow was protested for non-payment, protest fees added $1.90.

Sent Laughlin & Co. our check No. 9 in payment of account

Sent Laughlin & Co. our check No. 9 as payment for the account.

Sold to Raymond H. Moss, 182 Spring St., 5 chests Japan tea, 217# at .48; 5 sacks Rio coffee, 214# at .28.

Sold to Raymond H. Moss, 182 Spring St., 5 chests of Japanese tea, 217 lbs at $0.48; 5 sacks of Rio coffee, 214 lbs at $0.28.

Sold to Watkins & Fish, 10 sacks Mocha coffee, 424# at .32.

Sold to Watkins & Fish, 10 sacks of Mocha coffee, 424 lbs at $0.32.

Cobb & Willet paid their account in full, deducting 2% for cash.

Cobb & Willet settled their bill completely, taking a 2% discount for paying in cash.

Deposited cash on hand.

Cash deposited.

Sold to Cobb & Willet, 5 chests Japan tea, 213# at .48.

Sold to Cobb & Willet, 5 chests of Japanese tea, 213# at $0.48.

Sold for cash, 2 sacks Rio coffee, 88# at .28.

Sold for cash, 2 sacks of Rio coffee, 88 lbs at $0.28.

Paid our note to Japan Importing Co., check No. 10.

Paid our invoice to Japan Importing Co., check No. 10.

Paid sundry office expenses from petty cash 3.60.

Paid miscellaneous office expenses from petty cash $3.60.

Sold to Wade & Francis 3 sacks Rio coffee, 123# at .28; 2 sacks Mocha coffee, 86# at .32.

Sold to Wade & Francis 3 sacks of Rio coffee, 123# at $0.28; 2 sacks of Mocha coffee, 86# at $0.32.

Paid clerk's salary, ck. No. 11, 10.00.

Paid clerk's salary, check No. 11, $10.00.

Paid for labor, ck. No. 12, 16.50.

Paid for labor, ck. No. 12, $16.50.

Paid ½ month's salary to D. C. Hoadley, ck. No. 13, 75.00.

Paid half a month's salary to D. C. Hoadley, check No. 13, $75.00.

1st. Balance cash, first charging petty cash expenditures as a cash payment.

1st. Balance the cash, starting by recording petty cash expenses as a cash payment.

2nd. Post purchase book, sales book, journal, and cash book.

2nd. Purchase book, sales book, journal, and cash book.

3rd. Take a trial balance.

3rd. Prepare a trial balance.

4th. Credit interest to partner's accounts.

4th. Add interest to partner's accounts.

5th. Take an inventory of stock on hand. The records show quantities purchased and quantities sold. When the same goods have been purchased at different prices, use the last price paid in figuring inventory.

5th. Take an inventory of the stock on hand. The records show how much was purchased and how much was sold. When the same items have been bought at different prices, use the most recent price paid to calculate the inventory.

6th. Close accounts into trading and profit and loss accounts.

6th. Finalize the trading and profit and loss accounts.

7th. Distribute net profits to partners' capital accounts.

7th. Distribute net profits to the partners' capital accounts.

COMBINED ORDER AND SALES RECORD

17. Instead of keeping separate order and sales books, both records may be combined on one blank. This is accomplished by the use of order blanks provided with columns for the distribution of sales to the different departments. Before the order is filled these blanks are handled in the same manner as those without distribution columns. When filled, the amounts are extended in the proper columns and the invoice made. The orders are then filed in a binder, each day's orders being kept together, and postings made direct to customers' accounts. The footings are carried forward to the end of the month and totals posted to sales accounts. The original orders thus become a loose leaf sales book.

17. Instead of keeping separate order and sales books, both records can be combined on one form. This is done by using order forms that have columns for allocating sales to different departments. Before the order is filled, these forms are handled like those without distribution columns. Once filled, the amounts are recorded in the appropriate columns and the invoice is prepared. The orders are then organized in a binder, with each day's orders kept together, and entries are made directly to customers' accounts. The totals are carried over to the end of the month and summed up in the sales accounts. The original orders then serve as a loose leaf sales book.

ABSTRACT OF SALES

18. When the order blank is used as a sales record, making a sales book with a record of a single sale to a sheet, it is somewhat inconvenient to determine from the footings the total sales for the day. This information is of considerable value, as a knowledge of what is being done from day to day is of importance to the principals of a business. Such a record is provided for by an abstract of sales on a separate sheet. This abstract should show total sales for each day, both cash and on account, divided by departments.

18. When the order form is used as a sales record, creating a sales book with a record of one sale per sheet, it can be a bit inconvenient to figure out the total sales for the day just by looking at the footings. This information is really valuable, as knowing daily figures is important for the business owners. An abstract of sales on a separate sheet provides this record. This abstract should display total sales for each day, both cash and credit, organized by department.

The blank may be made the same size as the order blanks, and filed in the sales binder at the beginning of the month. Sales are 42recorded daily and footings carried forward to the end of the month, when the totals may be posted direct to the credit of the sales account in the general ledger. The totals of sales on account will be posted to the debit of the sales controlling account in the general ledger.

The blank can be the same size as the order blanks and filed in the sales binder at the start of the month. Sales are recorded daily and totals are carried forward to the end of the month, when the totals can be directly posted to the sales account in the general ledger. The totals of sales on account will be posted to the debit of the sales controlling account in the general ledger.

OUT FREIGHT

19. The proper treatment of freight paid on outgoing shipments is an important question in accounting. When goods are sold at delivered prices, the freight paid is one of the items of expense in selling the goods, and when the books are closed the account will be closed into profit and loss. However, in a wholesale business, freight is sometimes paid as an accommodation to the customer when the goods have been sold at f. o. b. prices. Although the amount should be added to the invoice it should not be credited to the sales account as this would be taking credit for a fictitious trading profit. Such an item should be made a special charge against the customer by means of a journal entry.

19. The correct handling of freight charges on outgoing shipments is a key issue in accounting. When goods are sold at delivered prices, the freight costs count as part of the expenses involved in selling those goods, and when closing the books, this account will be reflected in profit and loss. However, in a wholesale business, freight may be paid as a favor to the customer when the goods are sold at f.o.b. prices. Even though the amount should be included on the invoice, it shouldn’t be credited to the sales account, as that would falsely reflect a trading profit. This charge should be specifically applied to the customer through a journal entry.

Combined Order and Sales Record

Combined Order and Sales Log

THE GENERAL OFFICES OF THE SAMUEL C. TATUM CO., CINCINNATI, OHIO

THE GENERAL OFFICES OF THE SAMUEL C. TATUM CO., CINCINNATI, OHIO

Abstract of Sales by Departments

Sales Summary by Departments

SALES EXPENSE

20. In a wholesale or manufacturing business it is very desirable that the exact cost of selling goods be known. Broadly, this cost is covered under the general head of sales expense, but this is usually divided into several classes of expenditures. The segregation of the various items of sales expense is desirable for the purpose of determining the percentage of each. The items which properly belong in sales expense depend somewhat on the nature of the business. For example, traveling expenses are usually a direct sales expense, but in some businesses they may be chargeable to the cost of purchases. The items entering into sales expense of the average business are: advertising, salaries of salesmen, traveling expenses of salesmen, commissions paid on sales, cost of packing and shipping, out freight.

20. In a wholesale or manufacturing business, it's really important to know the exact cost of selling goods. Generally, this cost falls under the category of sales expenses, but it's typically broken down into several types of expenditures. Breaking down the different items of sales expense is useful for figuring out the percentage of each. The items that should be included in sales expense depend somewhat on the type of business. For instance, travel expenses are usually considered a direct sales expense, but in some businesses, they might be charged to the cost of purchases. The items that make up the sales expense in an average business include: advertising, salespeople's salaries, travel expenses for salespeople, commissions on sales, packing and shipping costs, and outbound freight.

21. Advertising. This account should be charged with all expenditures for publicity such as newspaper, magazine, street car, and bill board advertising, cost of printing catalogs, booklets, and circulars. Where there is any reason for so doing, the cost of the different classes of advertising can, of course, be kept in separate accounts. The aim and object of advertising being to increase the sale of goods, it is properly considered an item of sales expense.

21. Advertising. This account should include all expenses for publicity like newspaper, magazine, streetcar, and billboard ads, as well as the cost of printing catalogs, booklets, and circulars. If necessary, the costs for different types of advertising can be tracked in separate accounts. Since the purpose of advertising is to boost sales, it is rightly regarded as a sales expense.

22. Salaries of Salesmen. This account is charged with all salaries paid to salesmen whether traveling or working in the house. Commissions and bonuses are sometimes included in this account, but it is usually considered best to keep them in separate accounts.

22. Salaries of Salespeople. This account includes all salaries paid to salespeople, whether they are traveling or working in-house. Commissions and bonuses are sometimes included in this account, but it's usually best to keep them in separate accounts.

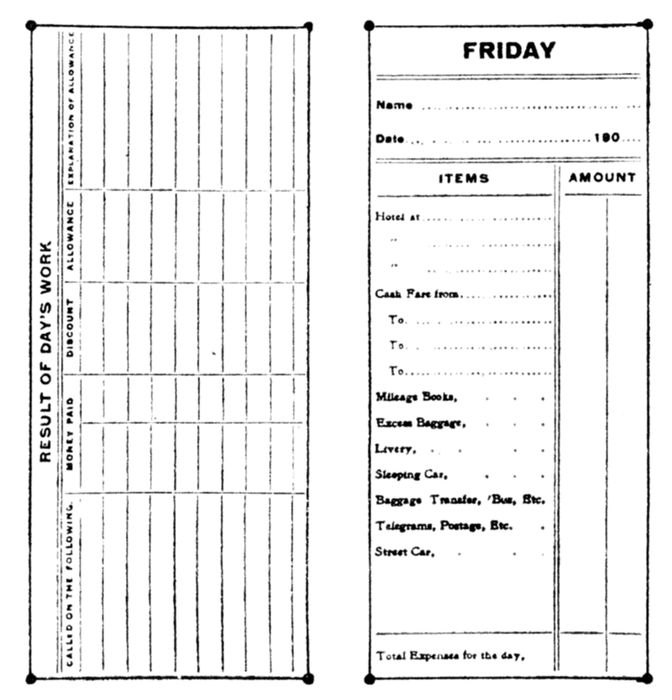

23. Traveling Expenses of Salesmen. This account is charged with all legitimate traveling expenses of salesmen, the specific items included depending largely on the nature of the business. For example, in some businesses a liberal allowance is made for the entertainment of customers, while in others this item is never allowed. In any business the traveling expense account requires careful scrutiny. Salesmen should be required to furnish an itemized statement or voucher of expenses at stated intervals. For convenience, this should be made on a form specially provided for the purpose. One of the most convenient and popular expense vouchers is in the form of a book of a convenient pocket size, with a page for each day of the week and a summary of the week's expenses on the last page.

23. Traveling Expenses of Salesmen. This account covers all legitimate travel expenses for salespeople, with specific items varying based on the type of business. For instance, some companies allow a generous budget for entertaining clients, whereas others do not permit this expense at all. Regardless of the business, the travel expense account needs careful examination. Salespeople should provide a detailed statement or receipt of expenses at regular intervals. For convenience, this should be done using a specially designed form. One of the most practical and popular expense vouchers is a compact notebook that includes a page for each day of the week and a summary of the week's expenses on the last page.

24. Packing and Shipping. This account is charged with the 45entire cost of packing goods for shipment. It includes such items as wages of shipping clerk and his assistants, crates, lumber, boxes, and all other packing materials.

24. Packing and Shipping. This account covers the full cost of packing goods for shipment. It includes expenses like the wages of the shipping clerk and their assistants, crates, lumber, boxes, and all other packing materials.

TRIAL BALANCE BOOK

Traveler's Expense Book

Travel Expense Report

25. To save rewriting the names of the accounts each month, a trial balance book can be used to good advantage. These books are made to accommodate six trial balances on a double page, and are sometimes made with alternate short leaves so that twelve trial balances may be made with one writing of the names. When the trial balance book is used, care must be exercised in providing space for the addition of new accounts in each section. Where separate sales and purchase ledgers are used, it is best to provide a trial balance book for each ledger.

25. To avoid rewriting the names of the accounts every month, you can effectively use a trial balance book. These books are designed to hold six trial balances on a double page and are sometimes made with alternating short leaves so that twelve trial balances can be recorded with one entry of the names. When using the trial balance book, it's important to ensure there's enough space for adding new accounts in each section. If you have separate sales and purchase ledgers, it's best to have a trial balance book for each ledger.

THE CHECK REGISTER

26. Large check books are cumbersome to handle and necessitating the expenditure of much needless labor. Their use is rapidly giving way in modern offices to the check register. The check register has several distinct advantages. It exhibits, in compact form, a record of all checks issued and can also be arranged to show deposits and balance in the bank. Distribution columns can be provided with headings for the different expenditure accounts, which makes of the check register a cash expenditure book. The form should be varied to suit the business in which it is to be used. A typical form is illustrated on page 37.

26. Large checkbooks are clunky to use and require a lot of unnecessary effort. Modern offices are quickly transitioning to check registers instead. The check register has several clear advantages. It provides a compact record of all issued checks and can also be organized to display deposits and bank balances. It can include columns labeled for different spending categories, making the check register work as a cash expenditure book. The format should be adapted to fit the specific business it’s being used for. A typical format is shown on page 37.

27. Checks in Pads. When the check register is used it is the usual custom to have checks put up in pads. After the check is written, it is registered and numbered to correspond to the register number. With the use of padded checks, it is not necessary for the clerk who writes the check to know anything about the bank balance.

27. Checks in Pads. When using a check register, it’s common practice to have checks in pads. After a check is written, it gets recorded and numbered to match the register number. With padded checks, the clerk who writes the check doesn’t need to know anything about the bank balance.

Trial Balance Book

Trial Balance Ledger

Check Register Combined with Cash Expenditure Book

Check Register Combined with Cash Expenditure Book

Cash Received Book

Cash Receipt Log

Checks in Pads

Checks in Pads

CASH RECEIVED BOOK

28. A cash book specially ruled for a record of cash received is used to supplement the check register or cash expenditure book. Columns are provided for the different classes of receipts, with one credit column. It is assumed that all cash received is deposited, payments being made exclusively by check. This does not refer to petty cash expenditures which should be kept in a petty cash book or on envelope vouchers.